Download Briefing Paper

What Does CETA Achieve on Services?

The Most Favoured Nation Clause

EU Services Liberalisation in CETA

What Would CETA+++ Offer in Services?

How Many Pluses: Can the UK Improve on CETA?

The UK is a services-driven economy. About 80% of UK output comes from the services sector and 45% of UK total exports are cross-border flows of services.[1] In terms of value added, services exports generate a larger flow of income than goods exports, and the services sector runs a substantial export surplus, going some way towards offsetting the deficit on the goods account. Moreover, cross-border trade is only one of the ways in which services exports are delivered. The other major route (so-called mode of supply) is via commercial presence whereby British-owned firms establish and sell services in other countries. In 2014, the UK’s international investment position in services sectors abroad stood at about £500 billion.[2]

The Comprehensive Economic and Trade Agreement (CETA) between the EU and Canada has figured as a template for a future UK-EU trade relationship, in pronouncements by both the European Commission and the UK government. CETA has a number of appealing aspects, such as a near 99% removal of tariffs on goods and an aim of closer co-operation in areas such as regulation, conformity assessments and standards. At the same time, Canada retains sovereignty over its laws and its external trade policy, satisfying two of the UK government’s declared ‘red lines’.[3] In December 2017, Brexit secretary David Davis argued for a “Canada plus plus plus” (CETA+++) agreement with a vision to achieve “an overarching free trade deal, but including services, which Canada doesn’t”.[4]

The statement that CETA does not include services is frequently repeated, yet CETA devotes a large part of its long text to just that. The European Commission praises CETA as the most comprehensive trade agreement on services that it has ever concluded.5 Moreover, its services provisions were vocally criticised during the negotiation process: for example, the European Public Service Union (EPSU) opposed

“The inclusion of public services in CETA” and “CETA’s ‘negative list’ approach for services commitments and the inclusion of ‘standstill’ and ‘ratchet’ mechanisms that lock-in liberalisation”.[6]

So, what does CETA offer in terms of access to EU services markets, and does it provide a solution to the UK’s desire to keep good access to such markets post-Brexit? This paper assesses the degree of services trade liberalisation offered by the EU in CETA. We find that some sectors are relatively open, but, equally, some sectors important to the UK – such as financial services and transport services – remain significantly restricted. These are the areas in which the UK government should be seeking ‘pluses’, but for a number of reasons, we conclude that CETA+++ would be a poor substitute for the Single Market and that such a deal is, in any case, unlikely to be achieved.

The following sections briefly summarise CETA’s provisions on services and investment and our main findings with respect to the EU’s commitments in CETA. For further details on the degree of EU services and investment liberalisation in CETA, and the methodology used to derive these results, see our working paper “European Union services liberalisation in CETA”. [7]

Trade in services can be conducted in several different ways: in trade-speak, ‘through different modes of supply’. The General Agreement on Trade in Services (GATS) defines four different modes of supply: Cross-border supply (mode 1), consumption by a resident abroad (mode 2), commercial presence (mode 3) and the presence of natural persons (mode 4).[8]

CETA covers all four modes of supply – modes 1 and 2 in chapter 9 (Cross-Border trade in services), mode 3 in chapter 8 (Investment) and mode 4 in chapter 10 (temporary entry and stay of natural persons for business purposes). There are also additional chapters on financial services, international maritime transport, telecoms and e-commerce respectively. CETA, like GATS, achieves services liberalisation through a set of key obligations. The central obligations are market access and national treatment, which prohibit quantitative restrictions and discriminatory treatment of services, service suppliers and investors from the other party.[9]

Broadly speaking there are two approaches to services liberalisation in trade agreements; using a positive list or a negative list. For the first time in an EU Free Trade Agreement (FTA), CETA uses a negative list for modes 1, 2 and 3. In such an approach, all services sectors are liberalised by default and a party must list any sectors or sub-sectors it wishes to limit or exclude from the commitments. As such, a negative list is usually considered to provide a greater degree of transparency and predictability, and since the default position is to liberalise all sectors, this increases the scope for sectoral coverage and provides valuable clarity on the sectors that contain restrictions.

CETA, as most other agreements, still contains a number of broad explicit carve-outs: services supplied in the exercise of government authority (as long as it is not commercial or in competition with others) and most air services are excluded, and the EU also excludes audio-visual services. In addition, there are hundreds of pages of further reservations listed in two annexes. Annex I gives all reservations for existing measures that the parties wish to maintain. These reservations are subject to standstill and ratchet, essentially locking in the prevailing regulatory conditions, and ensuring that any future liberalisation cannot subsequently be withdrawn. Annex II contains reservations for future measures, by which the parties retain the right to adopt new or different (more liberal or more restrictive) measures in the future, providing scope for future policy space.

While Annexes I and II apply to most of the chapters related to services and investment, the presence of natural persons (mode 4) is dealt with separately in CETA using both positive and negative lists, and as such it is also discussed separately in this paper.

An important feature of CETA is the inclusion of a Most Favoured Nation (MFN) clause that applies to both investment and cross-border trade (articles 8.7 and 9.5 respectively), as well as the chapters on temporary entry and stay of natural persons, financial services and international maritime transport.

The MFN clause means that any CETA+ commitments made by the EU in an existing or future trade agreement with a third country (e.g. the UK after Brexit) must be extended to Canada in the relevant dimensions. The EU excludes from MFN any very deep agreement, essentially related to the rights and obligations within the Single Market. Annex I and II contain some reservations with respect to the MFN clause, giving the relevant party the right to provide differential treatment to a third country where such exceptions exist, but overall these reservations are few. Similar to other trade agreements, the MFN clause also does not apply to measures providing for recognition (such as the recognition of accreditation of testing and analysis services).

The MFN clause could pose a significant challenge in a future UK-EU deal, as it may limit the EU’s willingness to offer more favourable terms to the UK if it then must also extend this treatment to Canada.[11] Similar MFN clauses are also found in other recent EU trade agreements, such as the EU-Korea agreement.

With over 550 EU reservations contained in Annex I and II, some applying to the EU as a whole and others only to individual member states, it is difficult to get an overall understanding of the actual degree of liberalisation offered by the EU in CETA.

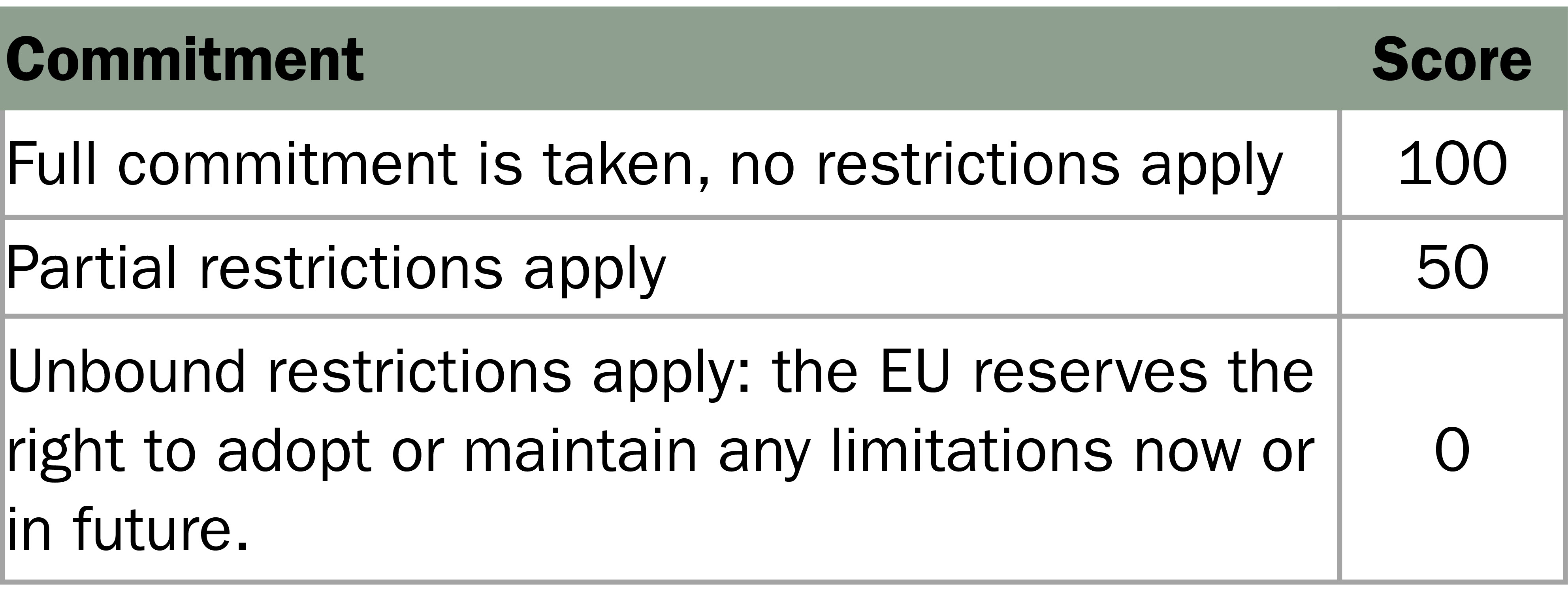

To inform this discussion we produce a summary of the degree of liberalisation granted by the EU across a wide range of services sectors. Inspired by the work of Bernard Hoekman, [12] we score the EU’s commitments as either 0, 50 or 100 depending on the degree of liberalisation.

At the most detailed level we cover 675 different categories as defined in the provisional Central Product Classification system from 1991.[13] We create EU27-wide summaries for each services sector by weighting each EU member’s score by GDP and then aggregating the scores across member states.[14]

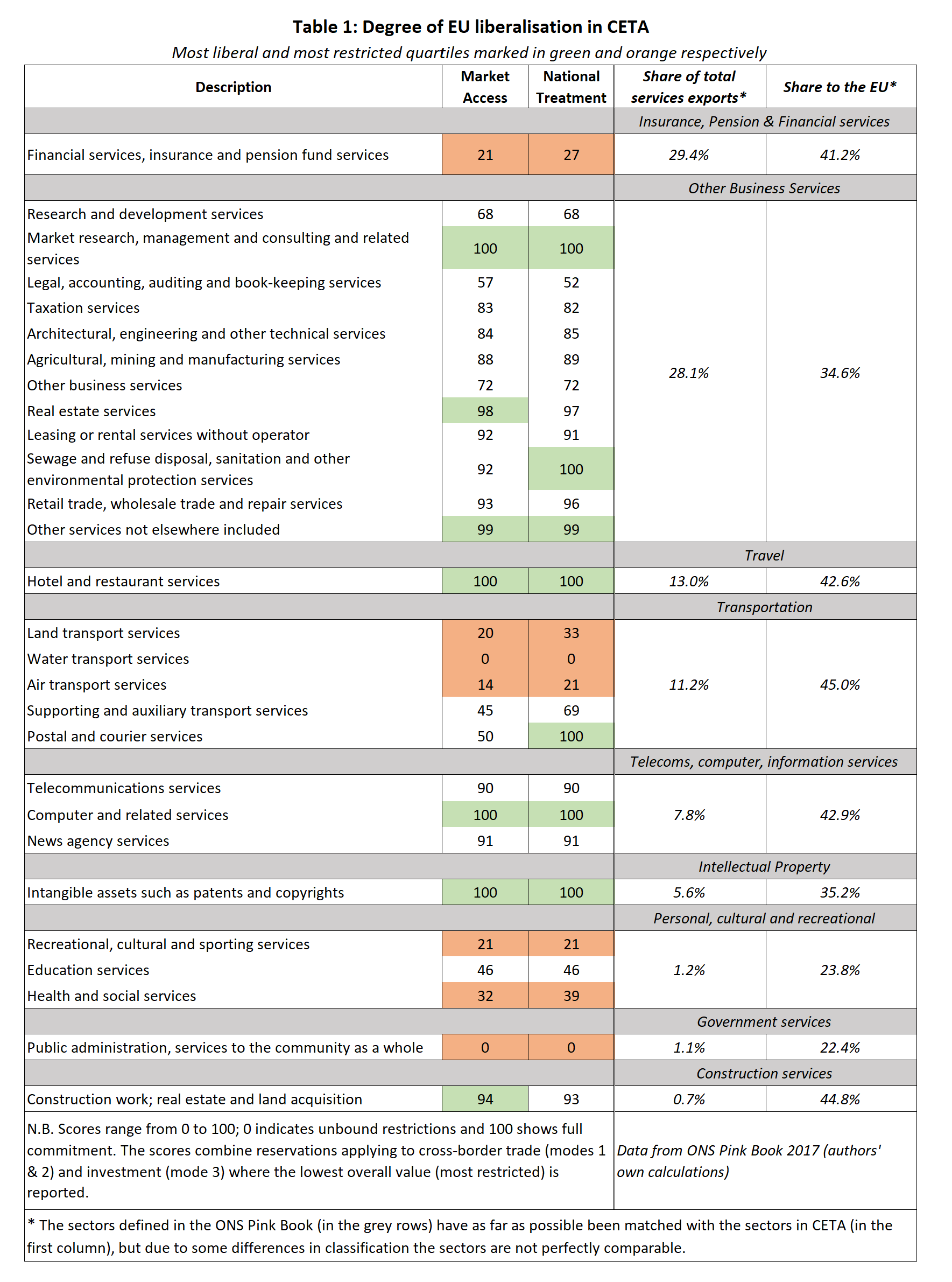

Table 1 contains a summary of the degree of liberalisation granted by the EU in CETA for the two key obligations of market access and national treatment across a range of services sectors. Scores range from 0 to 100, where 0 shows that there is at least one unbound reservation applying to the EU as a whole. This does not necessarily mean that the sector is entirely closed to trade; it simply denotes that the EU reserves the right to adopt or maintain any restrictions now or in the future with respect to at least one mode of supply in the sector. In contrast, a value of 100 indicates that no restrictions apply and thus that the sector is fully committed. Because the scoring method does not capture variations in the degree of restrictiveness within each threshold (e.g. all partial restrictions are given the same score (50) regardless of their relative degree of restrictiveness), the estimates should be viewed as indicative rather than precise and not perfectly comparable across sectors.

The top and bottom quartiles (the most liberal and most restricted sectors) are highlighted in green and orange respectively. To give an indication of the relative importance of the sectors to the UK, the final two columns provide export data for a number of services categories defined in the ONS Pink Book (2017). The left-hand column gives each sector’s share of total UK services exports in 2015, and the right-hand column has the corresponding share of these exports that went to the EU. One caveat is that for some sectors trade might predominantly take place through establishing a local presence (mode 3) or through mode 4, which would not be reflected in the ONS figures since they only account for cross-border trade flows.

Insurance, pension and financial services combined accounted for the largest share of UK services exports in 2015. This sector is one of the most restricted in CETA with cross-border trade being limited to a very narrow range of services, including insurance services related to transport and freight, certain types of banking services such as financial advisory services and portfolio management services.[15] Overall, this considerably limits the scope for cross-border trade in financial services. There are further restrictions both at the EU-wide level and for individual member states, such as requirements related to establishment, specific legal forms, licensing and authorisation. Like all trade agreements, CETA also contains a prudential carve-out giving each party the right to take ‘reasonable’ measures for prudential reasons. Most importantly for the UK, CETA does not provide anything similar to passporting, since a local license is still needed for the provision of services.[16]

Recreational and cultural services are also among the most restricted, owing in part to the overall exclusion of audio-visual services, but also to further EU restrictions on cultural services. Additionally, the transport sector is highly restricted with land, water and air services exhibiting high degrees of protection. A caveat to this is that in some sectors, such as air transport, bilateral agreements separate to CETA govern access and regulatory matters, and in such cases Table 1 may overstate the restrictiveness.

The restrictions on insurance, pension, financial services and transport services are problematic; combined, these sectors accounted for 40.5% (£93 billion) of total UK cross-border services exports in 2015, of which 42% (£39 billion) went to the EU. If Brexit reduced access to the EU in these sectors this would likely have a negative impact on exporters in the UK.

‘Other business services’ has the second largest share of total services exports, after insurance, pension and financial services, although exports in this sector are relatively less EU-driven than in most other categories. This sector encompasses a wide range of services where the degree of liberalisation varies quite considerably. For legal services, many EU member states have made at least one reservation, particularly concerning domestic and EU law, where admission to the Bar and residency is often required. Although not reflected in Table 1, this sector is also heavily dependent on trade through mode 4, the movement of natural persons.

For mode 4, the relevant part of CETA is chapter 10 – Temporary entry and stay of natural persons for business purposes. It is important to recognise that even the most liberal mode 4 agreement is no substitute for the freedom of movement of workers guaranteed by the European Single Market. Mode 4 grants the right to travel to a country to provide a service, subject to a number of conditions, whereas freedom of movement grants access to the labour market. In the former, entry is defined in terms of the service, (usually restricted to a specific contract negotiated prior to arrival) whereas the latter allows a worker to take any job open to locals. CETA describes access rules in terms of key personnel, short-term business visitors, contractual service suppliers and independent professionals, and for each category sets out time limits on visits and, where applicable, the qualifying activities. CETA also establishes a framework for the recognition of professional qualifications, but leaves these to be negotiated in the future, and as such, provides little of immediate value.

CETA describes access rules in terms of key personnel, short-term business visitors, contractual service suppliers and independent professionals, and for each category sets out time limits on visits and, where applicable, the qualifying activities. CETA also establishes a framework for the recognition of professional qualifications, but leaves these to be negotiated in the future, and as such, provides little of immediate value.

It is also worth noting that the UK is notably restrictive in terms of mode 4 regulations; in CETA the UK registers restrictions in every single mode 4 category that we distinguish. Thus, the policy challenge in this area is less likely to be the EU’s restrictions than the UK’s.

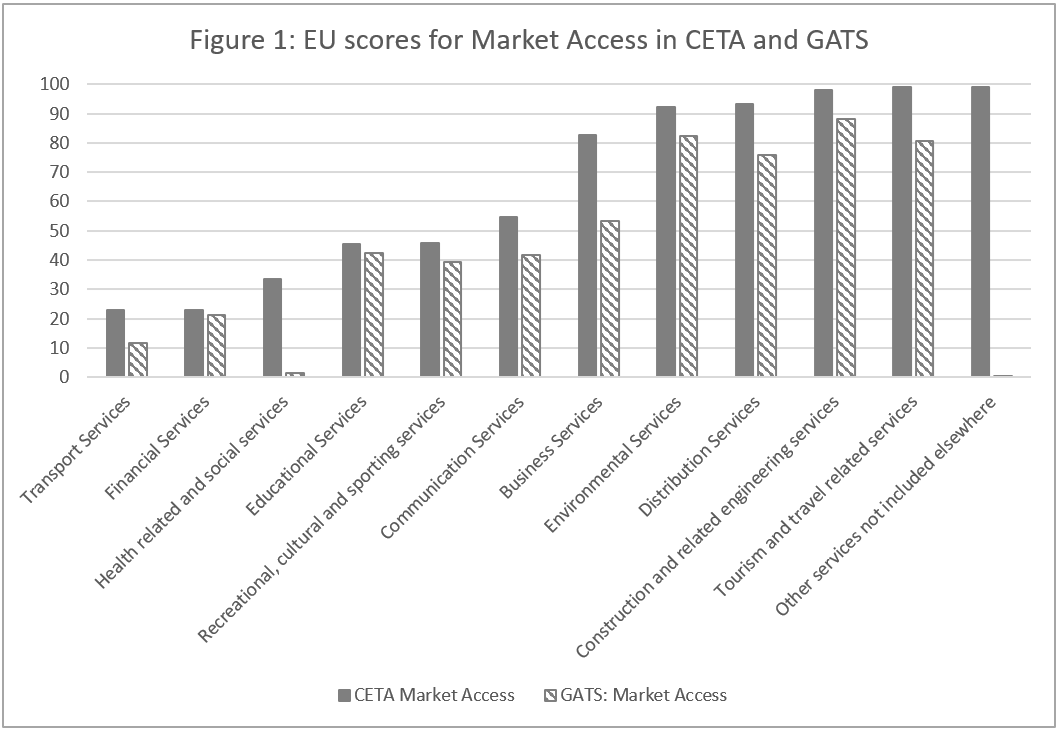

As seen in Table 1, some sectors are fully, or close to fully committed by the EU; hotel and restaurant services, computer services and real estate services, to name a few. Can this level of liberalisation be attributed to CETA? Perhaps unsurprisingly the answer is ‘not necessarily’. Whether or not CETA achieves new levels of liberalisation depends on the EU’s pre-CETA policies, governed, in part, by the EU’s commitments in GATS. Therefore, using the same scoring methodology as discussed earlier, we score the EU’s commitments in GATS as a comparison to the provisions in CETA.[17]

Figure 1 displays the scores for market access in CETA and GATS across the 12 services categories defined in GATS, starting from the left with CETA’s most restricted sector. CETA exhibits a higher degree of liberalisation in all sectors.[18] The largest step towards liberalisation is for the residual category ‘other services not included elsewhere’ and further improvements are in health-related services, business services and distribution services. In other sectors, such as educational services and financial services, the estimates are almost identical. With respect to market access in financial services, the limited selection of cross-border services committed in CETA is generally identical to those committed in the GATS, except for insurance intermediation and portfolio management services, where CETA goes further than GATS.

The GATS schedule binds the minimum level of commitment afforded by a country; however, applied policies tend to be considerably less restricted.[19] It is, therefore, not surprising that overall CETA achieves a higher degree of liberalisation than GATS. By simply binding the policies already applied by the EU, CETA would commit to a higher level of liberalisation on paper, but achieve little change in actual policies. Creating such certainty is valuable for countries (like Canada) that would otherwise be vulnerable to the EU unilaterally scaling back its openness to GATS levels [20] However, it is a poor substitute for the openness and security provided by the Single Market.

Moreover, despite CETA going further than the GATS schedule, it still follows the schedule closely. A comparison of the one-third most restricted sectors in CETA and GATS shows that three out of the four most protected sectors in CETA were also the most restricted in GATS. The same holds true for the most liberal sectors in CETA and GATS. Thus, it seems that the EU has been unwilling to make significant commitments to open up the sectors where protection really matters to it.[21]

From the preceding discussion and Table 1, we identified the sectors that are quantitatively important to the UK in terms of services exports to the world and to the EU, but where the EU’s policies are relatively restricted in CETA. In terms of a CETA+++, it is clear that sectors such as financial services, transport services and certain business services would benefit from ‘pluses’, and as such, they could be a good place to start. However, suppose the UK were able to negotiate a deep and comprehensive trade agreement with the EU that covered most services sectors; would this compensate for the loss of access entailed in withdrawing from the Single Market? It would clearly be better for exports than no agreement or even one that covered just a few sectors, but it would be a poor substitute for the Single Market. Even a large swathe of sectoral agreements would fail to deliver the ‘architectural’ – the over-arching – aspects of the Single Market, or its automaticity.

There are at least three important architectural features of the Single Market. Top of the list is the common legal framework in which any EU citizen or firm has access to an enforcement system that ultimately ends up in the same Court – the Court of Justice of the European Union – which is independent of political pressures and fundamentally even-handed. Effective redress is central to services trade because unlike goods, which can be inspected before entry into a country, consumers must purchase a service before they know its quality, and key features of that quality arise from conditions in the country of production over which the importing country has no jurisdiction. For example, banks keep their reserves in their home country and those using these banks from abroad rely on that function being suitably policed. Similarly, this is the case with the governance of broadcasters or the quality of technical advice from commercial lawyers. If such re-assurances are not complete, the governments of services importing countries will come under pressure from consumers, or from local competing producers, to regulate imports themselves, which will both absorb resources and dampen competition and trade. No dispute settlement system in any free trade agreement (FTA) approaches the level of assurance that the EU court system offers.

The second architectural feature of importance is the free mobility of persons, which, as we noted above, no FTA has ever come close to replicating. Despite the improvements in communications technology, services transactions still depend heavily on an element of face-to-face contact. The freedom of mobility within the Single Market, coupled with the wide and deep mutual recognition of professional qualifications within the EU, means that such contact can be achieved without planning and bureaucracy – avoiding the uncertainty that these inevitably entail. This again increases competition and saves resources. A recent study of the markets for certain professional services in the USA found that “the between-state migration rate for individuals in occupations with state-specific licensing exam requirements is 36 percent lower relative to members of other occupations” and cited evidence that lower migration was associated with a higher cost of services.[22]

Third, data exchange is fundamental to effective service provision in many sectors. The EU’s data regulation is uniform across the Union. Hence, services firms in one member state can operate across the Single Market with no concerns about legality or extra effort to manage data exchange.

The Single Market also has a strong degree of automaticity. Through the direct effect of EU Regulations and the requirement to apply EU Directives via local law, members of the Single Market have a high degree of confidence that services trade within the Market will not suddenly be undermined by administrative fiat or regulatory divergence. The UK, on the other hand, is proposing that in certain sectors it should have the right to diverge from the EU at a time of its own choosing, either by declining to follow changes in EU law or by explicitly repudiating it. The trading relationship between the UK and the EU would become less a commitment to continuing alignment – which would support long-run investments in the European economy – and more a recipe for opportunistic collaboration, which would not. Investment and integration will inevitably decline even if de facto the UK remains closely aligned with the EU.

Even an ambitious CETA+++ would not support existing levels of services trade between the UK and the EU. But we ought also to consider whether the UK is likely to achieve all these pluses in the first place.

In some areas, the EU will likely be happy to agree a deeper level of integration with the UK than it offered in CETA. For example; CETA respects the two parties’ different domestic requirements on data protection and exchange, and, except for commitments not to operate these in an obviously discriminatory way, takes no step towards integrating them. The EU will permit full data exchange only with third countries it deems to have ‘adequate’ – i.e. effectively European – protections. It currently grants Canada partial adequacy status, which ensures free cross-border data flows in certain sectors, and CETA makes no advance on this. Following Brexit, if the UK chose to adhere closely to the General Data Protection Regulation (GDPR), which, as a member state it will be obliged to apply from May 2018, data exchange could be freer than with Canada, and this position could be enshrined in a UK-EU trade agreement.

Another area in which Canada may have constrained the level of ambition in CETA is financial services. Canada has traditionally maintained significant barriers to trade in this sector – for fear of being dominated by the huge US industry, and for prudential reasons. While the EU has stated that it has never signed an FTA containing significant liberalisation in financial services, it did propose one in TTIP and may therefore be willing to agree more with the UK than it obtained in CETA .[23]

Overall, however, it seems unlikely that the EU will be willing to offer an FTA that grants the UK much more access in services than granted to Canada in CETA. First, the EU places great store on the integrity of the Single Market, manifested by its oft-expressed unwillingness to countenance ‘cherry-picking’. It is true that the UK and the EU start with a greater degree of alignment in services than any previous FTA,[24] and this does, indeed, make it easier for the EU to agree a deeper and more extensive agreement with the UK than with other third countries. The problem, however, is that this is not what the EU seeks. The EU conceives of its Single Market as a single package in which participants accept all its facets – those that are in their immediate material interests and those that are not. This is partly because free and competitive markets depend on a whole range of institutional and other arrangements that cannot be adequately replicated by sector-specific agreements, and partly because of fears that the delicate balance of costs and benefits necessary to bind twenty-seven sovereign nations into such a complex web would rapidly unravel if those nations could choose their participation ‘à la carte’.

The EU has signed FTAs and equivalence agreements that grant countries access to some European markets on terms that are similar to those of member states. For example, the EU-Korea FTA contains text on cars, pharmaceuticals and financial services, and CETA facilitates mutual recognition of conformity assessments in several sectors. Similarly, the EU permits exceptions and derogations from the Single Market without ejecting countries from it – for example, the UK has several derogations even as a member of the EU, and Norway does not apply the Single Market in its entirety. Thus, it seems that to some extent the EU can live with an incomplete market. Based on this, some commentators argue that the UK’s aim of a deep and comprehensive trade agreement is just a matter of degree, not of principle, and that the EU’s intransigence about ‘cherry picking’ is unreasonable and surmountable.

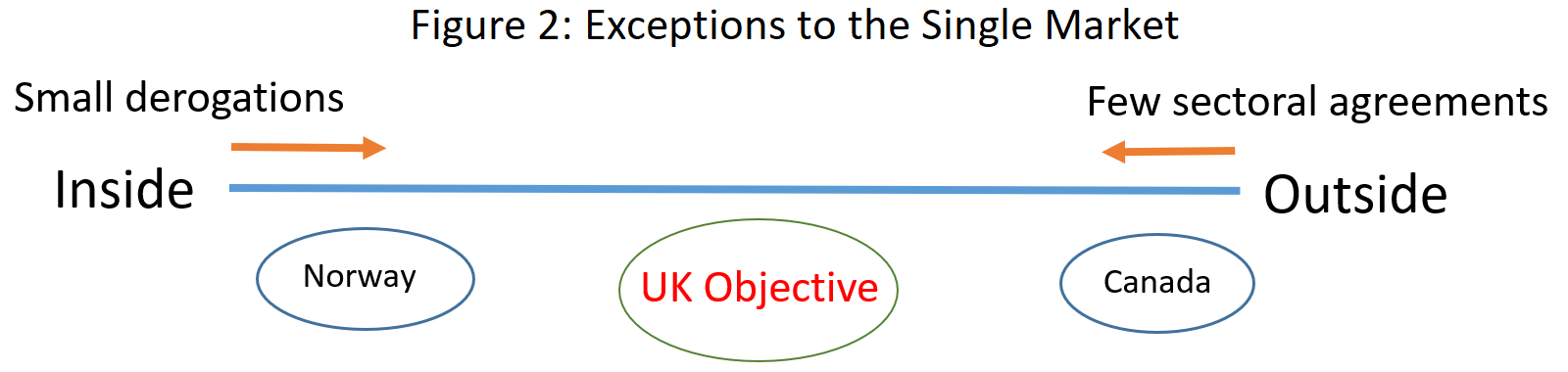

This may be true, but a more reasonable interpretation is that the integrity of the Single Market is a matter of deep principle for the EU, especially in the face of a full-frontal attack of the sort that some UK politicians have mounted. You are either inside or outside the Single Market. Pragmatism dictates that in the former case a few derogations are possible (Norway) and in the latter case a few concessions (Canada) can be made, but not so many as to threaten the distinction between ‘in’ and ‘out’. Figure 2 illustrates this interpretation, treating the degree of integration as if it were a simple linear phenomenon; while Norway and Canada are acceptable as variants of ‘in’ and ‘out’, the UK objective of half-in half-out is qualitatively different. None of this is to say that there is nothing to negotiate on services, the UK may well achieve a little more flexibility than Norway or a few more concessions than Canada, but it will have to be understood as a series of small exceptions, not a fundamentally different ‘bespoke’ deal.

Figure 2 proceeds as if the UK were seeking to define its position on integration once and for all. But, as noted above, it actually seeks scope to diverge further in the future. This is almost the complete antithesis of the efforts in other trade agreements which focus on preventing unnecessary divergences through chapters on regulatory cooperation. These lack teeth, but at least cultivate a constructive atmosphere. Some scholars argue that reducing regulatory frictions, in the absence of deep political arrangements, is possible by building trust between regulators so they can agree to accept differences in their respective regulatory systems on the basis that the end objectives are deemed equivalent. This equivalence status could permit trade without additional regulations on the part of the importing country.[25] Such equivalence is in the gift of the importing country’s authorities and is often easily rescinded; thus achieving and maintaining equivalence long-term requires considerable diplomatic cooperation over long periods. The atmosphere of an exit negotiation is arguably not conducive to discussing equivalence calmly and objectively. Nevertheless, establishing the means to do this should figure very high in the UK’s priorities as soon as the outlines of the future UK-EU trade relationship are settled. The diplomatic groundwork for this could usefully start immediately.

Two further factors discussed above contribute to making CETA+++ a poor basis for seeking good access to EU services markets. First, CETA does not advance services liberalisation much beyond what the EU is willing to offer to all trading partners (erga omnes, in trade-speak). It does not address the thorny issues that have been partially solved within the Single Market – for example, bank passporting or the broadcasting licence. Thus, defining CETA as a starting point leaves a huge amount to be done.

Second, the most favoured nation (MFN) clauses that pervade the services and investment chapters of CETA mean that, short of creating a (sectoral) Single Market, any concessions that the EU offers to the UK have to be extended ‘for free’ to Canada (and in some cases to Korea and other partners). In mercantilist terms, these MFN clauses raise the cost of any concessions the EU makes. Canada is not so large that this makes offering concessions impossible, but it is clearly a discouragement.[26]

The entire discussion so far has been in terms of UK exports of services, but, of course, the real benefit of international trade is from imports. By opening the markets for services to EU suppliers, the Single Market has increased competition and reduced prices in the UK, which has both boosted UK productivity and benefitted UK consumers directly. In principle, the UK could open its own market independently of whether it signs a trade agreement with the EU. However, in absence of an agreement, it has to do so on an MFN basis. Since the UK wishes to persuade other countries to sign trade agreements that cover services, the more likely outcome is therefore that if the EU will not keep its markets open to UK providers, the UK will not do so to EU providers. The result will be a decline in competition and an increase in consumer prices relative to the status quo.

Britain needs trade agreements in services – its area of comparative advantage – and in particular with its largest market for services exports. CETA is the most comprehensive trade agreement on services that the EU has ever signed with a third country, and although CETA does liberalise services trade, it does not do so to anything like the extent that UK services providers have grown used to in the Single Market. Moreover, CETA lacks important architectural aspects of the Single Market, which are of particular importance in services trade. In short, ‘CETA plus’ would not solve the UK’s services problem.

The authors are grateful to seminar attendees at both the UKTPO and the European Policy Centre for discussion, and to Bernard Hoekman, Hamid Mamdouh and Pierre Sauvé for comments on a draft Working Paper on the analysis of CETA. Naturally, none of them is responsible for the paper’s remaining shortcomings.

The authors assert their moral right to be identified as the authors of this publication. Readers are encouraged to reproduce material from UKTPO for their own publications, as long as they are not being sold commercially. As copyright holder, UKTPO requests due acknowledgement. For online use, we ask readers to link to the original resource on the UKTPO website.

[1] Harris, James (2017) “Revealing the exports map of Britain – what ONS is learning about international trade in services” Office for National Statistics https://blog.ons.gov.uk/2017/10/02/building-a-better-understanding-of-local-level-service-exports/

[2] Borchert, Ingo (2016) “Services Trade in the UK: What is at stake?” UK Trade Policy Observatory, Briefing Paper 6, http://blogs.sussex.ac.uk/uktpo/files/2017/01/Briefing-paper-6.pdf

[3] Gasiorek, Michael (2018) “UK-EU trade relations post Brexit: binding constraints and impossible solutions” UK Trade Policy Observatory, Briefing paper 17 http://blogs.sussex.ac.uk/uktpo/publications/uk-eu-trade-relations-post-brexit-binding-constraints-and-impossible-solutions/

[4] Morales, Alex (2017), “U.K. Seeking ‘Canada Plus Plus Plus’ EU Trade Deal, Davis Says”, Bloomberg https://www.bloomberg.com/news/articles/2017-12-10/u-k-seeking-canada-plus-plus-plus-eu-trade-deal-davis-says

[5] European Commission (2017) “Guide to the Comprehensive Economic and Trade Agreement (CETA)” http://trade.ec.europa.eu/doclib/docs/2017/september/tradoc_156062.pdf

[6] European Public Service Union, (2016) “EPSU calls for the rejection of CETA because it’s a bad deal for citizens” https://www.epsu.org/article/epsu-calls-rejection-ceta-because-its-bad-deal-citizens

[7] Magntorn, Julia and Winters, L. Alan (forthcoming in 2018) “European Union services liberalisation in CETA” University of Sussex Economics Department Working Paper 08-2018: http://www.sussex.ac.uk/economics/research/workingpapers

[8] For further information and examples of the four modes of supply, see the glossary in Borchert (2016): http://blogs.sussex.ac.uk/uktpo/files/2017/01/Briefing-paper-6.pdf

[9] Further obligations prohibiting performance requirements and nationality requirements for senior management and board of directors are incorporated into the chapters on Investment and Financial Services. Additional obligations also apply to Maritime Transport – for example, obligations to allow the supply of feeder services between ports.

[10 Marchetti, Juan and Roy, Martin, (2009) “Services liberalization in the WTO and in PTAs.” In Marchetti, Juan & Roy, Martin (Eds.), Opening Markets for Trade in Services: Countries and Sectors in Bilateral and WTO Negotiations (WTO Internal Only, pp.61-112). Cambridge: Cambridge University Press. doi:10.1017/CBO9780511812392.005

[11] One wit has suggested that this is what the third ‘plus’ stands for ‘extra liberalisation for the UK plus Canada’.

[12] Hoekman, Bernard (1996). ‘Assessing the General Agreement on Trade in Services’ in W. Martin and L.A. Winters (eds.), The Uruguay Round and the Developing Countries. Cambridge: Cambridge University Press.

[13] There are several versions of the CPC, of which CETA uses CPC provisional; United Nations, 1991, Statistical Papers series M, no 77.The relevant sections for our analysis are categories 5-9 which include non-transportable goods and services.

[14] Any UK restrictions are excluded from the analysis since we are interested in the EU27’s commitments; the UK’s contribution to EUGDP has therefore also been excluded in the weighting.

[15] The full list of qualifying services is found in Annex 13-A of CETA and apply to all EU members except Belgium, Cyprus, Estonia, Latvia, Lithuania, Malta, Poland, Romania and Slovenia who all committed slightly different bundles of sectors.

[16] Hill, Dominic and Kent, Rachel (2017) ‘Does CETA provide a workable model for market access in the financial services industry?’ Hogan Lovells http://www.hoganlovellsbrexit.com/blog/64/does-ceta-provide-a-workable-model-for-market-access-in-the-financial-services-industry

[17] For this comparison we use a draft GATS schedule from 2006 that applies to the EU-25. For further details on the GATS schedule and the methodology applied, see Magntorn and Winters (2018 “European Union services liberalisation in CETA” University of Sussex Economics Department Working Paper Series: http://www.sussex.ac.uk/ economics/research/workingpapers

[18] For Environmental Services, there are, curiously, a number of sub-sectors where CETA appears more restricted than GATS, particularly with respect to the three sectors specified in the WTO’s W/120 list for this category. This is because, in these sectors, Germany included a market access restriction in CETA that it did not include in GATS. However, averaging the scores across all sub-sectors committed by the EU in this category still gives CETA a higher (more liberal) score than GATS.

[19] Borchert, Ingo, Gootiiz, Batshur and Mattoo, Aaditya (2011) “Services in Doha: what’s on the table?” In: Martin, Will and Mattoo, Aaditya (eds.) ‘Unfinished Business? The WTO’s Doha Agenda.’CEPR and World Bank, London, pp. 115-143. ISBN 9781907142451 https://voxeu.org/sites/default/files/file/unfinished_business_web.pdf

[20] On the benefits of binding existing policies in a trade agreement, see Handley, Kyle, and Nuno Limao (2015). “Trade and investment under policy uncertainty: theory and firm evidence.” American Economic Journal: Economic Policy 7.4 (2015): 189-222. https://www.aeaweb.org/articles?id=10.1257/pol.20140068

[21] For further discussion on the EU’s commitments in trade agreements compared to GATS, see Francois, Joseph, Hoekman, Bernard, Nelson, Doug (2015) ‘TTIP, regulatory diversion and third countries’ In: Akman, Sait, Evenett, Simon, Low, Patrick (eds) ‘Catalyst? TTIP’s impact on the Rest’, CEPR Press, pp. 19-26 https:// voxeu.org/sites/default/files/file/TTIP_23march.pdf

[22] Johnson, Janna E. and Kleiner, Morris M. (2017) “Is Occupational Licensing a Barrier to Interstate Migration?” NBER Working Paper No. 24107 http://www.nber.org/papers/w24107.pdf

[23] For more on this see Corporate Europe Observatory (2014) “Leaked document shows EU is going for a trade deal that will weaken financial regulation” https://corporateeurope.org/financiallobby/ 2014/07/leaked-document-shows-eu-going-trade-deal-willweaken- financial-regulation

[24] Although even here alignment is not total because the Single Market in services is still incomplete.

[25] Hoekman, Bernard (2017) “International Regulatory Cooperation in a Supply Chain World” in Tapp, Stephen, Assche, Ari Van and Wolfe, Robert (eds.)“Redesigning Canadian Trade Policies for New Global Realities”, Volume VI, Institute for Research and Public Policy (IRPP) http://irpp.org/wp-content/uploads/2015/08/AOTS6-hoekman.pdf

[26] When the UK comes to negotiate with Canada, the MFN clauses in CETA are virtually prohibitive. Any concession that Canada offers the UK beyond those in CETA, will have to be extended to the EU, an economy six times the size of the UK’s, ‘for free’.

Doi: 10.20919/9781912044559