Download Briefing Paper

An Overview of UK Services Trade

Trade in services is the dark matter that, well, matters. It is economically significant for several reasons, partly because it directly affects UK consumers’ welfare in such sectors as telecommunications, health or retail distribution, and partly because producer services such as finance, transportation or professional services are inputs into both the production and international exchange of goods. In addition, because of the UK’s comparative advantage in many services sectors, including but not limited to the financial sector, services trade makes a positive contribution to the UK’s current account.

Consequently, Brexit will have important repercussions for the UK’s economic ties with the EU in the realm of services markets, yet gauging Brexit’s effects comprehensively is not straightforward. The complexities of understanding services trade emanate from three principal features:

1. Services are traded via multiple ‘modes of supply’ (see glossary at the end) that each feature entirely different regulatory environments. It is not enough to simply look at cross-border trade in services; instead, flows of capital, people and goods are all intrinsically linked to services trade.[1] For example,

– Services can be brought to consumers by foreign providers establishing a commercial presence, in which case all the regulatory provisions governing inward investment apply.

– Professionals may travel abroad to discharge their services locally, in which case a host of professional qualification and certification issues arise.

– A substantial share of the value of traded merchandise goods consists of services, so that any impediment to goods trade has potential indirect effects on embodied services.

2. There are no explicit measures of either transport costs or trade protection; instead, nearly all measures affecting service trade are of a regulatory, ‘behind-the-border’ nature that are difficult to keep track of, let alone assess their potential impact on services trade.

3. Policy-making roles and responsibilities are much more scattered across governmental agencies than in goods trade. Neither is there one department/ministry for services trade policy within each country, nor is there one uniform EU services trade policy towards external partners.

This Briefing Paper elaborates on these aspects so as to highlight how Brexit might directly and indirectly affect UK services trade and policy-making in this area. The paper commences with a picture of current UK services trade across the various modes of supply. The revealed strengths of the UK in services could usefully inform negotiating priorities going forward. The Briefing Paper also provides an overview of prevailing services trade policies, showing how market access regimes differ across EU countries and across sectors. A related aspect is preferential market access abroad outside of the Single Market. The paper therefore provides an overview of agreements with services or investment provisions that the EU has concluded in the past. It is likely that the UK will cease to be party to these agreements after Brexit.

The international exchange of services can occur through multiple channels, which are often linked both from a business as well as a policy making perspective.

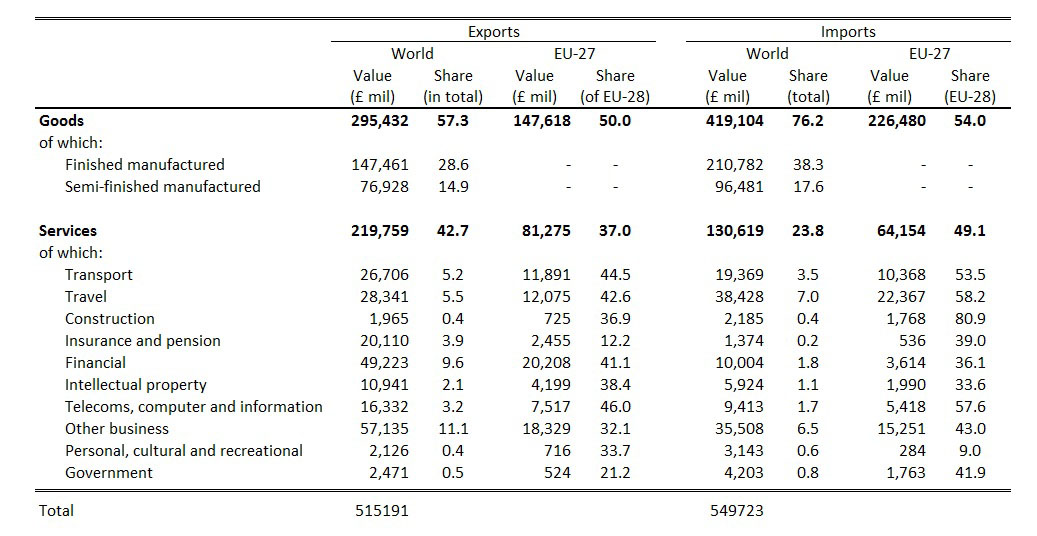

Cross-border trade in services (or ‘mode 1’) involves the direct exchange of a service, often in digitised form, and is relatively well captured in balance of payments statistics. In 2014 the UK exported a total of about £220 billion services and imported £130 billion, thus running a sizable surplus in terms of cross-border services trade (Table 1). Thus the value of cross-border services exports is quantitatively important – services exports constitute 43% of total UK exports (goods and services) whereas services imports account for one-quarter of total imports.

Table 1 shows the different categories in which cross-border services trade is recorded in the balance of payments. It can be seen that services trade is much broader than financial services. In particular, one of the most traded category (“Other business services”) encompasses a rich set of producer services such as research and development, design, marketing, or brand management.

Whilst the UK is running a sizable trade deficit in goods, both overall and with the EU, the British economy exports more than twice as much ‘other commercial services’ than it imports.[2] The largest components therein are business and financial services, respectively. The provision of such services is likely associated with high skilled jobs.

In terms of geographic orientation, relative to total world exports and imports of services, about one-third of UK services are exported to the EU[3] and one-half of all services imports originate from the EU. These shares underscore how tightly the UK is intertwined with continental Europe. Transportation and Telecommunications exhibit particular high export shares directed towards the EU, owing probably to those sectors’ intrinsic link with goods trade. At the same time, Asia is also an important region with which the UK exchanges a range of distinctly ‘producer input’ type of services.[4]

It is important to note that the value of services trade, and its share relative to goods trade, refers to cross-border trade in services only. These figures do not include other forms of trading services, which will be discussed below. The value of services trade in its entirety is likely to be much larger than cross-border services trade, even though not all parts are equally well-represented in official statistics.

Table 1: UK Trade in Goods and Services, by Sector and Destination, 2014

Source: ONS Pink Book 2015; author’s own calculations.

Notes: Figures refer to 2014. ‘-’ denotes not available. ‘Services’ encompass cross-border trade in services as per the UK balance of payments. Relative shares of goods and services refer to total trade in merchandise goods and services, respectively (not current account totals).

Another principal way of trading services is for a foreign supplier to set up shop in another country so as to serve customers (consumers or corporate entities) locally. The value of services thus provided, i.e. through the establishment of a commercial presence, is captured in Foreign Affiliate Trade Statistics (FATS, or “mode 3” in GATS speak). Unfortunately, FATS statistics are not widely available and it has instead become customary to rely on foreign direct investment (FDI) figures, for which somewhat better statistics exist albeit often not in a very detailed manner. Comparing the value of services trade across alternative modes is fraught with difficulty, partly because of mis-measurement and partly because the relative importance of modes varies across countries and sectors. However, generally speaking mode 3 services trade is quantitatively as important as cross-border services trade.

In 2014 the UK’s international investment position in services sectors abroad stood at about £500 billion, having fallen relative to 2013, whereas foreign businesses held about £671 billion in domestic services sector firms, up by 18 percent from the previous year due to investments primarily from Europe and the Americas.[5] Half of the inflow from Europe went into information and communication industries whilst the rise from America was mainly driven by financial services industries. Overall these figures demonstrate the UK’s strong position in attracting Foreign Direct Investment (FDI); indeed, the inward stock of FDI (encompassing all sectors, not just services) amounts to 51 percent of UK GDP, which is appreciably higher than the world average (34 percent).[6]

Some of this investment might directly benefit British consumers (e.g. the local presence of firms such as Lidl, a German retailer, or Santander UK plc, a wholly foreign owned British bank). For business services, EU membership was perhaps one contributing factor drawing inward investment into the UK, for instance by foreign firms seeking to serve UK manufacturing activity, which itself benefitted from the Single Market. Often large service providers are shadowing large manufacturing firms as they expand their operations geographically. As such, Brexit could alter the rationale for at least some of the investment that has previously been flowing into services sectors.

The effect of Brexit on outward FDI of Brexit may be more muted insofar as local establishment is often a precondition for providing services and is not easily reversible. That said, establishment in professional services sectors often takes specific forms such as partnerships, which are reliant on the recognition of qualifications or experience. The potential lapse post-Brexit of facilitating Single Market legislation such as the directive on Mutual Recognition of Professional Qualifications could have a detrimental effect on mode 3 trade in certain services sectors.

In addition to the four modes of supply as conventionally set out in the GATS framework, services are also effectively traded as embodied inputs into a country’s merchandise exports. This has sometimes been called ‘mode 5’ services trade.[7] The phenomenon can be seen as part of a wider secular trend called ‘servicification’, which refers to firms increasingly using external service providers in support of their principal economic activity, typically manufacturing. This could take the form of ‘domestic outsourcing of activities such as accounting, design, or marketing, which were previously done in-house. Yet there is nothing to prevent such services from being procured from abroad via any of the conventional modes of delivery.[8] In any event, independent from where service inputs originate, ‘mode 5’ trade highlights the fact that, partly as a result of servicification, a good deal of gross merchandise exports consists of domestic services content.

Whilst this particular kind of services trade is not widely appreciated, preliminary evidence suggests that it is quantitatively important. Based on TiVA statistics, Cernat and Kutlina-Dimitrova estimate that as of 2009 nearly 35% of EU-27 gross merchandise exports in fact represented services inputs (equivalent to over 300 billion Euro). In 1995 that ‘mode 5’ share stood at 28%. Hence, not only is trade in embodied services inputs large in absolute terms, its share has been increasing by 23 percent. These intermediate services inputs originate from domestic services production that, in turn, could either be supplied by domestic service sector firms such as banks or transport enterprises (e.g. HSBC or British Airways), or alternatively supported by FDI, e.g. Bank of America (UK) or the UK affiliate of UPS. This latter case represents an example of inbound mode 3 services trade facilitating outbound mode 5 services trade. As it happens, it was the British economy that recorded the largest increase in the share of high-skilled labour in manufacturing value added (+10.2 percentage points) over 1995-2008 of all advanced economies.[9] Given that many producer services are skill-intensive activities, and that a good deal of manufacturing value added is exported, this development could indicate that ‘mode 5’ services trade has become more and more relevant for the UK economy.

It is evident that for such trade to flow smoothly, two seemingly unrelated policy instruments, namely the UK’s policy towards inward investment as well as the export destination’s goods trade regime, would need to align in a suitable way. The case of ‘mode 5’ services trade illustrates that goods and services production appear to be ever more intertwined in a technology-intensive manufacturing base. For trade policy to support this development, the demands for coordinating hitherto unrelated areas of policy-making may be rising. In a nutshell, the variety and quality of available services plays an ever more important role in making manufacturing competitive.

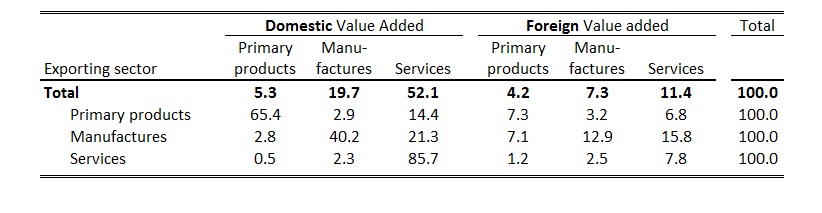

Over the past two decades, the UK economy has continuously deepened its integration into international production fragmentation, and the services sector is assuming a key role in this process. Conceptually, economies participate in ‘Global Value Chains’ (GVC) by importing foreign inputs to produce the goods and services they export (henceforth called ‘backward GVC participation’) and also by exporting domestically produced inputs to partners in charge of downstream production stages (called ‘forward GVC participation’). Between 1995-2011, the share of foreign value added content in UK exports rose from 18.2% to 23%, whilst the share of domestic value added sent to third countries rose from 19% to 24.7%.[10] Thus these figures, which are most likely an underestimate of the current situation as they do not include the most recent rebound years after the Great Recession, show that both forward and backward GVC links have become stronger. Services have been a key driver of this development (Table 2), in particular by forging forward linkages. This shows that UK services are an important input into downstream production located abroad. The prevalence of forward linkages underscores the salience of market access for UK services exports.

Table 2: Domestic and foreign Value-Added Contribution to Gross Exports in the UK, 2011

Source: WTO: UK profile “Trade in Value Added and Global Value Chains”, cf. endnote 10. Note: Figures denote percent shares of sectoral value added in industry total gross exports.

Table 2 demonstrates that more than half of the value added of UK total exports in 2011 consisted of domestic services value added (52.1%). At the same time, total UK exports also contained 11.4% of foreign services value added. In terms of dynamics, these two value added shares of UK total exports—domestic and foreign services—have each grown by 7 percent every year over the period 1995-2001. It is not surprising that services value added constitutes the majority of services exports, but even with regard to UK manufacturing exports as a subset of total exports, domestic services contribute 21.3% to value added, and a further 15.8% are foreign services. Overall, domestic services are underpinning export performance in a crucial way, even though the import side, i.e. securing foreign services as inputs into UK exports, appears to be nearly as important.

A final point worth emphasising is the upstream position of UK services trade. Considering the UK’s forward GVC participation, i.e. domestically produced inputs that go on to be exported to third countries via at least one other partner economy, the top three industries are all services sectors. These are “other business services” (22.9%), “wholesale and retail trade” (11.8) and “financial intermediation” (10.3), respectively, with their percentage share in total exports of domestic inputs given in brackets. The top destinations are Germany, Ireland and China, thus highlighting again the dominant role of EU trade partners for forward linkages. By contrast, there is no service sector amongst the top three industries for backward GVC participation, i.e. imported foreign inputs for UK exports.[11]

The EU’s policy-making competencies were recently broadened when, as part of the 2009 Treaty of Lisbon, FDI became part of the EU’s Common Commercial Policy. As far as services trade policy is concerned, it is still the case though that across all four GATS modes of supply, the EU merely provides for a framework of rules, from which individual EU member states deviate when it comes to market access and national treatment in their domestic markets.[12] This is true for both applied policies as well as GATS commitments, and the extent of such derogations between member states differs appreciably across sectors.

What does this mean for the UK’s future access to the European market? To begin with, the EU’s GATS schedule of commitments defines the legally binding conditions that would apply to the UK as a WTO member in its own right in the absence of any other arrangement. There are two implications of this ‘fall back scenario’ that are worth keeping in mind. First, most WTO founding members of the GATS did not make very ambitious commitments on market access and national treatment, therefore trading on GATS terms is typically rather undesirable.[13] At the same time, countries are free to apply more liberal policies than they committed to under the GATS, and many do, so that actual MFN policy regimes typically afford (much) better market access than what GATS schedules would prescribe. This phenomenon is known as ‘commitments overhang.[14] As a result, market access and national treatment for the UK as an ordinary WTO member may be somewhat worse compared to the status quo as an EU member yet in reality, it may not be as bad as GATS schedules might suggest. In any event, it needs to be borne in mind that applied MFN regimes lack the legal certainty and predictability of membership in the Single Market.

Policies that apply to services trade amongst EU economies are likewise more open than applied policies towards third countries such as the US or Japan. An additional feature is that applied policies could—and do—vary across EU member states, reflecting the fact that there is not one uniform EU external services trade policy towards non-members. Rather, individual EU member states at times apply different policies for service suppliers from within versus from outside the EU. Hence, post-Brexit UK suppliers will face a new set of actual market access conditions in EU markets across services sectors and modes of supply, respectively, and there is no simple rule to gauge the incremental change in actual market access conditions.

An example may help illustrate how the difference in conditions within and outside the Single Market differs across sectors. Consider for instance the retail distribution sector, in which there is basically no difference for retailers from within the EU and outside the EU, respectively, when it comes to establishing commercial presence in any EU country. In principle, the same is true in the telecoms sector, except for France where non-EU persons or firms cannot hold more than 20 percent of voting shares in firms operating radio-based infrastructure. As a counter-example, the situation is widely different in the legal sector, in which policies range from no restrictions for establishing a commercial presence in ten member states to Austria where only licensed lawyers from EEA countries may open branches. Five member states require EU/EEA nationality or admission to the Bar in an EU member state for lawyers to temporarily move to an EU country to advise on foreign law.

It is between these two corner outcomes—the actual policies towards non-EU countries and the status quo (ie. full access to the Single Market)—that there is space that could potentially be exploited during negotiations on a future UK-EU trade agreement. It is worth remembering that—pursuant to GATS Art. II:1—external services trade policies are applied on an MFN basis, thus any preferential access to the EU market that the UK might seek would need to be part of a comprehensive agreement. Otherwise, pursuant to GATS Art. V the EU would be obliged to immediately extend the conditions granted to the UK to all other WTO members, which is rather unlikely.

Within that future agreement, whatever form it might take, a roadmap for the UK’s negotiating agenda could probably be derived by squaring the currently applied policies per sector and mode with the specific export interests of UK firms as evidenced by trade flows under relatively undistorted Single Market conditions. Apart from negotiating the terms of market access and national treatment for services, the mutual recognition of professional qualifications and, indeed, the mutual accreditation of regulatory agencies would be a separate negotiating matter.

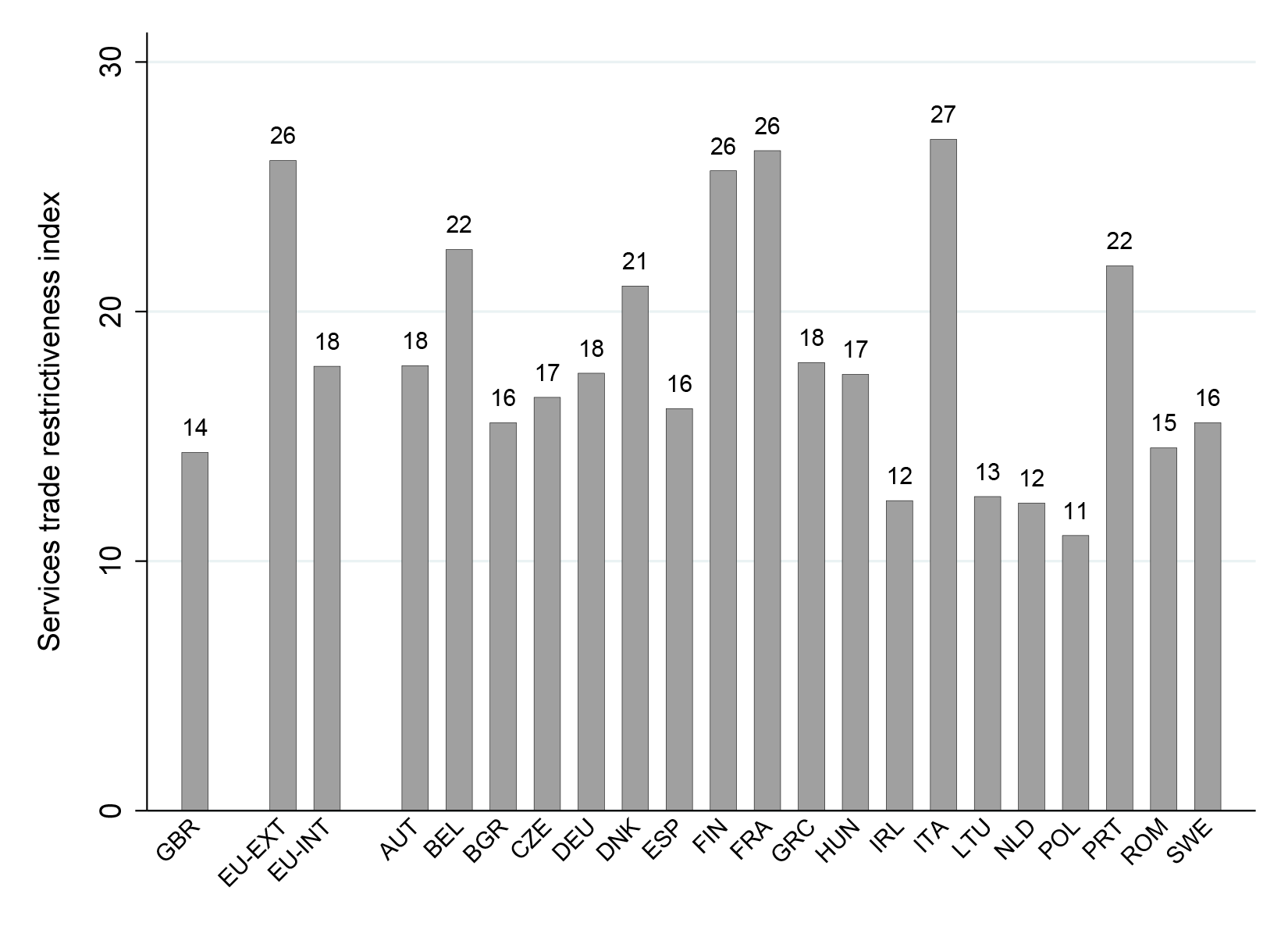

Information from the World Bank’s Services Trade Restrictions Database (STRD) sheds some light on the varying degree of openness in major services sectors across 20 of the 28 EU member states, including the UK (Figure 1).[15] The Services Trade Restrictiveness Index (STRI) depicted in Figures 1 and 2 aims at capturing the restrictiveness with respect to services trade of a country’s applied policy regime, based solely on available policy information.[16] Because of the Single Market and the four freedoms, EU member countries are distinctly more open vis-à-vis each other compared to non-EU countries. In order to capture the two-tiered nature of policies in this context, the STRI score for individual EU countries represents a trade-weighted measure of openness; since EU countries trade a lot with each other, their STRI scores are typically driven by the more open preferential policies. In contrast, the artificial entity “EU-EXT” captures EU member countries’ average policy towards non-EU providers, whereas “EU-INT” is a simple average of EU-internal policies.

Figure 1: Trade Policy Restrictiveness: country-level STRI scores

Source: World Bank Services Trade Restrictions Database

The quantification using STRI scores affords at least a qualitative picture of differences in services trade policies across EU countries and sectors (Figure 1). First, average external restrictiveness (26) is higher than policy barriers within EU members (18). Second, there is a good deal of variation in applied policies across EU countries, with the UK being amongst the most liberal members on average. Thirdly, the overall scores shown in Figure 1 are primarily driven by investment policies (mode 3), partly because mode 3 is quantitatively important and partly because of the incidence of policy measures affecting investment.

The country-level scores shown in Figure 1 obfuscate the fact that the picture is rather different in professional services sectors, in which trade restrictions arise mostly from regulation on the movement of natural persons as service suppliers (mode 4). Here policies across the 20 EU members are appreciably more restrictive (STRI scores ranging between 50-60) and more diverse. In this particular area, Britain’s score of 60 is slightly higher than the internal average (57). Policy restrictions on mode 4 are prevalent despite the free movement of persons as stipulated by the Single Market. Legislative actions such as the Mutual Recognition of Professional Qualifications directive did go some way towards facilitating mode 4 trade, therefore an exit from the Single Market would be likely to have substantial ramifications for the ability of service professionals to move to or from EU-27 countries.

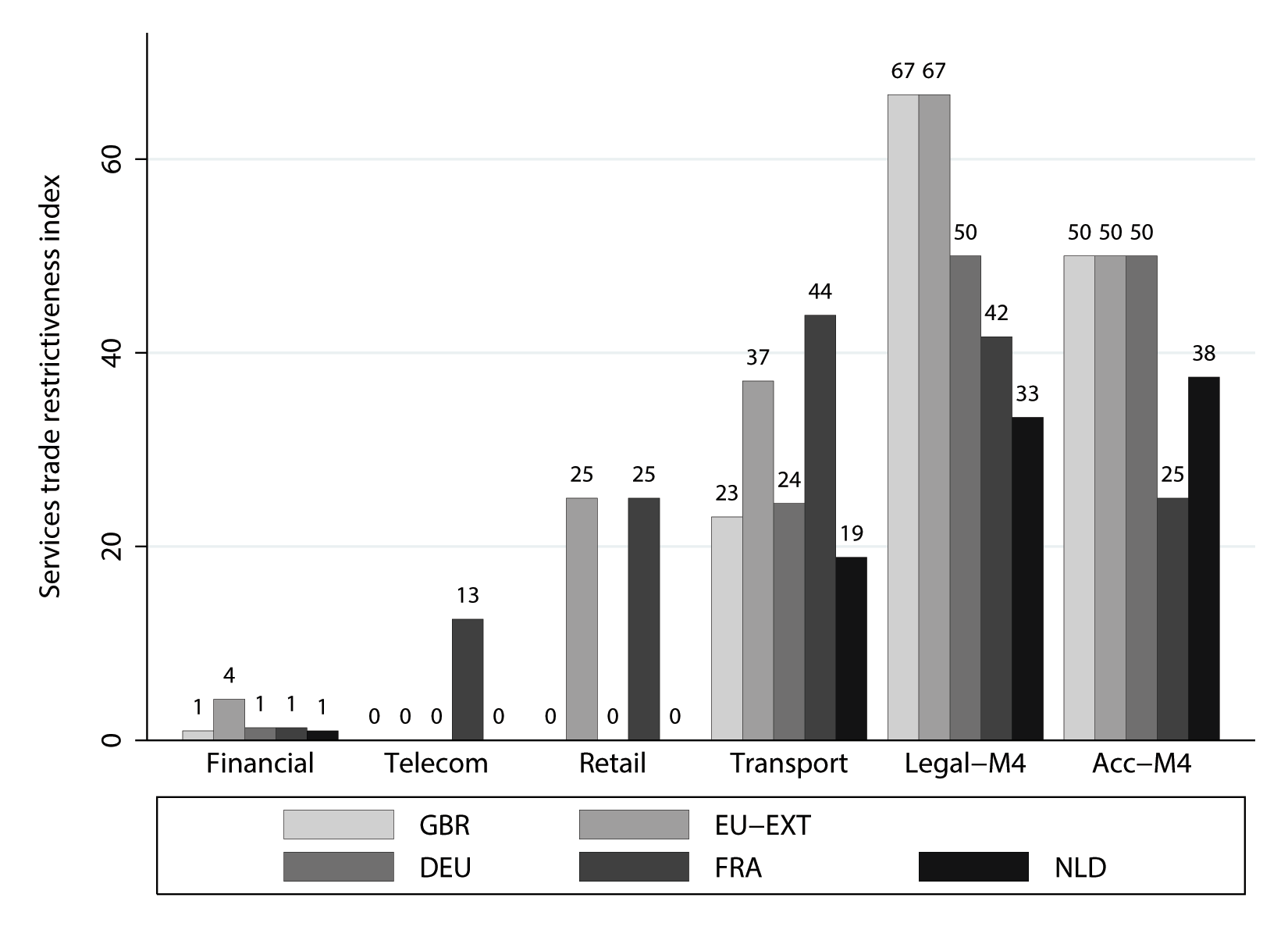

A first impression about the differences in market access within the EU can be obtained by juxtaposing policy restrictiveness across major services sectors (Figure 2).[17] The average external EU’s regime and the UK’s policies are set against those of three adjacent and large economies (Germany, France and the Netherlands). Several observations can be made: EU economies are generally fairly open in financial services, telecoms and retailing, both vis-à-vis each other and towards non-EU providers. It is in professional services sectors (and to a lesser extent transportation) where access for foreign providers is restricted. That said, there are differences across countries: for instance, in transportation sectors the UK imposes the same minor restrictions as the other EU countries depicted (ranging from 19-25) but providers from outside the EU face more restrictions (37). That wedge is even more pronounced in the legal and accountancy professions (via mode 4). Lawyers and accountants looking to provide such services in the EU are up against major restrictions (67 and 50, respectively). Whilst the UK individually is as restrictive as the EU’s external regime, other markets such as France and the Netherlands tend to be more open for service professionals from within the EU. These advantages to UK service suppliers would potentially be lost post-Brexit if “EU-EXT” policies were applied to UK firms.

Figure 2: Trade Policy Restrictiveness, by sector

Source: World Bank Services Trade Restrictions Database

With respect to services trade and investment, the UK has preferential access to a range of foreign markets through bilateral or plurilateral agreements that the EU has negotiated in the past on behalf of its membership. The number of Preferential Trade Agreements (PTA)[18] for services is not as large as the number of merchandise goods FTAs. Still, the consideration that the UK would lose its preferential access to these markets after it left the EU applies in like manner to services and investment too.[19] Currently, there are 14 services agreements in operation that the EU has concluded with third countries or blocs, including South Korea, Mexico, Chile and Central America.[20]

In addition, a trade and investment agreement with Canada (CETA) has just been completed and awaits ratification. The prevailing legal view is that post-Brexit the UK would not be able to continue as party to these agreements and would need to renegotiate.[21] Given the relative geographic and language proximity between the UK and Canada, it is not inconceivable that an EU without the UK fundamentally alters the attractiveness of the deal from Canada’s perspective; of course this depends on the yet-to-be-determined future relationship between the UK and EU-27. It could provide a taster of a broader squall line if other countries felt that Brexit unfolded in a way that impairs their existing rights or commercial advantages. Conversely, though, if properly managed CETA could provide a template for dealing with this unprecedented situation in other bilateral and multilateral settings.

Going forward, the EU is currently engaged in negotiations with nine bilateral (trade and) investment agreements including the largest players such as the United States, Japan, Indian and China. In particular, negotiations with China aim at replacing the 26 existing Bilateral Investment Treaties between individual EU member states and China by one single comprehensive investment agreement. This is an example of a case in which the UK is going to miss out on the EU’s hefty bargaining power when forging an agreement. If these negotiations came to fruition, the remaining 27 EU members would transition to a new agreement whilst post-Brexit, the UK would be left with its 1986 BIT with China. The UK could of course aim at negotiating an upgrade too, but the balance of negotiating power in this bilateral relationship would be rather different.

Currently, the European Commission is also acting on behalf of its members in the plurilateral Trade in Services Agreement (TiSA) negotiations. The UK would presumably want to (re-)take its place as a standalone member in that forum after leaving the EU. Whilst TiSA is formally open to all WTO members, access does not appear to be automatic (China is understood to be interested in joining but has not yet become part of the talks). Again, this would suggest that the UK will have to rely on some goodwill for continued access to the single most important plurilateral forum for services trade negotiations. In any event, meaningful engagement therein will require staff resources and expertise previously provided by the EU Commission.

The UK is also party to about 180 bilateral treaties with investment provisions,[22] some 31 of which are not—or not yet—in force. For instance, Economic Partnership Agreements (EPAs) or other Association Agreements currently under negotiation all pass for BITs in UNCTAD’s comprehensive inventory.[23]

Trade in services across its various modes of supply—cross-border trade, consumption abroad, investment, and movement of service professionals—constitutes a substantial part of UK international trade, particularly with respect to the EU. Whilst the financial sector is arguably an area of specialisation in the UK, there is a host of business services such as legal advice, engineering, marketing or consulting for which as a whole the value of cross-border trade, in fact, exceeds that of financial services.

Overall, the UK runs a sizable trade surplus in cross-border services trade, even though the share of services imports coming from the EU is larger than the share in overall UK services exports that goes to the EU. That is, the UK exhibits a comparative advantage in services and the EU is one of its most important export markets. At the same time, UK businesses benefit from the import of a range of business services as inputs into both the services and the manufacturing sector, respectively.

The UK services sector has continuously deepened its integration into international production fragmentation, with the value added shares of domestic and foreign services inputs into UK total exports each having grown by 7 percent every year over the past two decades. Partly as a result of this process, more than half of the value added of UK total exports consists of domestic services (as of 2011), underpinning the crucial role of services for export performance.

Going forward negotiations with the EU should seek to preserve the conditions that currently sustain this favourable situation. Services trade, including investment and the temporary movement of persons as service suppliers, is salient for the performance of the UK’s manufacturing base and its trade competitiveness.

Brexit will entail a change in the conditions under which UK businesses trade with the EU. For services, gauging the extent of market access conditions is difficult because:

1. There are distinct regulatory frameworks—and political sensitivities—for cross-border trade, investment, and movement of people, respectively;

2. The EU’s services trade policies applied to non-EU countries are typically more liberal than what the EU GATS commitments would prescribe, across all modes of supply;

3. There is no uniform EU services trade regime for third country suppliers to begin with. Access to individual EU markets for UK service providers is likely going to change in a way that differs across EU member states, sectors, and modes of supply. Access to foreign markets other than the EU is also going to change insofar as the UK will most likely cease to be party to preferential services trade agreements that were concluded by the EU in the past, such as EU-Korea or, going forward, CETA.

GATS

The WTO’s General Agreement on Trade in Services. The GATS came into being during the Uruguay Round of trade negotiations and entered into force in January 1995. Since January 2000, services have become the subject of multilateral trade negotiations.

GATS commitments

Are legally binding commitments inscribed in WTO Members’ GATS Schedule of Specific Commitments. Schedules identify the services for which a Member guarantees market access and national treatment and any limitations that may be attached. Commitments are undertaken with respect to each of the four different modes of service supply. Most Schedules consist of both sectoral and horizontal sections. The “Horizontal Section” contains entries that apply across all sectors subsequently listed in the schedule.

Modes of supply

Because many services are not storable, effective exchange (trade) of a service may require the proximity of supplier and consumer. Thus it has become customary in the terminology of the GATS to take a broad view of trade in services to include not just cross-border trade but also international transactions through foreign investment or the movement of people. The different ways of trading services are known in GATS parlance as the four ‘modes of supply’:

Mode 1 – Cross-border: services supplied from the territory of one country into the territory of another, without either supplier or buyer/consumer moving to the physical location of the other. Example: a blueprint or presentation sent electronically from India to the UK.

Mode 2 – Consumption abroad: services supplied in the territory of one country to a resident of another country who moves to the location of the supplier(s). Example: tourism; a UK student going to France to study.

Mode 3 – Commercial presence: Legal persons (firms or any type of business) moving to the location of consumers to sell services locally through the establishment of a foreign affiliate or branch (often foreign direct investment). Example: Retailers Lidl or Aldi opening shops in the UK.

Mode 4 – Presence of natural persons: services supplied by natural persons resident in one country in the territory of another by (temporarily) moving to the country of the consumer(s). Example: A US lawyer travelling to the UK for 3 months to discharge legal advice.

Trade in services

Exchange of services between residents of two different countries. Compared to merchandise goods, services have unique characteristics that affect their tradability. The two most obvious characteristics include intangibility and non-storability. In addition, services typically also require differentiation and joint production, with consumers having to participate in the production process. In order to capture these aspects and to allow for trade in services that also require joint production, the WTO defines trade to span four modes of supply. In terms of global values, services trade represents about 20% of total trade (on a balance of payment basis), even though services account for over 60% of global production and employment in most countries. Due to measurement issue and the multiple modes of supply, official statistics are thought to severely underestimate the value of services trade.

Service trade policy

Any legislative measure that has the potential to affect trade in services. Such regulatory measures could be de jure non-discriminatory or discriminatory. In the former case, all suppliers irrespective of ownership are subject to the regulation (e.g. all banks have to have a certain amount of paid-up capital) whereas the latter applies to foreign suppliers only (e.g. foreign insurance companies may not sell life insurance). Service trade policies could also be categorised by mode of supply, or whether they affect market entry of new suppliers or rather operations of incumbent suppliers.

Ingo Borchert, Batshur Gootiiz and Aaditya Mattoo (2014), “Policy Barriers to International Trade in Services: Evidence from a New Database”, World Bank Economic Review 28(1), pp. 162-188.

Lucian Cernat and Zornitsa Kutlina-Dimitrova (2014), Thinking in a Box: A ‘Mode 5’ Approach to Service Trade, Journal of World Trade 48 (6), pp. 1109–1126.

Marcel Timmer, Abdul Azeez Erumban, Bart Los, Robert Stehrer and Gaaitzen de Vries (2014), “Slicing Up Global Value Chains”, Journal of Economic Perspectives 28 (2), pp. 99-118.

This document was written by Ingo Borchert. Very helpful comments were gratefully received from Alan Winters, Peter Holmes and an anonymous referee. Any remaining errors are the author’s.

Ingo Borchert asserts his moral right to be identified as the author of this publication. Readers are encouraged to reproduce material from UKTPO for their own publications, as long as they are not being sold commercially. As copyright holder, UKTPO requests due acknowledgement. For online use, we ask readers to link to the original resource on the UKTPO website.

_________________________________________________________________________

[1] This Briefing Paper focuses primarily on cross-border services trade (‘mode 1’) and establishing commercial presence (‘mode 3’) as the quantitatively dominant conduits of services trade. Consumption abroad (‘mode 2’) is important mainly in sectors such as tourism, healthcare and education. The temporary movement of service professionals (‘mode 4’) is closely tied to a country’s overall immigration/visa policies, and such trade as might occur is notoriously poorly captured in official statistics. Even before the Brexit vote, in which “regaining control over immigration” was a major theme, both the UK and other European countries have traditionally been applying rather restrictive policies, and this is unlikely to change in the future.

[2] ‘Other commercial services’ exclude the categories of Travel, Transportation and Government services, respectively, for which the notion of a trade balance is not as straightforward to interpret.

[3] This share rises to nearly 50% if Switzerland is included, which is a major destination for UK financial services exports.

[4] Comprising of ‘technical, trade related, operational leasing and other business services.’

[5] Source: ONS Statistical Bulletin – Foreign Direct Investment Involving UK Companies: 2014

[6] Source: UNCTAD World Investment Report 2016, country fact sheet United Kingdom, 2015 figures.

[7] See Cernat and Kutlina-Dimitrova (2014), Figure 5.

[8] Mode 2 does not seem practical in this regard but modes 1, 3 and 4 are all potential avenues for obtaining such services from abroad.

[9] See Timmer et al. (2014), Table 4.

[10] Source for all figures in this section: United Kingdom profile “Trade in Value-Added and Global Value Chains”, based upon the OECD-WTO TiVA Database and available from the WTO website: https://www.wto.org/english/res_e/statis_e/miwi_e/GB_e.pdf

[11] The top three GVC-importing industries are chemicals, motor vehicles, and petroleum products, respectively.

[12] Specific commitments in the GATS are undertaken in terms of market access (Art. XVI) and national treatment (Art. XVII). The former refers to the absence of quota-type restrictions such as limitations on the number of service suppliers, on the total value of service transactions, or on the number of service operations or natural persons that may be employed, amongst others. National treatment refers to non-discrimination accorded to services and service suppliers of any other countries in respect of all measures affecting the supply of services.

[13] Countries that newly acceded to the WTO post-1995 typically made broader and deeper GATS commitments as part of their overall accession negotiations.

[14] Thus named in analogy to the ‘binding overhang’ that exists for tariff rates on goods.

[15] All information contained in the STRD can be accessed at http://data.worldbank.org/data-catalog/services-trade-restrictions. In principle the Database focuses on countries’ MFN policies as of 2009.

[16] The STRI score is constructed by assessing policy regimes for each subsector-mode combination in their entirety, and assigning values on an openness scale from zero to 100 in intervals of 25, with zero denoting ‘completely open’ and 100 denoting ‘completely closed’ (ie. no entry allowed at all). STRI scores are aggregated to the country level using appropriate sets of modal and sectoral weights, respectively. For further details see Borchert et al. (2014).

[17] The STRI scores for the two professional services sectors, Legal and Accounting/Auditing, depict policy restrictiveness with respect to the movement on natural persons (mode 4).

[18] There is a range of terms used to denote agreements that have provisions relevant for services trade and investment, including Services Economic Integration Agreements (EIAs) or Bilateral Investment Treaties (BITs), and individual agreements such as CETA or TTIP that feature investment provisions.

[19] See UKTPO Briefing Paper #2: http://www.sussex.ac.uk/bmec/documents/briefing-paper-2.pdf.

[20] The full list includes: Albania, Bosnia and Herzegovina, CARIFORUM States (EPA), Central America, Chile, Colombia and Peru, FYR Macedonia, Georgia, Rep of Korea, Mexico, Montenegro, Rep of Moldova, Serbia and Ukraine.

[21] Eg. Sir Alan Dashwood QC, Cambridge University, in testimony to the HoC Foreign Affairs Committee. See http://data.parliament.uk/writtenevidence/committeeevidence.svc/evidencedocument/foreign-affairs-committee/the-costs-and-benefits-of-uk-membership-of-the-eu/oral/25756.pdf.

[22] Mostly BITs but also FTAs, EPAs or Association Agreements where relevant. The number does not include such entries as the EC Treaty, the EC-EFTA Agreement, or the Energy Charter Treaty.

[23] UNCTAD Investment Policy Hub, http://investmentpolicyhub.unctad.org/IIA/AdvancedSearchBITResults (accessed 28 Sept 2016).