8 July 2020

8 July 2020

Dr Minako Morita-Jaeger, International Trade Policy Consultant and Fellow, UK Trade Policy Observatory at the University of Sussex.

Japan and the UK launched the Japan-UK Free Trade Agreement (FTA) negotiation on 9th June. The two governments agreed to “work quickly to make the new partnership as ambitious, high standard, and mutually beneficial as the EU-Japan Economic Partnership Agreement”.[1] As negotiations accelerate, there are three fundamental issues to consider when assessing the deal.

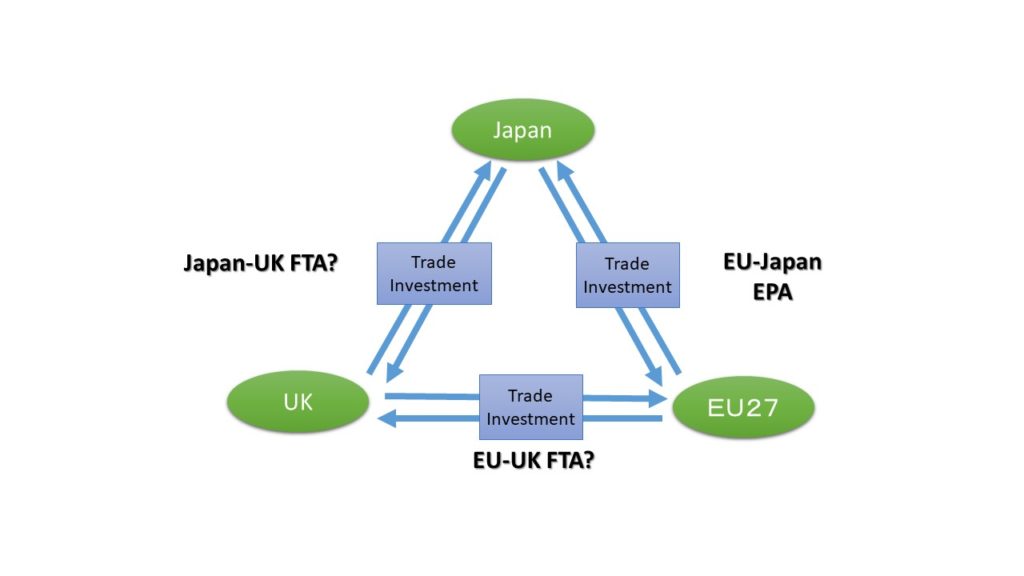

Although the Japan-UK FTA is a bilateral trade agreement, it cannot be disconnected from the EU-UK future trade deal. The Japan-UK bilateral relationship constitutes one side of the EU-Japan-UK trilateral relationship because many Japanese and UK firms are engaged in Global Supply Chains (GVCs) and regional supply chains in Europe. (Figure 1).

This trilateral relationship is especially important for Japanese business. It is widely known that Japanese firms established the business model of using the UK as a hub for business in Europe, or as a gateway to Europe, based on the UK being an EU Member state. Japanese companies, especially manufacturers, are currently under great pressure to reshape their business model because frictionless trade between the EU and the UK will end on 31st December 2020. The prospect of the EU-UK FTA on 1st January 2021 is completely uncertain. According to a Japanese business survey (2019), the top concern of Japanese companies doing business in the UK and the EU is the EU-UK FTA. Notably, border frictions created by new border controls and customs procedures; tariff rates; and ending the free movement of people are listed as the factors that impact most heavily on Japanese business in Europe. Given that these factors threaten their day-to-day business, their interests in the Japan-UK FTA are overshadowed.[2]

This trilateral relationship is especially important for Japanese business. It is widely known that Japanese firms established the business model of using the UK as a hub for business in Europe, or as a gateway to Europe, based on the UK being an EU Member state. Japanese companies, especially manufacturers, are currently under great pressure to reshape their business model because frictionless trade between the EU and the UK will end on 31st December 2020. The prospect of the EU-UK FTA on 1st January 2021 is completely uncertain. According to a Japanese business survey (2019), the top concern of Japanese companies doing business in the UK and the EU is the EU-UK FTA. Notably, border frictions created by new border controls and customs procedures; tariff rates; and ending the free movement of people are listed as the factors that impact most heavily on Japanese business in Europe. Given that these factors threaten their day-to-day business, their interests in the Japan-UK FTA are overshadowed.[2]

Whilst the EU-UK future trade deal is outside the scope of the Japan-UK FTA negotiation, a successful EU-UK future trade deal can be seen as a prerequisite to prosperous Japan-UK trade and investment relations.

2. The Japan-UK FTA for investment

If Japan and the UK aim to achieve a truly “ambitious” and “mutually beneficial” FTA, it should be designed to serve investment for the following reasons.

First, Japan and the UK have a strong investment relationship. For the UK, Japan’s investment stock in the UK is the second-largest among non-EU countries after the US and the 6th largest (5.9%) if we include the EU members and the UK Offshore Islands.[3] For Japan, the UK is the second-largest foreign direct investment (FDI) destination following the US. It is important to note that Japanese investment to Europe has been concentrated in the UK, accounting for almost 40% of total FDI stock.[4]

From the UK perspective, Japanese companies are an important source of employment, creating 130,000 jobs in the UK (2018).[5] What is not well known yet is the role of foreign-owned companies in UK exports, especially in services. More than half of UK services exports (£74.6 billion) are generated from foreign-owned firms including Japanese firms. For example, foreign-owned manufacturing firms in the UK, such as the automotive, chemical and pharmaceutical industries, generated £8.8 billion in services exports.[6] These are the sectors where Japanese firms have been investing. Given that Japan is the largest investor abroad in the world (14% of the world total in 2018),[7] whether the post-Brexit UK can continuously attract Japanese investment must be a highly critical issue for the UK economy.

Second, the investment section of the EU-Japan EPA covers only investment liberalisation.[8] During the EU-Japan EPA negotiation, the EU and Japan could not agree on investment protection and investment dispute settlement. Although the issue was part of continuing negotiations towards a future investment agreement, its prospects look gloomy. This is because the EU is promoting the Investment Court System while Japan prefers the Investor-State Dispute Settlement (ISDS). Improving the investment chapter by including investment protection and investment dispute settlement is exactly what the UK and Japan could prioritise if both governments aim to achieve an EU-Japan EPA-plus agreement. The issue is also important if the UK is to join the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) in the future. The CPTPP has a comprehensive stand-alone investment chapter containing ISDS provisions. The UK could use the Japan-UK FTA as a stepping-stone for its future accession to the CPTPP.

Third, Japanese business shows a strong interest in concluding a bilateral investment treaty (BIT) with the post-Brexit UK. Given that Japanese firms have been exposed to Brexit-related uncertainty since the EU Referendum in 2016, they have a strong desire to ensure legal certainty.[9] Although the UK has 92 BITs in force, no investment treaty exists between Japan and the UK.[10] For example, the UK has a BIT with Korea containing ISDS.

Since the early 1990s, states have been actively incorporating investment provisions into FTAs to promote investment liberalisation and investment protection. Since the EU-Japan EPA does not have a comprehensive investment chapter and there is no BIT between Japan and the UK, both governments have to prioritise improving investment rules in order to secure existing investment and providing incentives towards future investment.

3. A balance between “continuity” and the level and scope of “ambitions”

The Japanese and UK governments aim to enter the Japan-UK FTA into force on 1st January 2021 without any interruption after the transition period. The Japanese Government expressed the necessity to complete the bilateral negotiations by the end of July, in order to fit the outcome into its domestic legislative process. This allows the two governments less than two months to negotiate a deal.

The big challenge here is how to achieve their “ambitions” and “continuity” within an unprecedentedly short negotiating time-frame. There are high-level political pressures for achieving “continuity”. For the UK Government, there is growing expectation to make the Japan-UK FTA the first successful trade agreement for the post-Brexit UK – given that the political prospect of concluding the UK-US FTA this year is becoming very thin. For Japanese and UK business, continuity of the EU-Japan EPA is critical to avoid disruption of supply chains. On the other hand, the Japanese Government rejected a continuity agreement with the UK in the first place in order to make an FTA that directly mirrors the Japan-UK bilateral trade and investment relations and interests.

Then how to strike a balance? Trade negotiations can be categorised into market access negotiations and rule-making. In the case of the Japan-UK FTA, market liberalisation in goods and services cannot be expected except for some outstanding issues (e.g. accelerating the schedule of tariff eliminations) for three major reasons.[11] The first reason is that Japan does not have an incentive for further liberalisation than what it has accorded to the EU. Japan negotiated the EU-Japan EPA when the EU was 28 countries, including the UK itself. The economic reality that the UK market is much smaller than the EU market inevitably lessens Japan’s appetite for further market access negotiation. Second, the Most Favoured Nation (MFN) provisions in the EU-Japan EPA legally limit Japan’s capacity to commit to a higher level of market liberalisation with the UK than it has provided to the EU. According to the MFN provisions, if Japan accords a higher level of liberalisation to a future FTA partner, this should be unconditionally shared with the EU.[12] Third, the negotiating time-frame is too short to do serious market access deals.

The above envisages that rule-making beyond the EU-Japan EPA should play a pivotal role in creating value in the Japan-UK FTA. In addition to investment, improving e-commerce and digital trade would be mutually beneficial and a possible area to enhance. Unfortunately, there will not be enough time to upgrade the services trade chapter. The UK and Japanese services markets are de-facto open and business interests may fall into the category of domestic regulatory issues, such as mutual recognition and equivalence. Negotiations for these issues are time-consuming and cannot be done without the participation of domestic regulatory authorities.

In short, it is highly likely that both governments will have to downgrade their “ambitions” in order to achieve “continuity”. The Japan-UK FTA seems likely to end up with very limited improvements relative to the EU-Japan EPA.

[1] The Japan-UK Foreign Ministers’ Strategic Dialogue 2020, Joint press statement (8th February 2020),

[2] “Oushuu shinshutu nikkeikigyou jittai chousa” (in Japanese). JETRO, December, 2019 https://www.jetro.go.jp/world/reports/2019/01/fe6334f4e426937e.html.

[3] Source: ONS.

[4] Source: JETRO Investment data.

[5] Source: Ministry of Internal Affairs and Communications, Japan.

[6] “Foreign Investment as a Stepping Stone for Services Trade” https://blogs.sussex.ac.uk/uktpo/2020/06/11/foreign-investment-as-a-stepping-stone-for-services-trade/

[7] Source: UNCTAD.

[8] The EU-Japan EPA, Section B: Investment liberalisation (Article 8.6-8.13)

[9] Keidanren, “Policy Proposal on Investment Treaties”, October, 2019. https://www.keidanren.or.jp/en/policy/2019/082.html

[10] Japan has only 29 BITs entered in force.

[11] Japan shows strong interest in UK’s immediate elimination of the auto tariffs, which are scheduled to be eliminated in eight years in the EU-Japan EPA. In services, including audiovidual services, which is exempted from the scope of services trade in the EU-Japan EPA, is Japan and the UK’s mutual interests.

[12] See MFN provisions in goods (Article 2.8); cross-border trade in services (Article 8.9); and investment (Article 8.17) in the EU-Japan EPA.

Disclaimer:

The opinions expressed in this blog are those of the author alone and do not necessarily represent the opinions of the University of Sussex or UK Trade Policy Observatory.

Republishing guidelines:

The UK Trade Policy Observatory believes in the free flow of information and encourages readers to cite our materials, providing due acknowledgement. For online use, this should be a link to the original resource on our website. We do not publish under a Creative Commons license. This means you CANNOT republish our articles online or in print for free.

[…] purchase Japanese products, such as whiskey. On the flip side, there is the prospect of creating a trilateral relationship if the UK and EU come to an agreement. Japan would ultimately gain a win and provide more business […]