13 March 2021

Yohannes Ayele is Research Fellow in the Economics of Brexit, Nicolo Tamberi is Research Officer in Economics, and Guillermo Larbalestier is Research Assistant in International Trade at the University of Sussex. All are Fellows of the UKTPO.

Yohannes Ayele is Research Fellow in the Economics of Brexit, Nicolo Tamberi is Research Officer in Economics, and Guillermo Larbalestier is Research Assistant in International Trade at the University of Sussex. All are Fellows of the UKTPO.

On Friday 12 March, the Office for National Statistics (ONS) and HM Revenue and Customs (HMRC) released the UK’s trade in goods figures for January 2021, providing data for the first month following the end of the Brexit transition period. The ONS has provided their own interpretation of these data portraying a rather gloomy scene for UK trade. We have downloaded the raw data and here offer some initial thoughts on what we learn from the changes in trade flows in January 2021.

A few considerations should be kept in mind when analysing these monthly data. First, the Coronavirus pandemic affected trade, irrespective of the trade partner. For this reason, we compare UK-EU trade with the UK’s trade with the rest of the world (ROW). Second, adjustments to shocks can take some time to materialise, so the figures for January 2021 should be interpreted with caution. Third, firms have been stockpiling in the last few months of 2020, hence a reduction in January 2021 trade figures could be a consequence of stockpiling. Fourth, the methodology with which UK-EU trade data are collected changed in January 2021.

Finally, it is important to note that interpreting high-frequency trade figures can be challenging because monthly trade data can fluctuate considerably. In their analysis of the data, the ONS compared January 2021 with the preceding year. Arguably, however, January 2020 was also not a ‘normal’ month/year given the state of play of Brexit negotiations. In order to try and account for such volatility together with the effect of the Coronavirus pandemic, in our calculations we compare the value of trade for January 2021 with the average value of trade in the preceding three years (ie. January 2018, 2019 and 2020). We also compare the change in UK trade with the EU, with changes in trade with non-EU countries.

Our calculations show that total exports to the EU fell by 46.5% in Jan 2021 compared to average exports of Jan 2018-20, while exports to non-EU countries fell by 9.5% over the same period. These are dramatic changes. On the other hand, UK imports from the EU were down by 29.3% with imports from non-EU countries down by 17.7%, month-on-month. Comparing the impact on UK trade with the EU and non-EU countries goes some way to accounting for the differences in the impact on trade arising from the UK’s exit from the EU, and the impact of COVID-19.

Not surprisingly, there is clear evidence here of a Brexit effect. The fact that UK exports to the EU appear to be more affected than imports from the EU should also not be particularly surprising. While UK exports to the EU are now subject to border inspections, the UK has a light touch regime on imports from the EU at least until June-July of this year.

Table 1: UK total exports

| Partner | Average Jan 18-20, £m | Jan 2021, £m | Change (%) |

| Non-EU | 14,168 | 12,824 | -9.49 |

| Total EU | 14,392 | 7,706 | -46.46 |

| World | 28,560 | 20,530 | -28.12 |

Table 2: UK total imports

| Partner | Average Jan18-20, £m | Jan 2021, £m | Change (%) |

| Non-EU | 20,075 | 16,530 | -17.66 |

| Total EU | 21,181 | 14,983 | -29.26 |

| World | 41,256 | 31,513 | -23.62 |

Looking across EU partners, UK exports fell the most towards the three largest EU members: France (-56.8%), Italy (-56.6%) and Germany (-49.2%). On the other hand, UK exports to the US fell by 21.1% and exports to China dropped by 8.5%. We also observe an increase in UK exports to Japan (+7.5%), Canada (+1.6%) and Australia (+0.8%). On the other hand, imports from the US saw the largest drop (-38.7%), followed by Germany (-35%) and France (-34%). The only country (of the 15 largest trade partners) from which UK imports increased is China (+17.1%). All figures are computed comparing Jan 2021 to the average of Jan 2018-20.

We now turn to a more disaggregated analysis and look at the number of industries that saw a decline in exports and imports in January 2021 relative to the average of Jan 2018-20. We base this on trade classified by the so-called Harmonised System (HS) at the HS 2- and 4-digit levels. At the HS 2-digit level there are 97 industries in total, and at the HS 4-digit level there are 1221 industries.

Table 3 shows that a very high share of UK industries saw a decline in exports and imports to/from the EU. Hence the changes observed above are not simply concentrated in a few industries or sectors but are widespread. Therefore, at 4-digit level, 1041 industries out of 1221 saw trade decline. Secondly, we see that the number of industries that saw declines in exports to and imports from the EU is higher than with respect to the rest of the world. To partially consider the possibility of stockpiling in the months of November and December 2020, we also perform similar calculations comparing the average level of exports and imports of the last three months (Nov 2020 – Jan 2021) with the average of the last three years for the same months. This calculation shows a similar trend: more products saw a decline in export to the EU than to the RoW. This gives some indication of the initial impact of the changes in trading arrangements that came into force in January 2021.

Table 3: Number of industries that saw a decline in Jan 2021 relative to the average of Jan 2018-20

| Status | HS4 (#) | HS2 (#) | |

| EU | Exports | 1041 | 96 |

| Imports | 1058 | 88 | |

| Non-EU | Exports | 778 | 65 |

| Imports | 819 | 71 |

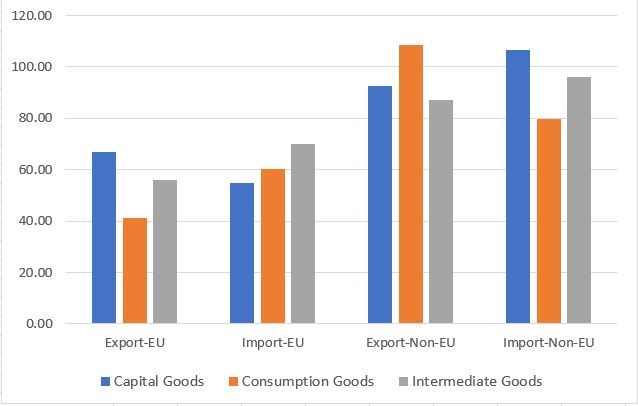

Classifying goods as capital goods, consumption goods and intermediate goods also reveals similar trends. Figure 1 shows that the level of exports of capital goods, consumption goods and intermediate goods is significantly lower compared with exports of the same category of goods to the rest of the world. For example, the UK’s exports of intermediate goods in January 2021 was below 60% of the average level of export of the last three years, and exports of consumer goods is only around 40% of what it was previously. These are very substantial changes in trade.

Figure 1: Level of trade in Jan 2021 relative to the average of Jan 2018-20 by type of goods

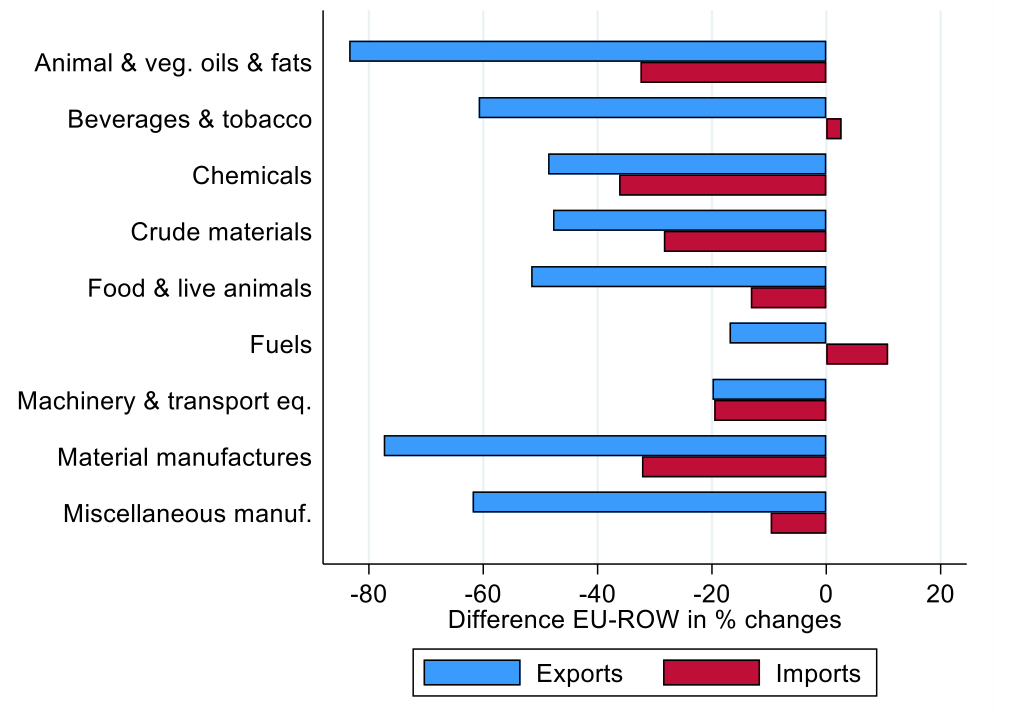

Figure 2 then considers the changes across sectors[1]. The figure shows the difference in the percentage changes in exports (in blue) and imports (in red) between the UK and the EU, and the percentage change in export (and imports) between the UK and the rest of the World. Take the first entry in the figure which is for Animal & vegetable oils and fats. In this sector, UK exports to the EU declined by 60%, while UK exports to ROW increased by 26%. Hence the difference between these two changes is 86%

Figure 2 provides a rapid way of assessing the extent to which the changes in UK trade with the EU in January 2021 is different to the change in trade with non-EU countries. What we see is that there are indeed substantial differences – and once again this gives prima facie evidence of short-run Brexit effects. Relative to non-EU exports, the most affected sectors appear to be Animal & vegetable oils & fats, Material manufactures and Miscellaneous manufactures. For imports, the most affected sector is Chemicals, followed by Animal & vegetable oils & fats and Material manufactures. On the other hand, Fuels and Beverages & tobacco imports from the EU performed better than from non-EU sources.

Figure 2: Difference in EU-ROW % changes by SITC, Jan2021 relative to average Jan2018-20

|

| The table shows the difference between % changes over Jan2021 relative to the average Jan2018-2020 in trade with the EU relative to trade with non-EU (a difference-in-differences). This is computed as where y is either exports or imports. The measure displayed on the horizontal axis is expressed in percentage points. |

We have also identified the industries, defined at the SITC 2-digit level, in which the changes in trade flows are the biggest in absolute terms.[2] Ranking the industries by those with the biggest absolute change in the value of trade with the EU (as always comparing January 2021 with the average export values of the previous three years) then the sectors with the largest effects were petroleum products (SITC33, -£1.2 bn), road vehicles (SITC78, -£0.7 bn) and pharmaceutical products (SITC54, -£0.6 bn). Out of the 20 products that saw the largest falls in export values, eight products can be categorised into machinery & transport equipment, four into the chemicals category, six are material and miscellaneous manufactures and food & live animals and fuels account for one product each.

The same approach applied to the value of imports from the EU in January 2021 (compared to the average import values of the previous three years), shows that road vehicles (SITC78, £1.4 bn), pharmaceutical products (SITC54, £0.8 bn) and telecommunications equipment (SITC76, £0.34 bn) were the products that saw the largest declines in import values. Considering the top 20 products with the largest negative values, six are products of machinery & transport equipment, four are in material manufactures, five are of miscellaneous manufactures, two in each of chemicals and food & live animals, and one in fuels.

An alternative approach is to consider which industries saw the biggest percentage fall in trade with the EU. While these sectors may be smaller and thus have a smaller aggregate effect on UK trade, the impact on the sectors themselves is much more substantial. The products with the biggest percentage changes in export values to the EU are fish and crustaceans (SITC 03, -83%), oil seeds (SITC22, -80%), footwear (SITC85, -77%), sugar and honey (SITC06, -76%), and animal oils and fats (SITC41, -73%). Looking at percentage changes in imports from the EU, and excluding products labelled as ‘unspecified’, the largest adverse percentage changes were for animals oils and fats (SITC41, -60%), pulp and waste paper (SITC25, -59%), travel goods (SITC83, -59%), pharmaceutical products (SITC54, -50%) and petroleum products (SITC33, -48.4%).

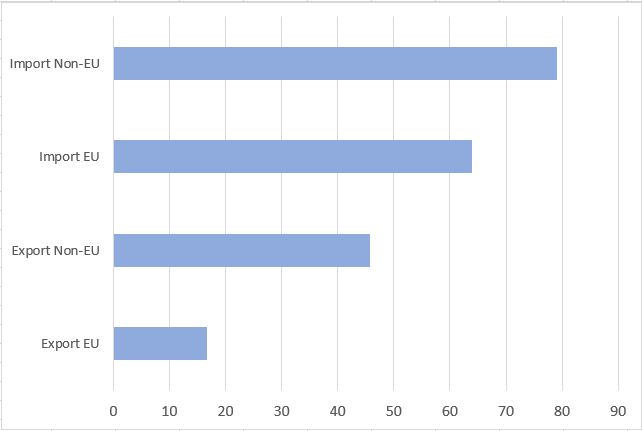

Finally, because disruption to the fisheries industry has received substantial coverage in the press over the last two months, we provide some figures for this more narrowly defined sector.[3] Figure 3 shows level of fish import and export in Jan 2021 relative to the average of Jan 2018-20. While there are no substantial differences in the change in imports by the UK from the EU and Non-EU , we see that exports to the EU saw a dramatic fall in January 2021 (more than 80% of the average of Jan 2018-20) , which bears out the reports in the press from the fishing industry.

Figure 3: Level of reduction of fish (HS03) trade in Jan 2021 relative to the average of Jan 2018-20

The changes we observe in this data are dramatic and worth underlining: UK exports to the EU in January 2021 were nearly 47% lower than the average of the preceding three years, and imports were nearly 30% lower. This is unprecedented. Some of this is because of COVID – but that is probably a small part of the story because, for example, exports to the rest of the world only declined by 10%. Some of this is temporary – the initial decline is no doubt bigger because of the stockpiling in November and December and because traders are likely to adjust to the new bureaucratic regimes – so the negative impacts will lessen. However, some of this will be very long-lasting and was not an inevitable consequence of the UK leaving the EU. It is an inevitable consequence of the manner in which the UK has left the EU, and of the nature of the Trade and Cooperation Agreement signed with the EU.

[1] This is based on the Standard International Trade Classification (SITC) at 1-digit level, excluding SITC 9.

[2] In this case we did not compare changes in trade with EU with changes in trade with non-EU countries.

[3] This is defined at the HS 4-digit level as HS 0307

Disclaimer:

The opinions expressed in this blog are those of the author alone and do not necessarily represent the opinions of the University of Sussex or UK Trade Policy Observatory.

Republishing guidelines:

The UK Trade Policy Observatory believes in the free flow of information and encourages readers to cite our materials, providing due acknowledgement. For online use, this should be a link to the original resource on our website. We do not publish under a Creative Commons license. This means you CANNOT republish our articles online or in print for free.