23 March 2021

23 March 2021

Michael Gasiorek is Professor of Economics and Director of the UK Trade Policy Observatory at the University of Sussex. Suzannah Walmsley is Principal Consultant and Fisheries and Aquaculture Business Development Manager at ABPmer.

Last week the UK’s trade data for January 2021 came out and the evidence was pretty striking. It showed a dramatic decline in UK exports and imports in January, and particularly so with the EU. Now some of this will have been driven by Covid-related lockdown restrictions, and some of the dramatic fall in trade with the EU itself may have been driven by firms’ stockpiling in November and December to protect themselves against the much-publicised potential border difficulties arising from the UK’s exit from the EU and the end of the transition period.

In this blog we dig a bit deeper into those numbers and focus just on fisheries. There are two reasons for looking at fisheries. Firstly, this was a sector that was politically contentious and difficult to resolve in the negotiations, and the second is that as much of what is exported is fresh, chilled or live, the issue of stockpiling is much less of a factor. It is worth noting that the EU–UK Trade and Cooperation Agreement (TCA) brought with it more regulatory autonomy for the UK with regard to fisheries management, and resulted in a transfer of quotas in favour of the UK of the order of 25% of the value of EU catches from UK waters. Nevertheless, the UK Government obtained much less in the agreement than the industry had hoped for and de facto the changes negotiated for many species and fishing communities will not make much difference (see Trade Bites podcast for a fuller discussion).

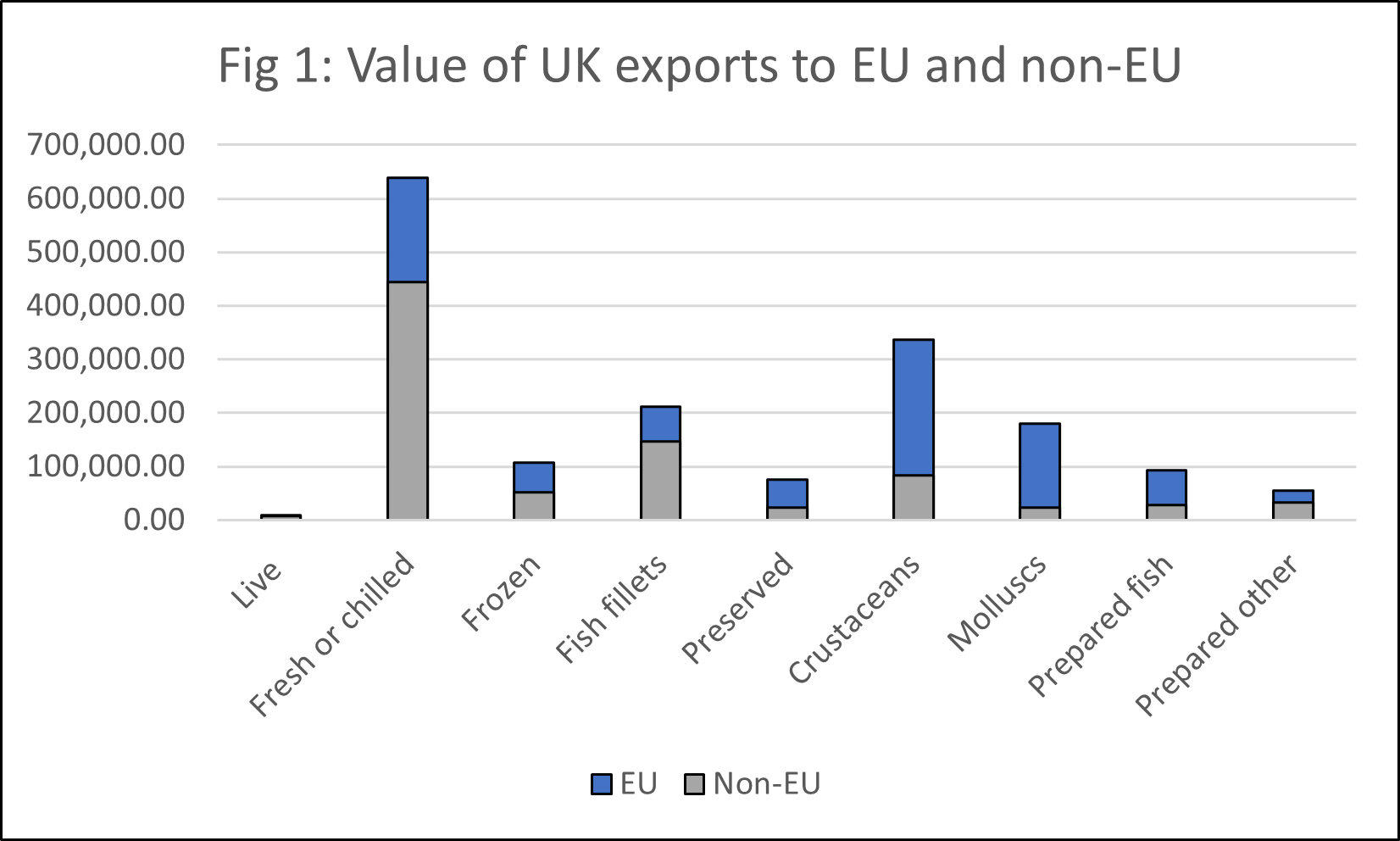

First, consider the chart below, which gives the value of UK exports to the EU and non-EU countries for the main fish categories as they appear in the trade data for 2019 (source: Comtrade). From this we see that the majority of exports are fresh or chilled fish and 60% of UK exports go to the EU. Indeed, for each category at least 55% of exports go to the EU, and in some cases, such as molluscs, over 85% is exported to the EU. This serves to underline the importance of the EU market to the UK industry.

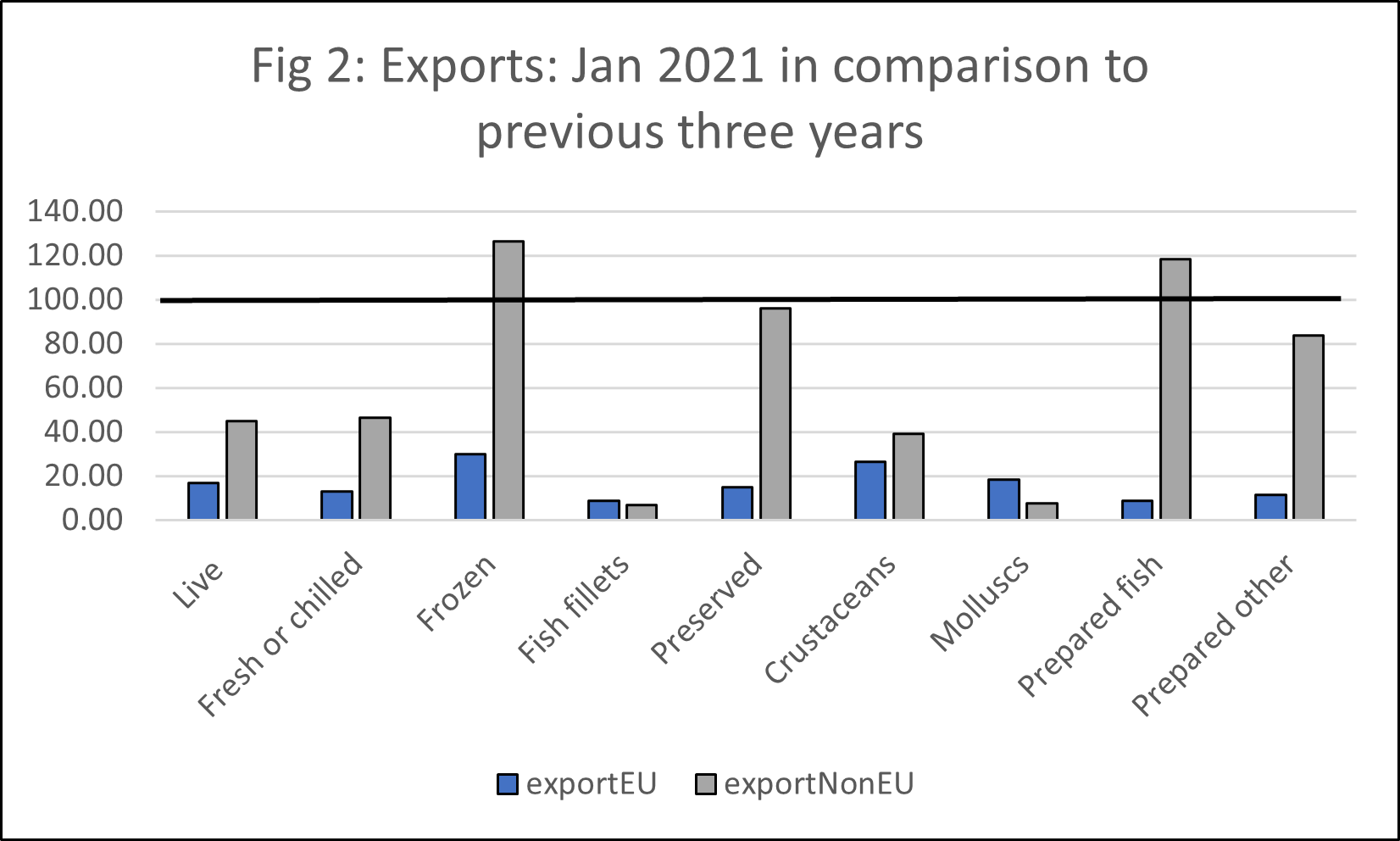

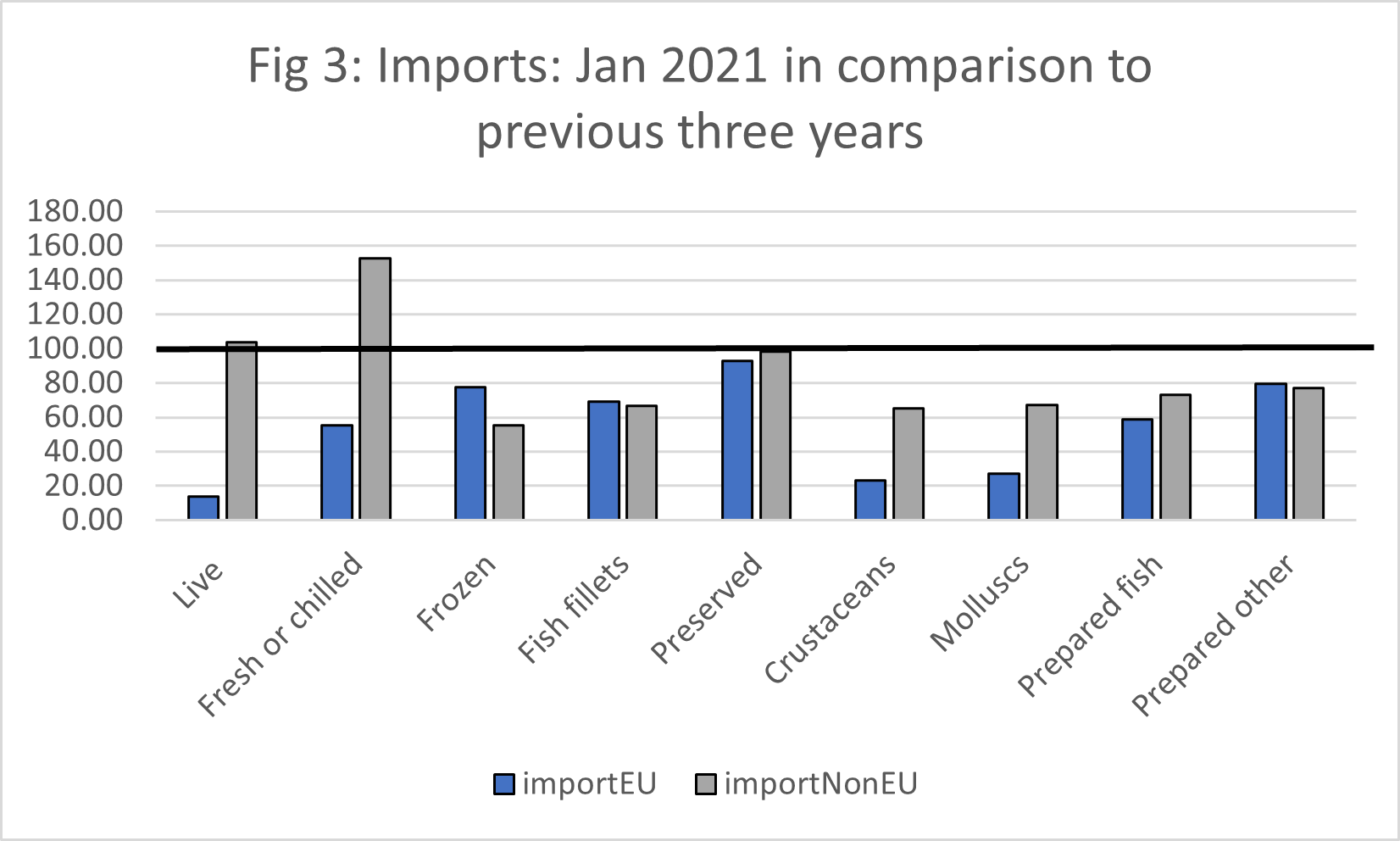

The impact on January fish trade arises from the end of the transition period and the treatment of the UK as a ‘third country’ trading with the EU. This has both raised the bureaucratic and administrative requirements and hence costs of trade with the EU, and also, in some cases, resulted in a ban on UK exports (for bivalve molluscs like mussels and clams, depending on which waters they were caught in). The impact on UK trade for different categories of fish can be seen in the two charts below. The first is for exports and the second is for imports. These give the ratio of UK trade in January 2021 relative to the average January trade over the preceding three-year period (2018-20). Note the last two categories refer to processed fish products either with regard to fish (prepared fish), or other products such as molluscs and crustaceans (prepared other). If trade in January 2021 had stayed level in comparison to the preceding year, then in the graph the ratio would be 100. Hence wherever the bar chart is less than 100 this indicates a decline in trade.

The charts indicate the collapse particularly in exports to the EU in January 2021. Trade was more than 80% lower for live fish, fresh or chilled fish, fish fillets, preserved fish, molluscs, and both categories of processed fish and fish products. There is some evidence of a slightly smaller impact for frozen fish, which may be because of a degree of stockpiling. Although not shown in the graph, if we take all the more detailed categories for salmon, the data indicates that salmon exports were down by over 96%. Such falls in trade are – to put it simply – unprecedented. It is interesting to see that in most cases the fall in exports to the EU is significantly higher than the fall to non-EU countries – except for molluscs and fish fillets which saw an even bigger decline in exports to non-EU countries. However, with regard to molluscs only a very small share of exports goes to non-EU countries and these monthly exports fluctuate considerably; also the decline in fish fillet exports to non-EU countries occurred much earlier during the first lockdown in March-April 2020 and never recovered; and this is also true of crustaceans. The overwhelming evidence therefore is of a Brexit-induced collapse in exports, possibly exacerbated by Covid effects causing reduced demand in European markets.

The fall in imports is smaller, but nevertheless substantial, especially with regard to all the fresh categories of fish and marine products, with a decline in fresh fish products by more than 40% and crustaceans and molluscs by around 75%. On the face of it, the UK has not introduced additional controls / measures on imports from the EU, and so one might have thought there would be no impact. The data suggest that trade in January was constrained on all sides, as UK and EU exporters may have avoided trading in either direction as they were expecting possible disruptions at the border with new control and administrative requirements. The disruption and problems that were observed in the initial days/weeks may have had a knock-on impact on non-EU trade, as vessels were tied up because of lack of access to markets, resulting in a general reduction in supply.

The next few months will be revealing as to the extent to which trade will pick up and the extent to which the problems in January were simply ‘teething’ problems. No doubt that is part of the explanation – however, it is likely that even these short-term teething problems, in addition to the higher longer-term bureaucratic costs, may have a painful impact on the seafood industry.

Disclaimer:

The opinions expressed in this blog are those of the author alone and do not necessarily represent the opinions of the University of Sussex or UK Trade Policy Observatory.

Republishing guidelines:

The UK Trade Policy Observatory believes in the free flow of information and encourages readers to cite our materials, providing due acknowledgement. For online use, this should be a link to the original resource on our website. We do not publish under a Creative Commons license. This means you CANNOT republish our articles online or in print for free.

[…] Gasiorek, Suzannah Walmsley. "A Fine Kettle of Fish" — UK Trade Policy Observatory, March 23, […]