What are rules of origin and why they are needed?

Which sectors may be more vulnerable to tight rules of origin?

Proposals for UK negotiating priorities

Over the past few years, the importance and intricacies of international trade have entered the public debate much more than ever before. With the negotiations over a Free Trade Agreement (FTA) with the EU, and also with the UK launching FTA negotiations with countries such as the US, Japan, and Australia, the term ‘rules of origin’ has even entered the public lexicon. In this Briefing Paper, we outline what rules of origin are, why they are needed, why they are complex, and which sectors in the UK may be most vulnerable to more restrictive rules of origin. We also discuss why the EU is highly unlikely to agree to the UK’s proposal on cumulation of rules of origin.

Rules of origin (RoOs) are used to determine the country of origin of a traded good. The origin of a good is not determined by the place it was shipped from but instead depends on where ‘production’ occurred. As many goods contain imported inputs, it becomes important to determine the minimum level of domestic activity needed for the good to be deemed as originating in a particular country. To reflect the fact that different industries have very different production processes, RoOs are often defined at a very detailed product level.

There are many reasons why determining the origin of a good is needed. For example, in order to correctly apply trade remedy measures such as anti-dumping duties or countervailing duties, or to administer tariff-rate quotas. In Free Trade Agreements, RoOs play a particularly important role. For a good to be eligible for the preferential treatment afforded by an agreement, it must be shown to originate in one of the parties of the agreement. This is to prevent trade deflection, whereby third countries (i.e. those not party to the agreement) export to the FTA partner with the lowest external tariff, and then ship the products on to other FTA partner(s) tariff-free, thereby circumventing the higher tariffs of the final destination country. For this reason, FTAs contain preferential rules of origin, which are typically specific to each agreement.

Currently, the UK applies the EU’s Common External Tariff (CET) as well as the EU’s Common Commercial Policy. This means that a good coming in from outside the EU faces the same tariff irrespective of whether it enters through the UK or from somewhere else in the EU. Hence there is no need for goods shipped between the UK and the EU to show originating status. This will change after the transition period, when the UK will have its own tariff schedule. The UK Global Tariff (UKGT), published in May 2020, differs from the EU’s CET in a number of ways, and overall around 60% of all detailed tariff lines have been reduced in the UKGT compared to their current levels under the EU’s CET.[1] Any trade agreement between the UK and the EU will, therefore, need to include rules of origin.

Each FTA has its own RoOs and is thus bespoke. Hence, the rules of origin agreed between the EU and Canada are different to those agreed between the EU and Japan. One notable exception to this is the EU’s Pan Euro-Mediterranean Rules of Origin (PEM).[2] The PEM aims to consolidate the different bilateral rules of origin that the EU has with its neighbours – the members of the European Free Trade Association (EFTA), the 10 countries which are part of the Barcelona Process, and the 6 countries of the EU’s Stabilisation and Association process in the Balkans – into the common PEM framework. Given that the PEM provides a set of RoOs that the EU has agreed with a wide range of near neighbours, plausibly the UK could either potentially negotiate to be part of the PEM system, and/or the PEM provides some indication of what the EU may be prepared to negotiate.

There are typically four types of conditions or criteria that are used to determine whether or not a good is deemed as ‘originating’:

In practice, for any given product the rules often contain combinations of the above. This might mean that two requirements both need to be met – for example that the VA rule needs to be satisfied and the CTC rule. Or, there may be a choice of meeting either one rule or another – for example, you can get originating status either by satisfying the CTC rule, or by satisfying the VA rule. The former is typically more constraining, the latter introduces more flexibility into the rules.

In order to see the relative importance of rules and their combinations, Table 1 below gives the incidence of the different criteria used to determine originating status in the Pan-Euro-Mediterranean (PEM) rules of origin. The calculation is done at the detailed HS 6-digit level of disaggregation, for which there are around 5,200 products, which have subsequently been aggregated into broader sectoral groupings.[3]

In the first four columns of the table, we give the incidence for each sectoral grouping of each of the main criteria where it is the sole criterion being applied. Hence in the first column we see, for example, in Automotives, there is a sole value-added rule which applies in 78% of cases. In contrast for chemicals, only 21% of the 6-digit product lines have a sole value-added rule, whereas 8% of cases have a sole CTC rule, and in 1% there is a specific production process rule. This means that for Chemicals a sole rule is only applied in 30% of cases.

In the final two columns of the table, and for each of the industry groupings we give the incidence of the more common alternative combinatory rules that are applied. Note that there are more than twelve types of combinatory (i.e. ‘and’ / ‘or’ ) rules which are used in the PEM. Hence, and staying with Chemicals, for 66% of product lines there is a choice between a value-added or a CTC rule. In contrast for Textiles, the dominant rule is the SP rule. Conversely, if we look at Advanced Manufacturing and Machinery, Automotives, or Other Transport Equipment, the dominant sole rule is the value-added rule, and the rule which is “CTC & VA, or VA” is also widely used. Similarly, if we consider Prepared Foodstuffs, the sole rules in total apply in only 50% of the product lines, and the use of the value-added rule and the CTC rule applies for 18% of the products (and not shown in the table another 16% are covered by being wholly obtained or a specific production process rule).

Overall, the CTC rule either on its own or in combination with other rules applies to 48% of product lines, and the VA rule either on its own or in combination applies in 49% of tariff lines, the SP rule for nearly 21% of all tariff lines, and being wholly obtained in 14%.

| Sector | VA | CTC | SP | WO | Other | Description |

| Agriculture | 1% | 0% | 1% | 83% | 13% | WO & VA |

| Prepared Foodstuffs | 4% | 21% | 4% | 21% | 18% | CTC & VA |

| Mineral Products | 1% | 77% | 5% | 0% | 17% | CTC or SP |

| Materials | 4% | 57% | 24% | 0% | 12% | CTC & VA |

| Chemicals | 21% | 8% | 1% | 0% | 66% | CTC or VA |

| Pharmaceuticals | 5% | 70% | 2% | 0% | 23% | CTC & VA |

| Textiles | 1% | 12% | 65% | 0% | 18% | SP, or VA & SP |

| Adv. Manuf. and Machinery | 42% | 0% | 0% | 0% | 57% | CTC & VA, or VA |

| Automotive | 78% | 0% | 0% | 0% | 20% | CTC & VA, or VA |

| Other transport equipment | 45% | 0% | 0% | 0% | 15% | CTC & VA, or VA |

| Manufacturing and Electronics | 47% | 10% | 0% | 0% | 38% | CTC & VA, or VA |

| Total | 17% | 20% | 17% | 11% | 35% | Combination of above |

Source: Own calculations

The table makes clear just how complex the determination of the rules of origin can be. In an FTA, these are typically negotiated at the detailed product level (such as the HS 6-digit). How they are set can impact on the degree of protection / liberalisation offered to a given industry. A high domestic value-added rule encourages greater use of domestic inputs and hence serves to protect the domestic input industry.[4] Indeed, in the recently re-negotiated USMCA (US-Mexico-Canada agreement), the rules of origin for automobiles were set at a high level for this reason. Conversely, to the extent that strict rules raise the costs for final producers it may make them less competitive either domestically or internationally. Given that rules of origin can be used to protect domestic (supplying) industries, it is not surprising that industries may seek such protection by lobbying for more constraining rules of origin.

Table 1 gives the relative incidence of the different rules in the PEM but does not indicate the share of UK trade that may fall under the different categories. An indication of this can be seen in Table 2. The calculations are based on the HS 6-digit level of disaggregation and we count the share of UK trade with the EU for which each of the four criteria is used – either solely or in combination with one of the other criteria – so they don’t sum to one hundred. If we take Processed Foodstuffs a CTC rule applies solely or in combination in around 50% of product lines but when it comes to the value of trade, the CTC rule applies for over 70% of trade. Indeed, the CTC rule is particularly important for Processed Foodstuffs, Mineral products, Materials, Pharmaceutical products, Advanced Machinery and Manufacturing and other transport equipment. The VA rules are important for Chemicals, Advanced Manufacturing, Automotive, and Manufacturing and Electronics.

| CTC rule | VA rule | SP rule | WO rule | |

| Agriculture | 0.0% | 7.0% | 0.4% | 94.9% |

| Processed Foodstuffs | 71.5% | 30.4% | 6.5% | 57.5% |

| Mineral Products | 99.9% | 0.0% | 96.3% | 0.0% |

| Materials | 76.0% | 16.5% | 32.9% | 0.0% |

| Chemicals | 56.1% | 93.0% | 9.1% | 0.0% |

| Pharmaceutical products | 99.3% | 75.7% | 0.4% | 0.0% |

| Textiles | 12.2% | 27.3% | 70.9% | 0.0% |

| Advanced Manufacturing and Machinery | 69.3% | 100.0% | 0.0% | 0.0% |

| Automotive | 2.5% | 100.0% | 0.0% | 0.0% |

| Other transport equipment | 95.2% | 100.0% | 0.0% | 0.0% |

| Manufacturing and Electronics | 48.9% | 94.6% | 3.5% | 0.0% |

| Total | 59.7% | 62.0% | 23.5% | 6.4% |

Note: categories are not mutually exclusive (one product can have both a CTC and VA rule), therefore the categories do not sum to 100%. Source: Own calculations.

It is also important to note that both the CTC rule and the VA rule could be determined at different levels of aggregation, and the level of aggregation impacts on the ease/difficulty of meeting the rule of origin. In the EU’s Pan-European Mediterranean (PEM) the CTC rule is in most cases defined at the HS 4-digit (heading) level. For example, the general rule for salt, stone, plastering materials, lime and cement (chapter 25) is “Manufacture from materials of any heading, except that of the product”.[5] Generally, the broader the level of aggregation at which the CTC rule is defined the more difficult it may be for a firm to meet it. There is a small proportion of products in Processed Foodstuffs (less than 4%) which are defined at the tariff line level, and in Pharmaceuticals the share defined at the tariff line level is close to 15%.

The value-added rule is often expressed in terms of ‘all materials’.[6] For example, the general rule for vehicles (chapter 87) states “manufacture in which the value of all the materials used does not exceed 40 % of the ex-works price of the product”.[7] However, the value-added rule can also be applied at a disaggregated level. Hence, the origin rule for chapter 8 (Edible fruit and nuts) states, in addition to requiring that all the fruit and nuts used are wholly obtained, that “the value of all the materials of Chapter 17 used does not exceed 30 % of the value of the ex-works price of the product”. In other words, there is a limit on the amount of inputs from chapter 17 that can be used to produce products under chapter 8. Similarly, the rule for other base metals, wrought (under HS chapter 81) is expressed at an even more detailed level, stating “Manufacture in which the value of all the materials of the same heading as the product used does not exceed 50 % of the ex-works price of the product”.

Hence instead of specifying that a good is deemed as originating if the value of all imported inputs is less than x% of the price of the good, a rule might specify that the value of imported inputs from a given HS chapter or 4-digit category has to be less than x% of the price of the good. The relative incidence of the use of the VA rules at different levels of aggregation is given in Table 3 below. Hence for Materials, in 28% of the cases, the VA rule is specified at the 4-digit level, and in Prepared Foodstuffs, in 91% of cases, the VA rule is specified at the 2-digit level.

| Category | All materials | Chapter | Heading | TARIC | Mixed |

| Agriculture | 23% | 75% | 2% | 0% | 0% |

| Prepared Foodstuffs | 0% | 91% | 9% | 0% | 0% |

| Mineral Products | 100% | 0% | 0% | 0% | 0% |

| Materials | 72% | 0% | 28% | 1% | 0% |

| Chemicals | 87% | 0% | 1% | 0% | 11% |

| Pharmaceuticals | 100% | 0% | 0% | 0% | 0% |

| Textiles | 3% | 0% | 0% | 0% | 96% |

| Adv. Manuf. and Machinery | 100% | 0% | 0% | 0% | 0% |

| Automotive | 100% | 0% | 0% | 0% | 0% |

| Other transport equipment | 100% | 0% | 0% | 0% | 0% |

| Manufacturing and Electronics | 99% | 0% | 1% | 0% | 0% |

| Total | 77% | 5% | 3% | 0% | 15% |

Cumulation of rules of origin is a term which is used to define the extent to which a country can count intermediate inputs from another country as equivalent to its own in determining origin. There are several forms of cumulation that could be agreed in an FTA:

Bilateral cumulation: Suppose the UK and the EU sign an FTA with bilateral cumulation of rules of origin and there is a product where the rule of origin states that there has to be a minimum of 40% domestic value-added.

Suppose that currently the amount of value-added from within the UK for the good is 30%, and that intermediate imports from the EU also comprise 30% of the value of the final good. Bilateral cumulation means that the UK producers can count the EU’s intermediate inputs as part of the determination of originating status. Hence, the amount of ‘domestic’ value-added here would be 30% (UK) + 30% (inputs from the EU) = 60%. As this is above the threshold of 40%, the final good is deemed as originating and so can enter the EU duty-free.

Without bilateral cumulation, if the UK exported the good to the EU, there would be only 30% domestic value-added for this good, which is less than the threshold and hence the final good would face tariffs on exports to the EU. Almost all FTAs agree on bilateral cumulation.

Diagonal cumulation: Suppose the UK has an FTA with the EU and another FTA with Korea. Taking the same example as earlier, now suppose that the UK is buying the intermediates, which account for 30% of the value of the final good, from Korea. Diagonal cumulation would mean that the UK could include the 30% Korean input for originating purposes when exporting the final good to the EU. So, again, the UK would have a total of 60% originating value-added, which is above the 40% threshold and so can export the final good duty-free to the EU.

In this example, Korean imported inputs count for originating status. However, whether the imported intermediate has been produced in Korea (i.e. ‘originates’ in Korea) will be determined by the rules of origin in place in the agreement between the UK and Korea. This raises the possibility that the UK and Korea could agree on very lax rules of origin (e.g. that only 10% domestic value-added is required). This would make it much easier for an intermediate input to be considered as Korean when exported to the UK, to be used in the production of a final good being exported to the EU. So, agreeing very lax rules of origin between the UK and Korea could give the UK a competitive advantage in the EU market.

In order to prevent this, for diagonal cumulation to be agreed, it is normally the case that each of the three countries needs to have bilateral FTAs with the others and the rules of origin between UK-Korea, UK-EU and EU-Korea need to be exactly the same. This is precisely the motivation behind the PEM system described earlier. Countries that are members of the PEM system all have identical rules of origin (the PEM rules of origin), and this allows for diagonal cumulation. Diagonal cumulation makes it much easier to source intermediate inputs from third countries in order to produce final goods which are then granted the preferential tariffs.

Full cumulation: Full cumulation is an even more flexible version of diagonal cumulation. If we return to the previous example and assume that the rule of origin between the UK and Korea for the intermediate input is that there needs to be a minimum of 40% Korean domestic value-added in the intermediate for that good to be considered as Korean when exported to the UK. Suppose that there is only 35% Korean domestic value-added. In that case when the good is imported by the UK it is not deemed to be Korean (and therefore tariffs would need to be paid on the import). With diagonal cumulation the Korean input cannot be cumulated with the UK inputs when assessing the final good being exported to the EU. The final good would, therefore, be deemed as only having 30% UK value-added, which is below the threshold and hence tariffs would have to be paid when the final good is exported to the EU.

With diagonal cumulation either the entire Korean good is deemed as originating or none of it. In contrast, if ‘full cumulation’ were allowed, this would mean that the UK could include the share that is Korean value-added in the input imported from Korea. That share is 35%, and the intermediate from Korea is 30% of the value of the final good. Hence the Korean element of that is 10.5% (i.e. 0.3 * 0.35). The total amount of originating value-added in the final good is therefore 30% (from the UK) + 10.5% (from Korea) = 40.5%. This is above the threshold and so the final good can be exported to the EU duty-free.

As with diagonal cumulation, for full cumulation to be allowed, each of the three countries needs to have bilateral FTAs and the rules of origin between each of the three countries typically need to be the same (the term sometimes used here is ‘equivalent’). The difficulties of negotiating both diagonal and full cumulation are therefore that they require all parties to have FTAs and to have the same rules of origin. Suppose the UK wanted to diagonally cumulate with the EU and Japan. This could only be possible if the same RoOs were agreed in all three agreement: EU-Japan; UK-Japan; UK-EU. This is a big ask, and it only takes one of the parties to want different rules of origin for the system to no longer be possible. Currently, the main examples of diagonal cumulation are the EU’s PEM system, and diagonal cumulation is also allowed under the EU’s Generalised System of Preferences (GSP).

One solution to those problems is another form of cumulation which, in the EU context, is normally referred to as extended cumulation, but is sometimes also referred to as cross-cumulation:

Extended cumulation: Suppose the rule of origin in the UK-EU FTA, the EU-Korea FTA and the UK-Korea were all different. This would preclude diagonal or full cumulation. Under extended cumulation the UK could use Korean intermediates in exporting a final good to the EU, providing that the definition of what constituted a Korean good is the same as that applied in the agreement between EU and Korea.[8] By applying the EU-Korea rules of origin to the intermediate being used by the UK, the EU would be assuring itself that access to the EU market is determined by the rules of origin set by the EU, and could not be undercut by lax rules of origin between the UK and Korea.[9]

With extended cumulation, it is therefore no longer necessary for the RoOs to be the same between countries. In fact, it is not even necessary for UK and Korea to have a free trade agreement. Extended cumulation is therefore much more flexible.

It is also possible to introduce sectoral extended cumulation. For example, it could be agreed that in the automobile industry the UK could count Korean inputs for origin purposes in its exports to the EU, where the criterion which determines whether or not the input is Korean is determined by the EU-Korea agreement.

The UK’s draft text, perhaps unsurprisingly, does not contain any detail on the proposed rules of origin which the UK would wish to negotiate. However, it does have relevant clauses with regard to cumulation.

The UK is proposing to allow for bilateral cumulation with the EU, and the form of bilateral cumulation which is envisaged here is full bilateral cumulation. This means that even if an EU intermediate product is not itself deemed as originating from the EU, UK firms can count the EU value-added in that product when using the input in a final good being exported back to the EU (Art 3.3, para 2). This is quite common in free trade agreements, such as in the EU’s agreements with Japan, Korea or Canada. [10]

However, we note that in contrast, the EU’s draft Treaty text with the UK only offers bilateral cumulation and not full bilateral cumulation. This is an important difference which will need to be negotiated.

The UK is also proposing to allow for the cumulation of origin with ‘relevant partner countries’ (Art.3.3, para 1) as well as with GSP countries. This proposal appears to be full (diagonal) cumulation, though the term itself is not used in the draft, and hence there is some lack of clarity over this. Additionally, in determining origin for the purposes of the diagonal cumulation, the UK is proposing that for the exports of the UK to the EU the rule of origin will be those the UK has agreed with the third (non-EU) country; and for the exports of the EU to the UK the rule of origin will be those the EU has agreed with the third (non-EU) country. (Art.3.3, para 8).

On the face of it, this opens up the possibility discussed earlier that the UK could have laxer rules of origin than the EU with a given partner, such as Korea, which makes it easier to use Korean intermediates in the production of exports, hence making it more competitive in the EU market. This would no doubt be unacceptable to the EU. However, para 8, needs to be read in conjunction with para 11, which states that such cumulation can only occur where the UK and the EU apply ‘equivalent’ rules of origin with the third country as opposed to identical rules of origin. What is meant by ‘equivalent’ also raises question. The term has been used in other EU FTA agreements such as CETA, which does provide for the (future) possibility of diagonal cumulation where all the relevant FTAs contain ‘equivalent provisions’ (but still will then need agreeing by all the parties).[11] To date, and to our knowledge, while the term equivalent has been used in previous EU agreements, in practice this has meant having identical rules of origin.

In summary, while the EU may (just) agree to full bilateral cumulation, it is very unlikely to agree to full diagonal cumulation, and particularly on the terms set out by the UK.

In this section we look a little more closely at the extent to which the UK and different sectors within the UK may be vulnerable as a result of the introduction of rules of origin in trade with the EU. Here it is worth repeating that as a member of the EU, and during the transition period, the UK is applying the EU Common External Tariff, so there is no need for rules of origin. The UK can use any intermediate from any third country in the production of a final good for export to the EU which then enters the EU duty-free. From January 2021, if there is a free trade agreement between the UK and the EU, then UK exports to the EU will only enter the EU duty-free if they can prove originating status, i.e. that they have been produced in the UK.

It is also important to note that rules of origin apply to each firm and for each product exported. Hence a given firm may export two products A and B to the EU, and it will need to provide originating proof for each of these products. The same products may be exported by a different firm, but be produced in a different way and while one firm may obtain originating status the other firm might not. This also means that it is extremely difficult to ascertain which firms and products within those firms may be vulnerable to the introduction of rules of origin on trade with the EU.

We undertake an initial assessment of ‘vulnerability’ across sectors by considering the extent to which individual UK firms both import and export within the same HS4 heading. To do this we take information at the firm level on how much is being imported and exported at the highly disaggregated HS 6-digit level.[12] For each firm and for each HS 6-digit product that the firm exports we calculate the ratio of HS 4-digit imports to 4-digit exports pertaining to that 6-digit category. Hence, the calculations are a proxy measure for how much the firm imports relative to its exports. The more a firm imports relative to its exports, the more likely it is that the firm is in some way reliant on imported intermediates and therefore may be vulnerable to the introduction of rules of origin. Of course, we do not know in which exported products the imports are being used, and this is critical in determining originating status. But prima facie – the higher this ratio: (a) the more likely it is that there is imported VA in the exports and hence the products may be more vulnerable to the VA rule; (b) the more likely it is that imports and exports are occurring within the same 4-digit category and therefore the product may be vulnerable to the CTC rule.

This HS4 ratio is calculated for every firm, and for every 6-digit product exported by each firm. This can then be aggregated up either to the sectoral level, or to consider the UK’s total exports. If we consider total exports, then for around 58% of the UK’s exports the firm-level HS4 ratio is greater than 50%. This suggests that a relatively high proportion of trade may be vulnerable. This vulnerability could be either because the high HS4 ratios suggest a higher share of imported value-added, or because they reflect imports within the same HS4 category as the exports and hence the firms may be vulnerable to the CTC rule. However, the CTC rule only applies for around 50% of tariff lines and about 56% of the value of the UK’s exports. Conceivably, therefore, up to around 56% of the UK’s exports may be vulnerable to the CTC – though in practice it will of course be lower.

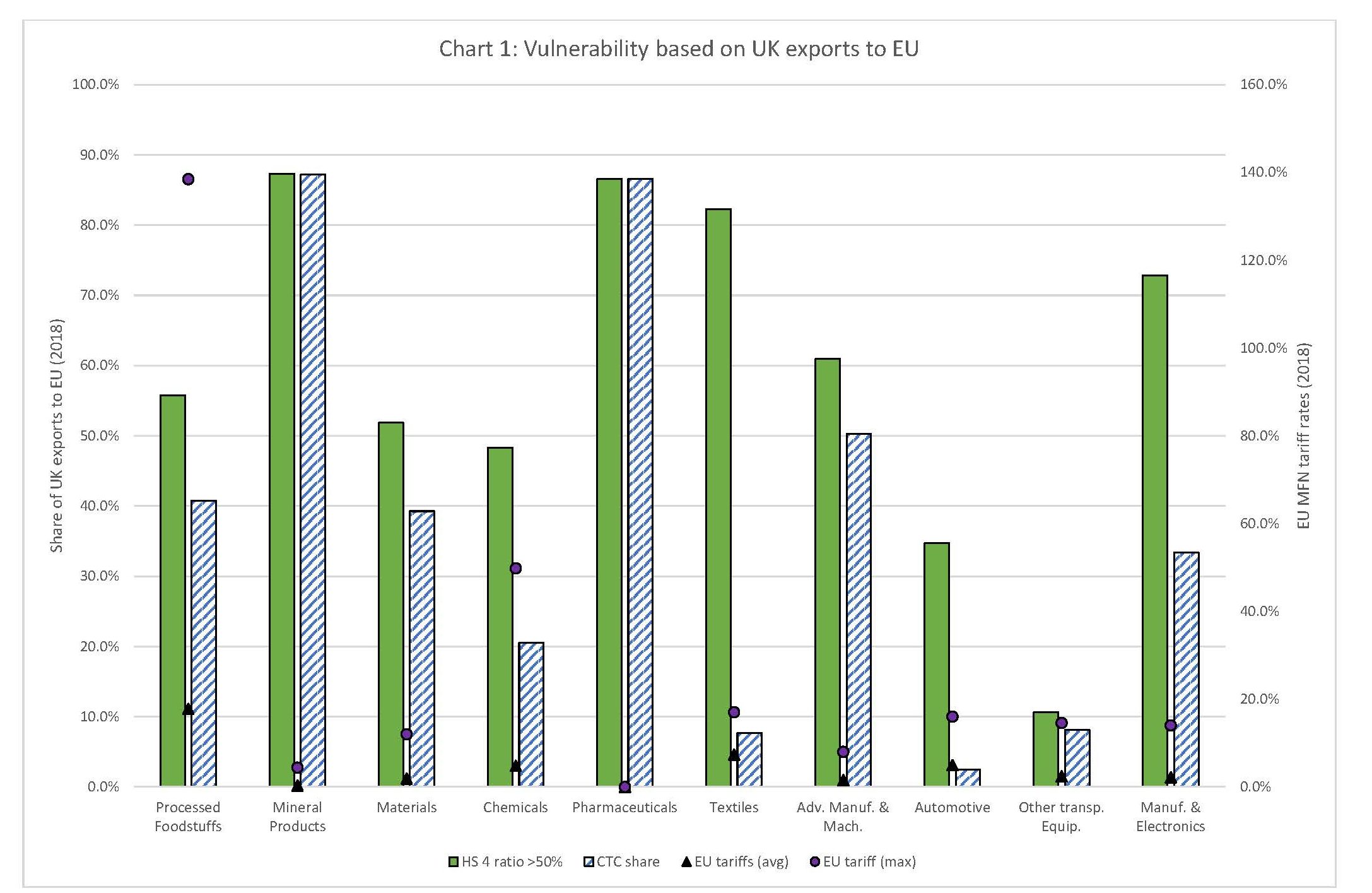

Both the HS4 ratio calculation and the extent of trade vulnerable to the CTC rules can be aggregated to the same broad sectoral groupings used earlier. This information is presented in Chart 1. Again, for each of these sectors we calculate the share of trade where, at the firm level, the HS4 ratio is greater than 50%. Hence for each sector we are capturing the extent to which, for the firms within that sector, their imports are at least 50% of the value of their exports to the EU. The higher this ratio, the more likely it is that the firms in that sector may be vulnerable to either the VA rule or the CTC rule. In the chart, this is given by the height of the green bar – and the higher the bar the more likely it is that firms within that sectoral grouping may be affected.[13] The blue striped bars in the chart give the share of vulnerable trade with the EU in that sector for which the CTC rule applies (either solely or in combination with other rules).

Now in practice, the degree of ‘vulnerability’ will also depend on the height of the EU’s tariff. The reason for this is straightforward. If a firm cannot prove originating status for its exports, then the consequence is that it must pay the EU’s tariff. For a number of goods, the EU’s tariff may be zero, or extremely low, and therefore there is little or no consequence for the firm. Indeed, where the EU’s import tariff is zero, there is no incentive for firms to seek to prove originating status. The higher the EU’s tariff, the greater the possible cost implications for UK firms. The chart also therefore provides information on the sectoral tariff levels – both the average and the maximum tariff applied in that sector.

Source: HS 4 ratios constructed based on HMRC firm level data. Trade data from UN COMTRADE for 2018. Tariff data from UNCTAD TRAINS for 2018, including ad-valorem equivalents.

From the chart, we see that in terms of the HS4 ratio the sectors potentially most vulnerable are Mineral Products, and Pharmaceutical products, and these are also sectors with a prevalent use of the CTC rule. However, for Pharmaceuticals the EU MFN tariff is zero, and hence rules of origin are not likely to be an issue. For mineral products, the average tariff is also extremely low (0.3%), and the maximum tariff is 4.4%. Other sectors which exhibit a high share (over 50%) of imported intermediates relative to exports are Processed foodstuffs, Materials, Textiles, Advanced manufacturing, and Manufacturing and Electronics. Just below 50% we see Chemicals and Automotives. Maximum tariffs are above 10% in Processed Foodstuffs, Materials, Chemicals, Textiles, and Automotives, Other transport equipment, and Machinery and Electronics, suggesting these are sectors where the consequences for individual firms (not necessarily for the sector as a whole) may be more significant.

With its near neighbours, the EU has been keen to agree and apply the PEM. Therefore, one possibility is for the UK to seek this option. There are currently 25 non-EU countries signed up to the PEM,[14] these countries account for 9.2% of UK imports in 2019, and 7.2% of UK exports. This indicates the amount of trade that could have diagonal cumulation if the UK were part of the PEM.

In our view the EU will not agree to any other form of diagonal cumulation, both on principle and because there is not the time for this to be negotiated, and even adherence to the PEM may not be on offer. Outside of the PEM arrangements, the EU has rarely agreed to diagonal cumulation. It is therefore unlikely to do so with the UK. It is also important to note that given the partial diagonal cumulation that the UK has agreed in its trade continuity agreements, there is also less incentive for the EU to agree to diagonal cumulation since its exports to the UK already benefit from the cumulation the UK has agreed with its continuity partners.

So, if the UK decides to eschew the PEM, it is likely to end up with bilateral cumulation of some form with the EU. Theoretically, if there was sufficient trade with third countries, such as the US, Japan, Canada and Korea, and if the UK could then negotiate diagonal cumulation with these third countries, then eschewing the PEM could be preferable. The share of UK exports going to these countries in 2019 was 15.7%, 1.8%, 1.4% and 1% respectively.[15] In terms of the values of trade affected therefore, such a policy would only make sense if it included the US. Remember however, that diagonal cumulation is between three countries – hence this would need to involve the US and another country AND would require the same rules of origin between all three countries. Achieving this is unrealistic.

Hence, unless there is an overriding need in particular sectors for the UK to have bespoke rules of origin with the EU (for example because application of the PEM would result in tariffs on trade for a given sector with the EU) we would recommend that the UK aims to be part of the PEM.

It may also be possible to introduce and to try and negotiate sectoral extended cumulation. For example, it could be agreed that in the automobile industry the UK could count Korean inputs for origin purposes in its exports to the EU, where the criterion which determines whether or not the input is Korean is determined by the EU-Korea agreement. However, once again in our view it is very unlikely at this stage that the EU will be willing to agree this.

If the UK does not wish to or does not manage to agree with the EU to be part of the PEM, it needs to think about how to configure its RoOs to maximise the possibility for firms to be able to use imported intermediates from third countries while maintaining tariff-free access to the EU. From the discussion in Section 2, we infer that the take up of preferences is more likely to be maximized:

In terms of cumulation there is a clear ranking of what would be desirable from least (bilateral) to most (extended) favourable:

There has not been the scope in this Briefing Paper to discuss areas such as ‘de minimis’ and ‘tolerance clause’, nor to discuss the bureaucratic procedures and costs governing rules of origin. But we note that flexibility can be introduced with regard to each of these elements, and we also note that the more the bureaucracy and paperwork underpinning RoOs can be submitted electronically the lower the bureaucratic costs associated with proving originating status.

The conclusions are relatively straightforward: Rules of origin are extremely complex and difficult to negotiate but they do impact on trade flows because they can constrain the extent to which firms can use imported inputs to maximise both their competitiveness with regard to price and quality, while still obtaining preferential access into the partner’s market. Rules of origin are therefore much more than a minor technical issue which needs addressing in an FTA. Because they can be constraining and increase firms’ costs, the aim should be to maximise the possibilities for cumulation – bilateral and diagonal, and to minimise the bureaucratic costs. With regard to diagonal cumulation, in our view, the best the UK could hope for in an FTA with the EU is to obtain diagonal cumulation by choosing to become part of the PEM.

[1] See UKTPO blog https://blogs.sussex.ac.uk/uktpo/2020/05/20/new-tariff-on-the-block-what-is-in-the-uks-global-tariff/

[2] https://ec.europa.eu/taxation_customs/business/calculation-customs-duties/rules-origin/general-aspects-preferential-origin/arrangements-list/paneuromediterranean-cumulation-pem-convention_en

[3] Note that the PEM rules are largely defined at the 4-digit level

[4] With cumulation it may also encourage higher use of partner inputs.

[5] Some products under chapter 25 have specific RoOs that differ from this general rule

[6] While it is referred to as a ‘value-added’ rule, de facto it is typically defined as a share of material inputs.

[7] Some products under chapter 87 have specific RoOs that differ from this general rule

[8] See Augier & Gasiorek (2007) who proposed this as a means of multilateralising regionalism.

[9] For a fuller discussion see: Jerzewska, A., 2018, Brexit and Origin: A Case for the Wider Use of Cross-Cumulation, The E15 Initiative, available online: http://e15initiative.org/publications/brexit-and-origin-a-case-for-the-wider-use-of-cross-cumulation/

[10] For example, the text in CETA states: (1) A product that originates in a Party is considered originating in the other Party when used as a material in the production of a product in that other Party; and (2) An exporter may take into account production carried out on a non-originating material in the other Party for the purposes of determining the originating status of a product. In the text for the proposed agreement with the UK, the EU currently is only offering (1), and not (2).

[11] Art. 3.8-3.10 of the Protocol on rules of origin and origin procedures in CETA states:

[12] The underlying data is based on HMRC firm level data

[13] We have excluded agriculture because of the dominance of the wholly obtained rule

[14] https://www.consilium.europa.eu/en/documents-publications/treaties-agreements/agreement/?id=2010035

[15] Source: UN Comtrade.