Assessing the economic potential from the CPTPP

Political and institutional dilemmas that can arise from expansion

On 16th July 2023, the UK Government announced that it had signed the Protocol of Accession to become a member of the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP). The UK will be the first new member of the bloc and the only member outside the Asia Pacific region and the Americas. The agreement will enter into force after all ratification processes are completed.

Much of the UK Government’s narrative around the CPTPP has been focussed on the economic benefits. The Secretary of State for Business and Trade, Kemi Badenoch, commented that the UK will only see the full benefit of the deal if we use it.[1] In 2021, the CPTPP countries (excluding the UK) accounted for almost 11% of the world’s GDP (US$ 14.3 trillion), 6.5% of the world’s population (512 million), and 14% of world’s exports and imports of goods and services (US$ 7.5 trillion).[2]

However, these benefits are likely to be modest but could rise with future CPTPP expansion. Indeed, the UK Government’s documentation points out that “the more CPTPP expands, the greater the benefits to the UK. This is why we want a seat at the table now”.[3] Perhaps more importantly, joining the CPTPP could represent a geopolitical strategic gain for the UK.

In this Briefing Paper, we consider the potential economic opportunities for the UK arising from the current CPTPP in comparison with the likelihood of further expansion in the future. We first evaluate the UK’s economic opportunities with both current and potential CPTPP members, including trade in goods, trade in services, supply chain relationships and rules of origin. In the analysis, we compare the CPTPP’s policies, with those of current and potential CPTPP members. Then we assess the political economy of CPTPP expansion. Finally, we conclude with some policy suggestions.

The nature of the UK’s bilateral relations with current and potential CPTPP members is shown in Table 1. This indicates that the UK has bilateral FTAs with nine of the countries, and that there are ten countries that have either applied to join or have indicated some interest in joining. Five countries have submitted formal applications to join the CPTPP: China, Taiwan (both in September 2021),[4] Ecuador (December 2021), Costa Rica (August 2022) and Uruguay (December 2022). Another five nations have expressed interest in joining the bloc – South Korea, Thailand, the Philippines, Indonesia and Colombia.

Table 1: The UK’s bilateral relations with current and potential CPTPP members

| Type | Current CPTPP | Potential CPTPP |

| New bilateral FTA | Australia, New Zealand | |

| Continuity Agreement+ | Japan | |

| Continuity Agreement (under renegotiation) | Canada, Mexico | South Korea |

| Continuity Agreement | Chile, Peru, Vietnam

Singapore (the UK-Singapore Digital Economy Agreement replaced the e-commerce chapter) |

Costa Rica

Ecuador, Colombia |

| GSP / DCTS | Indonesia, Philippines | |

| No bilateral FTA | Malaysia, Brunei | China, Taiwan, Thailand, Uruguay |

| Note: The FTA with Peru, Ecuador and Colombia is the UK-Andean countries FTA. The FTA with Costa Rica is the UK-Central America FTA. Note 3: The Developing Countries Trading Scheme (DCTS) is expected to replace the Generalised Scheme of Preferences (GSP) | ||

The latest UK Government’s policy paper which was released at the time of signing the Protocol of Accession has argued that the CPTPP would provide substantial market opportunities for the UK, boosting UK GDP by around £2.0 billion each year.[5] This equates to approximately 0.09% of the UK’s GDP in 2021. This falls somewhat short of compensating for the predicted 4% GDP loss of leaving the EU.[6]

There are two broad reasons for this. First, the EU is the UK’s most important trade partner, accounting for almost a half of its goods trade and almost 40% of its services trade. This is because of its geographic proximity, which matters for trade. In comparison, CPTPP countries account for 8.1% and 8.3% of the UK’s exports of goods and services, respectively; and for 6.2% and 7.5% of the UK’s imports of goods and services, respectively (Table 2).

Table 2: Shares of UK trade with current and potential CPTPP members, 2021 (%)

| Current CPTPP | CPTPP Applicants | China | Sub-total | EU | ROW | |

| Goods Exports | 8.1 | 8.7 | 5.6 | 16.8 | 48.0 | 35.1 |

| Goods Imports | 6.2 | 16.2 | 13.4 | 22.3 | 46.5 | 31.2 |

| Services Exports | 8.3 | 5.3 | 3.0 | 13.6 | 35.8 | 50.6 |

| Services Imports | 7.5 | 3.5 | 1.2 | 10.9 | 39.7 | 49.3 |

| Source: ONS Pink Book 2022, Ch.9. Shares are calculated out of UK total (i.e., trade with the world), authors’ own.

Note: CPTPP Applicants includes formal applicants (China, Costa Rica, Ecuador, Taiwan, and Uruguay) and potential applicants (Colombia, Indonesia, Philippines, South Korea, and Thailand). We single out China to demonstrate its economic magnitude within the CPTPP applicants. |

|||||

Second, most UK trade with current CPTPP members is already carried out under preferential terms through Free Trade Agreements (FTAs), except for Malaysia and Brunei (Table 1). The UK’s trade with these existing CPTPP and FTA partners account for around 95% of all UK exports and imports with the CPTPP. Close to 80% of the UK’s total trade with the CPTPP is with Japan, Canada, Singapore, and Australia. Outside of these economies, Vietnam accounts for a relatively important share of goods imports, but all in all, the opportunities from other emerging markets in the bloc, such as Chile, Mexico, or Peru, look limited.

It is worth noting that the shares of UK trade with a fully expanded CPTPP would significantly increase, thus increasing the economic benefits for the UK, primarily driven by China’s potential accession. UK’s trade relations with China, Taiwan, Thailand and Uruguay are on World Trade Organization (WTO) terms and its trade relations with Indonesia and the Philippines are under the Developing Countries Trading Scheme (which only applies to imports) (Table 1). Their preferential market access offers under the CPTPP, and compliance with unified CPTPP rules, would improve the UK’s market access to these countries.

As for those countries with whom the UK already has a bilateral FTA, including South Korea, Costa Rica, Colombia and Ecuador, the added benefit of the CPTPP differs depending on the quality of the bilateral agreement. For South Korea, the UK-Korea FTA is a continuity agreement based on the EU-Korea FTA (signed in 2009) and is currently under re-negotiation with updates expected in some areas. It is unlikely that Korea would offer more to the CPTPP than it has to the UK, the EU or the US. In contrast, if Costa Rica, Ecuador and Colombia join the CPTPP, this may create a better preferential trade environment for the UK since current trade agreements with these countries are narrower and shallower than the CPTPP.

There are two things to note regarding changes in market access for trade in goods. First, in aggregate, tariff elimination under the CPTPP does not provide significant new opportunities for the UK. This is because, as explained previously, most of the UK’s trade in goods with the CPTPP countries is (and/or soon will be) carried out under FTA preferences. Table 3 shows that, in 2021, the UK’s most important exports to the CPTPP were in machinery and mechanical appliances, precious metals, and motor vehicles. Products in these categories accounted for 45% of all UK exports to the CPTPP, and 7%-9% of all UK exports of these products were destined to CPTPP countries[7]. On average, these products faced almost zero, or very low, tariffs.

The market access of UK goods to Malaysia and Brunei will be upgraded from Most Favoured Nation (MFN) terms to preferential tariffs. For instance, Malaysia applies high MFN tariff rates on UK exports of vehicles (also including parts and accessories), whiskies and other spirits with high alcoholic percentages, while frozen and fresh meat currently face tariffs in excess of 30%. These are all products which the UK exports competitively, but not to Malaysia. In the case of Brunei, the highest tariffs currently applied on UK exports were 10% for various forms of textiles, and 5% for various forms of furniture.

China’s potential accession to CPTPP could provide substantial benefits for UK exporters as current tariff arrangements with China are also on an MFN basis. This is especially the case for motor vehicles and machinery, which make up a considerable amount of the UK’s exports to China (Table 3). Exports of these products to China face, on average, much higher tariffs compared to other potential CPTPP members, which mostly trade under preferential terms with the UK (Table 1).

Lastly, it is important to bear in mind that under CPTPP agreement there are numerous country-product-specific tariff-rate quotas (TRQs) that are mostly applicable to agri-food products. For example: Canada has TRQs in place for many dairy products, Malaysia on live poultry, pork, and eggs, Japan on wheat products, barley and chocolate. Once fully implemented, however, 99% of tariff lines among CPTPP members are expected to be duty-free.[8] This follows the UK’s current tariff elimination commitments under bilateral FTAs with current CPTPP members.

Table 3: The UK’s top goods exports to current and potential CPTPP members, 2021

| (1) | (2) | (3) | (4) | ||

| Partner | HS Code | Value

(£mn) |

Share, Partner Total (%) | Share, Product Total (%) | Average Tariff (weighted) |

| CPTPP | 84: Machinery and mechanical appliances; parts thereof. | 4,358 | 19.2 | 9.3 | 0.63 |

| 71: Precious or semi-precious stones, precious metals. | 4,160 | 18.3 | 8.7 | 0.05 | |

| 87: Vehicles; other than railway or tramway rolling stock; parts thereof | 1,706 | 7.5 | 7.6 | 3.82* | |

| China | 27: Mineral fuels, mineral oils and products of their distillation | 1,992 | 15.7 | 7.3 | 0.11 |

| 87: Vehicles; other than railway or tramway rolling stock; parts thereof | 1,612 | 12.7 | 7.2 | 14.66 | |

| 84: Machinery and mechanical appliances; parts thereof | 1,585 | 12.5 | 3.4 | 4.02 | |

| Other Potential Members | 27: Mineral fuels, mineral oils and products of their distillation | 1,515 | 16.4 | 4.0 | 0.01 |

| 84: Machinery and mechanical appliances; parts thereof | 840 | 12.5 | 1.8 | 1.52 | |

| 71: Precious or semi-precious stones, precious metals. | 671 | 10 | 1.4 | 0.10 | |

| Source: UN Comtrade and UNCTAD-TRAINS via WITS. Table prepared using TradeSift software.

Note: the shares under (2) are calculated out of the total trade with the partner; shares under (3) are calculated out of the total trade in that product; tariffs under (4) correspond to a trade-weighted effectively applied average rate of ad-valorem equivalents. ‘Other Potential Members’ includes Costa Rica, Ecuador, Taiwan, Uruguay (as formal applicants) and Colombia, Indonesia, Philippines, South Korea and Thailand (as potential applicants).*We expect this to change to almost zero once FTAs with Australia and New Zealand enter into force. |

|||||

The use of preferential tariffs heavily depends on rules of origin since UK firms must comply with product-specific rules of origin (ROOs) in order to gain preferential access to the markets of existing and potential members. ROOs under the CPTPP are different to those specified in each of the UK’s bilateral agreements. This may make it more difficult for UK firms to benefit as much from using ROOs under the CPTPP, depending on the different degrees of ROO restrictiveness across agreements.

There are two potential benefits regarding ROOs. Firstly, these rules affect all CPTPP countries. This could facilitate trade for UK firms in those markets, in terms of reducing cost and bureaucracy. Hence, UK firms will be able to trade under standardised rules of origin with a large group of trading partners, including current CPTPP members with whom the UK has a bilateral agreement (Australia, New Zealand and Japan) and potential future members.

Secondly, and more importantly, CPTPP “cumulation rules” allow the use of inputs from other members, counting them as “originating”, which widens the input supply for UK firms. This is particularly relevant for those products subject to rules that require a minimum amount of originating content in the product’s value added. Thus, for instance, a UK firm aiming to export machinery or electrical equipment to Australia under CPTPP rules, could use inputs from Japan, New Zealand and other CPTPP members, which will be considered as “originating”. The same would apply for potential new CPTPP partners.[9]

In practice, identifying whether it would be beneficial to apply CPTPP rules of origin in existing bilateral agreements is challenging because it depends on the product exported and the target destination. Each product is subject to one or more specific types of rules per agreement, with different degrees of restrictiveness, i.e. difficulty of compliance. For that reason, it is necessary to compare the CPTPP with existing bilateral agreements and look at the restrictiveness of the underlying rules of origin.

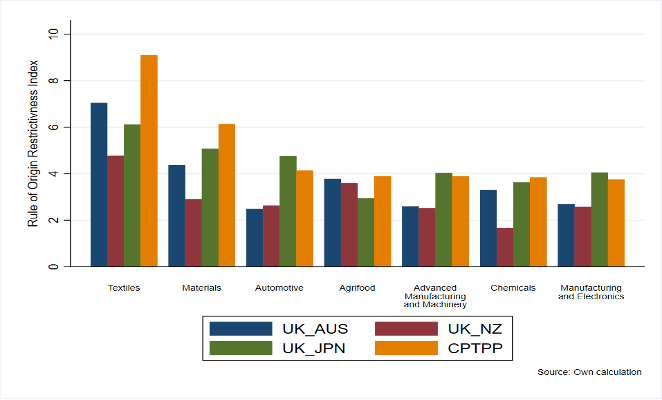

We apply a Rules of Origin Restrictiveness Index (ROO-RI),[10] scoring every product (defined at the HS 6-digit level) in Annexes 3-D and 4-A of the CPTPP with ranges on a scale from 1 to 10 (the higher the score, the more restrictive the rule). We find that the CPTPP has an average degree of restrictiveness of 5.25. That number implies a moderate restrictiveness level of the rules of origin contained in the CPTPP, given the 1-10 scale of our index. In contrast we find that ROOs under the CPTPP are on average more restrictive. The UK-Japan deal has a 4.35 average score, followed by UK-Australia with 4.10 and UK-New Zealand with 3.01.

Figure 1 shows the average ROO-RI for the CPTPP and the three aforementioned agreements across a set of broad industries. The CPTPP appears more restrictive in terms of rules of origin in the textile industry and, to a lesser extent, in materials, agrifood and chemicals.

Figure 1: ROO Restrictiveness Index across Industries – CPTPP vs. Other UK Trade Agreements

Looking at products which the UK intensively trades with current and potential CPTPP members, such as the machinery and transport industries, we see that the benefit of using the CPTPP ROOs as opposed to existing bilateral agreements is very product specific.

The Department for Business and Trade mentions car engines as an example of potential benefits for UK firms, by trading with CPTPP members under “modern rules of origin”. Our ROO restrictiveness analysis finds that engines for vehicles (from Chapter 84 of HS product classification) have a ROO-RI of 3.5 under the CPTPP, higher than UK-New Zealand and UK-Australia (scored 3 in both agreements), but lower than UK-Japan (scored 5). Goods in the transport industry are mostly subject to the Change in the Heading rule (CTH) in the CPTPP, which tends to be harder to comply with, as it typically involves a more complicated input transformation process than the Change in the Subheading rule (CTSH), which is more present in the UK-Australia and UK-New Zealand deals. As for the UK-Japan deal, the presence of exceptions to the CTH rule, which restrict the use of some inputs, complicate the compliance, driving up the restrictiveness score in that industry.[11]

A similar picture can be seen for different types of vehicles, in which CPTPP has an average score of 5.5, exactly like in UK-Japan, but higher than UK-New Zealand (scored 3 in each). In other words, trading with Australia and New Zealand under the CPTPP would imply complying with more restrictive rules of origin for UK firms than under existing bilateral agreements. That setback could be partly offset by the ability to make use of inputs from other CPTPP countries, seen as “originating”. On the other hand, firms targeting those markets that would also like to trade under easier ROO from the bilateral agreements, may not be able to use those CPTPP “originating” inputs. Hence, we need further product-specific analysis to be able to conclude which products it is better to trade under which deal.

CPTPP countries have strongly integrated value chains between themselves, and this is expected to increase. This is not surprising given the geographical proximity of CPTPP countries and their sectoral specialization. For the UK, the question then is what are the possibilities of integrating into these value chains, and for CPTPP countries to integrate into UK value chains? According to the UK Department for Business and Trade, CPTPP Rules of Origins will allow the UK to deepen its integration with CPTPP countries and hence diversify its supply chain linkages. To see the UK’s potential opportunities, we look at the supply chain relations between the UK with both current and potential CPTPP members.

Consider first, the extent to which CPTPP countries use UK value added in CPTPP exports (current and applicant members, including China).[12] We find that the UK accounts for only 0.4% of the value-added embedded in total CPTPP exports (current and applicant members, including China), while the EU accounts for 2.8% and the US for 4.1%. This indicates that size and proximity play an important role in determining participation in the value chain. Even if we control for the economic size of the EU, we find that UK involvement in CPTPP value chains is lower than that of the EU.

Next, we consider the converse: the value-added originating in CPTPP countries which is used in UK exports. We distinguish between current members and potential applicants (Colombia, Costa Rica, Taiwan, South Kora, Thailand, the Philippines and Indonesia).[13] We separate China from the group of applicants for comparison. Also, for comparison purposes, we include the share of value added sourced domestically from the EU27 and from the US. The calculation is done for three broad sectors: agriculture, forestry and fishing; manufacturing; services; and total (Table 4).

There are three key messages.

Table 4: Source of Value-Added in UK Exports 2018 (shares)

| Origin | Agriculture,

forestry & fishing |

Industry | Services | Total |

| CPTPP current | 1.34 | 2.05 | 1.06 | 1.42 |

| CPTPP applicants | 0.61 | 0.72 | 0.39 | 0.51 |

| China | 0.93 | 1.58 | 0.53 | 0.91 |

| China + CPTPP total | 2.89 | 4.35 | 1.98 | 2.85 |

| EU27 | 10.23 | 11.39 | 5.22 | 7.49 |

| USA | 3.47 | 3.69 | 2.11 | 2.69 |

| GBR | 78.02 | 72.15 | 87.96 | 82.17 |

Source: authors’ calculation based on OECD TiVA data.

Note: “CPTPP current” means the current 11 CPTPP member countries. “CPTPP applicants” include Colombia, Costa Rica, Taiwan, South Kora, Thailand, the Philippines, Indonesia. Uruguay and Ecuador are not covered in the TiVA dataset. “CPTPP total” means “CPTPP current” and “CPTPP applicants”.

In general, preferential services trade commitments under FTAs often do not provide a higher level of market access than that which the countries are in practice already allowing. Instead, preferential commitments in FTAs tend to lock-in the existing de facto liberalization provided by the unilateral and this helps to provide more certainty to businesses. Among current and potential CPTPP members, Southeast Asian countries, such as Indonesia, Thailand, Vietnam, Malaysia, show a high degree of restrictiveness in measures around services trade (Figure 2).

Figure 2: Services trade restrictiveness of applied measures – Current and potential CPTPP members

Source: OECD Services Trade Restrictiveness Index (STRI): Services Trade Restrictiveness Index (oecd.org)[14]

The major services exports from the UK to CPTPP countries are: ‘Other Business Services’ such as professional services, accounting, legal, engineering, and architectural services (27.7%), Financial services (23.9%), and Insurance and Pension services (13.3%) as can be seen in Table 5. The majority of UK services exports go to its four major CPTPP trade partners (Japan, Canada, Singapore and Australia). For example, 96% of UK Financial Services exports go to these countries. Since emerging markets such as Chile, Peru and Vietnam, already have a bilateral FTA with the UK, it is not known how much their services commitments under CPTPP would boost UK exports. Nevertheless, some commitments in the area of temporary entry for business persons that these countries made under the CPTPP are likely to facilitate business mobility.[15] The CPTPP can provide a clear advantage regarding the market access to Malaysia, since its services trade market access commitments under the CPTPP are much better than its WTO commitments.

Regarding potential CPTPP members, if China makes greater services commitments compared to its WTO commitments, these could improve UK’s market access. The area the UK currently predominantly exports to China are in travel services (42%), as well as Other Business Services (14.4%), transportation services (13.6%) and Financial Services (11.6%). Regulations which widely affect UK’s services exports, such as digital trade related measures (e.g. the local requirement on storing personal information) and labour market tests, will also be important.

Table 5: UK exports of services to current and potential CPTPP members, 2021 (%)

| (1) | (2) | (3) | |||

| Partner | EBOPS Code | Value

(£mn) |

Share, Partner Total (%) | Share, Service Total (%) | |

| CPTPP | 10: Other Business Services | 7,132 | 27.7 | 5.8 | |

| 7: Financial Services | 6,138 | 23.9 | 9.1 | ||

| 6: Insurance and Pension Services | 3,419 | 13.3 | 19.4 | ||

| China | 4: Travel | 4,007 | 42.0 | 16.6 | |

| 10: Other Business Services | 1,371 | 14.4 | 1.1 | ||

| 3: Transportation | 1,299 | 13.6 | 6.9 | ||

| Other Potential Members | 7: Financial Services | 1,838 | 26.1 | 2.7 | |

| 10: Other Business Services | 1,433 | 20.3 | 1.2 | ||

| 9: Telecomms and ICT Services | 1,373 | 19.5 | 4.6 | ||

| Source: ONS Pink Book 2022, Ch.9. Note: the shares in (2) are calculated out of total trade with the partner; shares in (3) are calculated out of total trade in that product. Data by service type is not available for Brunei, Peru, Vietnam, Costa Rica, and Ecuador. Total values may contain suppressed data. ‘Other Potential Members’ includes Costa Rica, Ecuador, Taiwan, Uruguay (formal applicants), and Colombia, Indonesia, Philippines, South Korea, Thailand (potential applicants). | |||||

In terms of rules (provisions), the Cross-Border Trade in Services chapter, the standalone financial services chapter and electronic commerce chapter improve transparency in relation with trade partners without a deep bilateral FTA with the UK. The CPTPP’s services and e-commerce chapters could provide a high degree of policy certainty with potential future members, and liberalization regarding others (eg. Costa Rica,, Ecuador or Columbia). Given that the UK is currently negotiating updates to the UK-South Korea FTA, it is unlikely that the CPTPP would provide more market access.

Given the competitiveness of the UK in services, we also explore the extent to which other countries make use of UK services in their exports – we call this embodied services exports. In Table 6 we give the share of UK embodied services exports by destination (and by broad sectors). If we look at the last column of the table, it indicates that out of all UK services exports that are then used by other countries in their exports (embodied service exports) 9.99% of these went to the CPTPP countries (and 4.05% to the CPTPP applicants, 2.7% to China and 83.27% to the Rest of the World). This is slightly higher than the share of UK direct services exports going to the CPTPP (see Table 2), which is 8.3%. The embodied services shares in exports going to the CPTPP are fairly similar across the three sectors, whereas we see a higher share for ‘Industry’ with regard to the CPTPP applicants and China. It is worth also noting that the table focusses on services embodied in other countries’ exports and thus by definition excludes the services embodied in the UK’s own exports. If we were to include this, then the share of domestic exports dominates, while accounting for 78% of UK total embodied services exports.

Table 6: UK embodied services exports by partner, % of total

| Exporter | Agriculture | Industry | Services | Total |

| CPTPP current | 8.04 | 10.17 | 9.82 | 9.99 |

| CPTPP applicants | 1.51 | 5.77 | 2.15 | 4.05 |

| China | 0.83 | 4.48 | 0.69 | 2.70 |

| ROW | 89.61 | 79.58 | 87.34 | 83.27 |

| Total | 100 | 100 | 100 | 100 |

Source: authors’ calculation based on OECD TiVA data for 2018.

Note: CPTPP applicants include Colombia, Costa Rica, Taiwan, South Kora, Thailand, the Philippines, and Indonesia. Uruguay and Ecuador are not covered in the TiVA dataset.

This table suggests that CPTPP countries are not a large market for UK embodied services exports, and neither does it indicate that the UK has a particularly strong, services focussed, supply chain relationship with current CPTPP members.

The previous section suggests that the economic benefits to the UK based on current trade relations are limited. An additional factor here is that some of the FTAs the UK has with the existing CPTPP members go further in certain policy areas. For example, the UK-Australia FTA and the UK-New Zealand FTA used the CPTPP as a template but further developed some rules such as on digital trade, financial services, and on the mobility of people. Similarly, the UK-Japan Comprehensive Economic Partnership Agreement (CEPA), has a digital trade chapter that goes further than the CPTPP and the Japan-US digital trade agreement. With Singapore, the UK successfully concluded a high-standard bilateral digital economy agreement using the CPTPP, the UK-Australia FTA, Australia-Singapore digital economic agreement, and Digital Economic Partnership Agreement as a template. The UK is also currently renegotiating its bilateral FTA with Canada and with Mexico to upgrade the existing continuity agreements.

With regard to Chile and Peru, the CPTPP may provide added benefits for the UK as the UK’s FTAs with these two countries are not as deep as the CPTPP agreement. The largest bilateral policy gain that the CPTPP creates is regarding UK trade with Malaysia and Brunei, which is currently on WTO terms with the UK. Notably Malaysia, which is transforming its economy from a middle-income to a high-income country, still maintains relatively strict services and investment policy.[16] Therefore, the CPTPP rules would provide legal certainty to UK business.

Although the economic opportunities for the UK to some extent depend on CPTPP’s future expansion, significant expansion is unlikely in the foreseeable future. The accession of China is the most challenging. First, for current members, China’s accession requires a hard geostrategic political decision, given history and political strategy behind the CPTPP. Trans-Pacific Partnership (TPP) negotiations were launched by the Obama administration in 2010. The rhetoric was to position the US as a rule-setter of the Asia-Pacific, including China.[17] Led by the US, TPP members aimed to achieve free, transparent and level-playing-field trade rules, and this also underpins the CPTPP. Currently, CPTPP members are driving through a volatile geopolitical landscape concerning China, including intensifying China-US hegemonic rivalry, China’s expansionism in the South China Sea and the China-Taiwan conflict. Many CPTPP members are close security allies of the US (e.g. Australia, Japan) and like-minded countries (Canada, Mexico, Malaysia, Singapore, Vietnam and New Zealand) in the Indo-Pacific region.[18]

In addition, the Biden administration’s initiative of the Indo-Pacific Economic Framework (IPEF) involves seven of the CPTPP countries (Australia, Brunei, Japan, Malaysia, New Zealand, Singapore and Vietnam).[19] IPEF is part of the US’s strategy to counter China’s strong economic and political influence in the region. Regardless of whether it creates tangible impacts,[20] the US’s re-engagement in the Indo-Pacific region may indirectly impact any decisions by CPTPP members regarding China’s membership. Given the economic significance of China, some Asian-Pacific countries are considerably counterbalancing politics and economics. In this context, the Regional Comprehensive Economic Partnership (RCEP), which is more flexible and involves shallower trade deals compared to the CPTPP, may play an important role in maintaining a close trade relation with China in the Asia-Pacific region. Seven CPTPP countries (Australia, Brunei, Japan, Malaysia, New Zealand, Singapore and Vietnam) are members of both the IPEF and the RCEP. These countries may not feel a strong economic or political impetus to welcome China into the CPTPP as the current policy framework could maintain a certain degree of political and economic equilibrium.

Second, for China, the conditions for joining the CTPP may prove too much. CPTPP members will apply strict requirements to protect the CPTPP’s fundamental principles of market-oriented rules and free trade. The accession rules demand each aspirant to accept “all of existing CPTPP rules”.[21] Since TPP negotiations were led by the US, the CPTPP rules strongly reflect the interests of American businesses and show an inclination towards containing China. This will be problematic for China. Although some argue that the Chinese government is domestically preparing for accession and intends to use it for political leverage when introducing domestic reforms,[22] it will take many years for China to fill the gap between its policies and CPTPP rules. The most challenging areas are digital trade, state-owned enterprises (SOEs), labour rights, government procurement, and intellectual property right protections and enforcement. For example, CPTPP digital trade rules are significantly different to those in China. Hence, China’s data sovereignty policy, including data localisation requirement as a prerequisite to do any sort of business, does not comply with the CPTPP’s prohibition on data localisation requirement. Another example concerns the rules on State Owned Enterprises (SOEs). The CPTPP SOE rules were designed to promote a level playing field. There is an intention to discipline China’s state-dominated economy (23-28% in China’s GDP[23]) and lack of transparency around its SOEs with strong penalties if China seeks a membership.[24]

Furthermore, to maximise an opportunity, CPTPP members will demand high-level market access commitments from China, especially in the areas of services and investment, where a high degree of protection remains. Whether China would be ready to agree to such commitments remains doubtful.

From the institutional perspective, it would appear that China’s chance of joining “the Club” seems very limited. For instance, China’s accession process could be on hold for several years as CPTPP members struggle to reach a decision as to when to begin the accession process. According to the CPTPP rules around its Accession Process, “the aspirant economy is encouraged to have consultations with each Party, with a view to addressing each Party’s questions or concerns on interested areas” for the accession process to start. Even if the Accession Working Group is formed and negotiations begin, it will take years for China to satisfy every requirement posed by the members of the CPTPP at each stage of the accession process.

If China’s accession process is politically delayed, or the process takes too many years to reach a conclusion, what would happen to the other countries waiting in line? In theory, CPTPP members could start accession negotiations for other aspirants, skipping over China or in parallel with its accession process, since there is no rule which explicitly prohibits this. However, bypassing China and starting the accession of Taiwan, which is the second country in line, may serve to deteriorate the relationship with China. Indeed, plausibly, China’s application may have the intention of complicating Taiwan’s bid.[25] The political economy surrounding China’s application would inevitably impact the other applications.

The economic benefits for the UK from joining the CPTPP largely depend on the CPTPP’s future expansion, with the accession of China providing substantial benefits to the UK. This is because the UK lacks preferential trade arrangements and a strong supply chain relationship with China. However, political and institutional factors surrounding China’s accession indicate that it is unlikely that China will join the CPTPP in the foreseeable future. This may have knock on effects to other accessions, especially Taiwan. China’s application to the CPTPP has made the club more difficult to expand.

China’s application creates a dilemma for the UK, as indeed for other CPTPP members. While the UK would economically benefit from China’s joining the CPTPP, it is difficult for the UK to accept China becoming a CPTPP member for political reasons. Given that the UK’s closed allies, such as Australia, Canada and Japan, wish to protect a liberal and open trade order based on the democratic system and expect the UK to become a ‘gatekeeper’ of the CPTPP[26] to protect this value together, it is important for the UK to seek alignment with these CPTPP members. Also, the UK should not erode the US’ initiative of promoting IPEF to increase its economic diplomacy presence vis a vis China in the Indo-Pacific.

The CPTPP is a like-minded middle power club that supports the liberal and rules-based trading system. Since the CPTPP was signed in 2018, the trade policy environment surrounding the CPTPP has been somehow changing from a neoliberal order to a post-neoliberal order. For example, countries are enhancing economic security policy by justifying the needs for resilient supply chains and protection from economic coercions. Big economies are entering into a subsidy race for green economy and trade. These could threaten a key aim of the CPTPP, which is to maintain a liberal and rules-based system, but somehow governments seem to be turning a blind eye to the contradictions between liberal FTAs, such as the CPTPP, and the move to more interventionist trade and industrial policies.

For the UK, what lies ahead after signing the treaty? The UK government should renew its strategic plan. The UK’s stated main strategy in joining the CPTPP was to economically benefit, especially from future expansion. But this strategy is challenged by the rapidly changing global and geopolitical landscapes and the difficulties of climate change and economic security. The UK Government should develop and articulate a strategic plan based on the political reality surrounding the CPTPP that focuses on coordinating with ‘like-minded’ countries, such as Australia, Canada and Japan, while maintaining an open and rules-based trading system on the one hand and addressing challenges related to economic security, climate change and sustainable development on the other.

[1] CPTPP trade deal will benefit UK if we use it, says Kemi Badenoch – BBC News

[2] Data retrieved from World Bank (02 February 2023). Indicators: GDP, PPP (constant international $), Population, total; Exports of goods and services (BoP, current US$); Imports of goods and services (BoP, current US$). Shares calculated out of world total. The future expansion of the CPTPP could increase these shares significantly, but this is mostly dependant on China’s accession.

[3] Department for International Trade (2021). UK accession to CPTPP: The UK’s strategic approach; UK Accession to CPTPP: The UK’s Strategic Approach (publishing.service.gov.uk). And the section of “Wider considerations” in Department for Business & Trade and Department for International Trade (2023). Policy Paper: Conclusion of Negotiations on the Accession of the United Kingdom of Great Britain and Northern Ireland to the Comprehensive and Progressive Trans-Pacific Partnership

[4] China submitted the application exactly one day before Taiwan.

[5] Department for Business & Trade (2023). Impact assessment of the accession of the United Kingdom of Great Britain and Northern Ireland to Comprehensive and Progressive Agreement for Trans-Pacific Partnership, 17th July, 2023.

[6] Office for Budget Responsibility, Economic and Fiscal Outlook, October 2021.

[7] Products classified as pharmaceutical products (HS 30), electrical machinery and equipment (HS 85) and beverages and spirits (HS 22) accounted for an additional £5.6 bn (equal to 18%) of UK exports to CPTPP countries. Moreover, 15.2% of the UK’s exports of beverages and spirits were destined to CPTPP countries.

[8] See “The Agreement” in Conclusion of Negotiations on the Accession of the UK to the CPTPP (31 March 2023).

[9] These advantages were also highlighted by the UK government, concluding that UK firms have thus the opportunity to diversify supply chains. The UK government also points out that the UK already has bilateral agreements with some CPTPP members, and that UK firms could use the preferential regime they prefer. See: DBT and DIT (2023).

[10] The ROO-RI was originally developed by Ayele, Gasiorek and Tong (2022), varying across products. This index extends a previous index by Cadot et al. (2006) and ranges on a scale from 1 to 10. The higher the score, the more restrictive the rule.

[11] Under the Change in Tariff Classification (CTC) rule, an imported input must be from a different tariff classification from that of the good to be exported, so it can be granted originating status. That usually involves a more complicated transformation process the higher the rule level. Therefore, we assume that a Change in Chapter (CC) is harder to comply with than a Change in Heading (CTH), which is in turn more restrictive than a Change in Subheading (CTSH).

[12] All calculations derived from the OECD TIVA dataset. Trade in Value Added – OECD

[13] The TiVA dataset does not cover Ecuador, which is a CPTPP applicant.

[14] Scoring of STRI relies on a careful reading of regulations and policies by economists and lawyers. Each of many elements is scored as restrictive (1) or not (0) and the overall score derived as a weighted sum of the parts scaled to range from 0 (no restrictions) to 100 (total restriction). The coverage of restrictiveness in the STRI stretches beyond the GATS market access and national treatment measures.

[15] The UK government’s latest policy paper lists some commitments and a new high benchmark on business mobility commitment with Mexico, Chile and Malaysia .

[16] WTO Trade Policy Revie, Malaysia, Report by the secretariat (WT/TPR/S/436), 14th December 2022.

[17] Wall Street Journal, April 2015, (Obama Presses Case for Asia Trade Deal, Warns Failure Would Benefit China – WSJ).

[18] U.S. Seeks to Build Network of Like-Minded Nations in Indo-Pacific > U.S. Department of Defense > Defense Department News and FACT SHEET: Indo-Pacific Strategy of the United States | The White House

[19] Canada is seeking a membership to the IPEF. Potential CPTPP members, including Indonesia, Korea and Thailand are members of the IPEF.

[20] Will IPEF Help the US Counter China? – The Diplomat

[21] Annex to CPTPP/COM/2019/D002: Accession-Process.pdf (mfat.govt.nz)

[22] See Deborah Elms Testimony (uscc.gov), for example.

[23] World Bank Working Paper, https://documents1.worldbank.org/curated/en/449701565248091726/pdf/How-Much-Do-State-Owned-Enterprises-Contribute-to-China-s-GDP-and-Employment.pdf

[24] Bhala, R. (2017). TPP, American National Security and Chinese SOEs. World Trade Review, 16(4), 655–671. And Chow, D. C. K. (2017). How the United States uses the Trans-Pacific Partnership to contain China in international trade. Chicago Journal of International Law, 17(2), 370–.

[25] The CPTPP Bids of China and Taiwan: Issues and Implications (asiapacific.ca)

[26] Britain’s post-Brexit trade alliance is a triumph … for Japan – POLITICO