Download Briefing Paper 24

Understanding what services trade liberalisation under FTAs can offer

Why are FTA services negotiations so difficult?

Legal and economic factors affecting FTA services negotiations

The UK’s future FTA services negotiations with non-EU countries

It is unrealistic for the UK to expect better deals than those of the EU

Britain relies hugely on the services sector, accounting for 80 per cent of the economy. In terms of trade, 45 per cent of its exports are cross-border services. Despite the fact that more than one-third of its services exports go to the EU, the UK government has decided to leave the EU single market for services. The UK government has high expectations of future services trade deals with non-EU countries but seems to have a very rose-tinted view of what FTAs can really offer.[1]

This briefing paper considers the UK’s future services trade deals with non-EU countries. We explain what Free Trade Agreements (FTAs) can really offer and why actual liberalisation is so difficult to achieve in FTA services negotiations. We then examine the factors that would specifically affect the UK’s future FTA services negotiations and thus develop a realistic view of how much the UK can expect from services trade deals with non-EU countries. We conclude that they offer no chance of recouping the losses of services trade resulting from leaving the services components of the EU Single Market.

Unlike goods trade negotiations – which conventionally focus on tariff eliminations/reductions – services trade negotiations are all about regulations. The Uruguay Round (1986-1994) incorporated services into trade liberalisation. The General Agreement of Trade in Services (GATS) helped to give greater clarity to businesses by providing obligations and disciplines on services trade and codifying WTO Members’ liberalisation commitments in terms of market access and national treatment.[2]

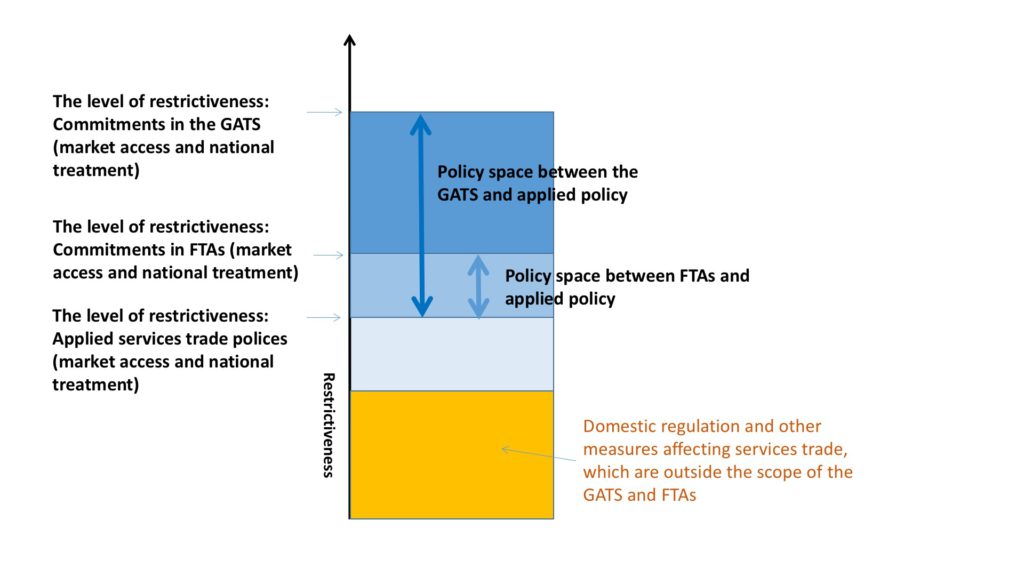

However, in the main, services trade agreements do not lead to actual trade liberalisation, which requires changes to existing services trade regimes. Figure 1 conceptualises two layers of ‘policy space’ in terms of market access and national treatment for services trade: one is between commitments in the GATS and applied services trade policy and the other between commitments in FTAs and applied services trade policy. In reality, commitments in neither the GATS nor FTAs are as liberal as applied trade policies in terms of market access and national treatment. In other words, countries have legally committed only a limited part of their actual services trade liberalisation. This is because governments prefer to retain the flexibility to change policies by maintaining ‘policy space’ between international trade agreements (i.e. the GATS and FTAs) and their applied policies. For example, a country may allow a 100% foreign equity share in its applied policy in broadcasting while providing no commitments in the GATS and guaranteeing only a 50% share in an FTA. This enables it to introduce any type of foreign equity restriction with partners trading under the GATS and to restrict FTA partners’ shares to levels between 50% and 100%.

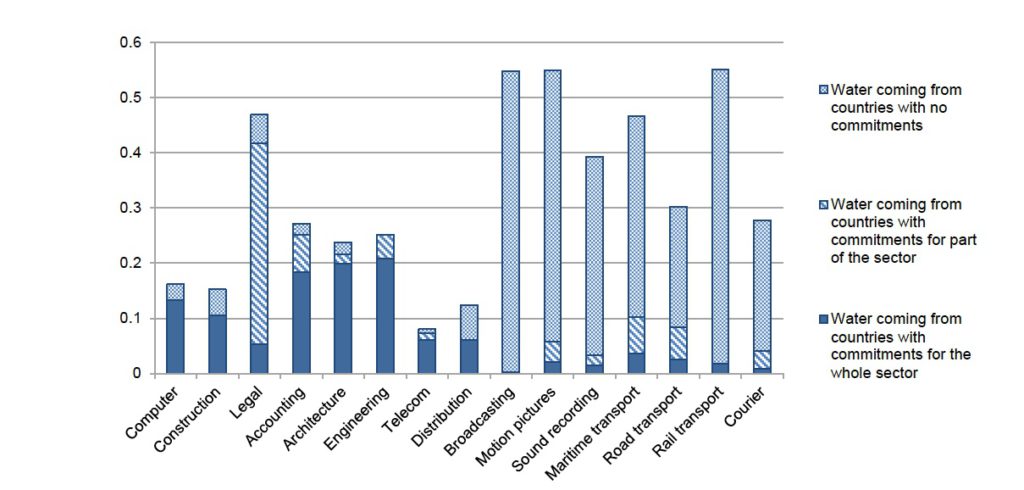

A study conducted by the OECD provides the numerical evidence that countries’ bound level of restrictiveness in the GATS is far above the level of restrictiveness of applied services trade policy.[3] Figure 2 shows the average ‘water’ (policy space) between the GATS commitments and applied services trade policy for 40 countries by sector.[4], [5] ‘Water coming from countries with no commitments’ in Figure 2 means that some liberalisation can be seen in applied policy even though no commitments have been made in the GATS. ‘Water coming from countries with commitments for part of the sector’ means that there is more liberalisation in applied policy than in the level of partial commitments in the GATS. ‘Water coming from countries with commitments for the whole sector’ means that the applied level is more liberal than the corresponding full commitment in the GATS.

Two features are evident from Figure 2. First, countries retain a huge policy space between the GATS commitments and applied services trade policy. Second, policy space in broadcasting; motion pictures; sound recording; maritime transport; road transport; rail transport and courier services comes mostly from countries with no GATS commitments in those sectors. In general, the higher the level of restriction, the deeper the ‘water’ in the GATS. In addition, although the study does not cover many developing countries, it shows that applied services trade policy in developing countries is generally more restrictive than that of developed countries and that developing countries typically have deeper ‘water’ than developed countries.[6]

Note: The average is based on the 40 countries covered in the STRI. But as landlocked countries are excluded from maritime transport and Iceland has no rail freight, the total number of countries is respectively 34 and 39 for maritime transport and rail transport. Source: Figure 3 in Miroudot, S. and Pertel, K. (2015), p12.

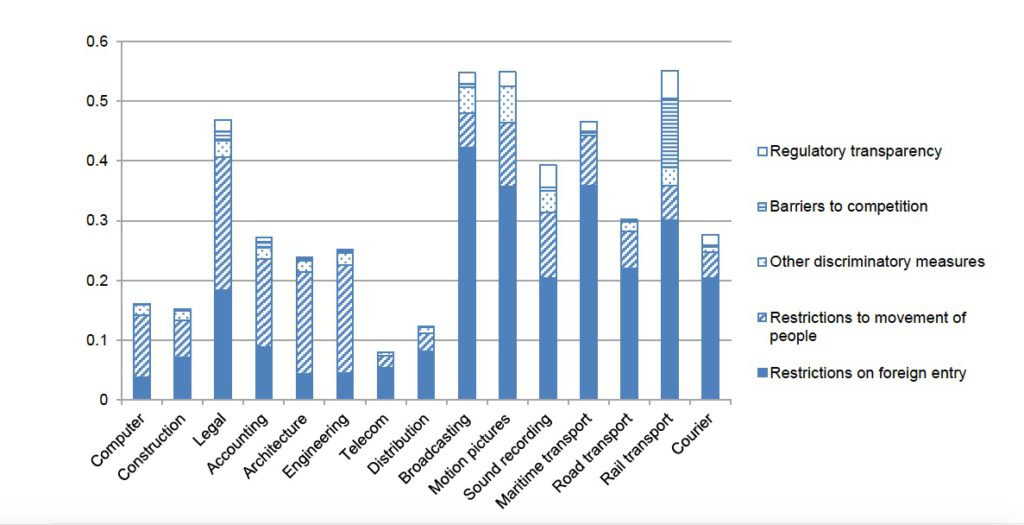

The OECD study also identified types of measures which comprise the ‘water’ in services bindings (Figure 3). For sectors that show the highest levels of policy space, restrictions on foreign entry tend to contribute the most ‘water’. In professional services such as legal; accounting; architecture; engineering and computer services, the major restriction is on the movement of people. Finally, it is worth noting that a World Bank study found that the offers made in the multilateral negotiations in the WTO’s Doha Round made virtually no progress towards eliminating the policy space between bound and applied policies in services.[7]

Source: Figure 13 in Miroudot, S. and Pertel, K. (2015), p25.

Note: (i) Regulatory transparency includes transparency relating to timeframe, number of official procedures required, and total cost of procedure; (ii) Barriers to competition include statutory monopoly and regulation which distorts competition; (iii) Restrictions on foreign entry: maximum foreign equity share; and (iv) Restrictions to movement of people include regulation relating to intra-corporate transferee, contractual services suppliers, and independent services suppliers. See more detail about methodology.

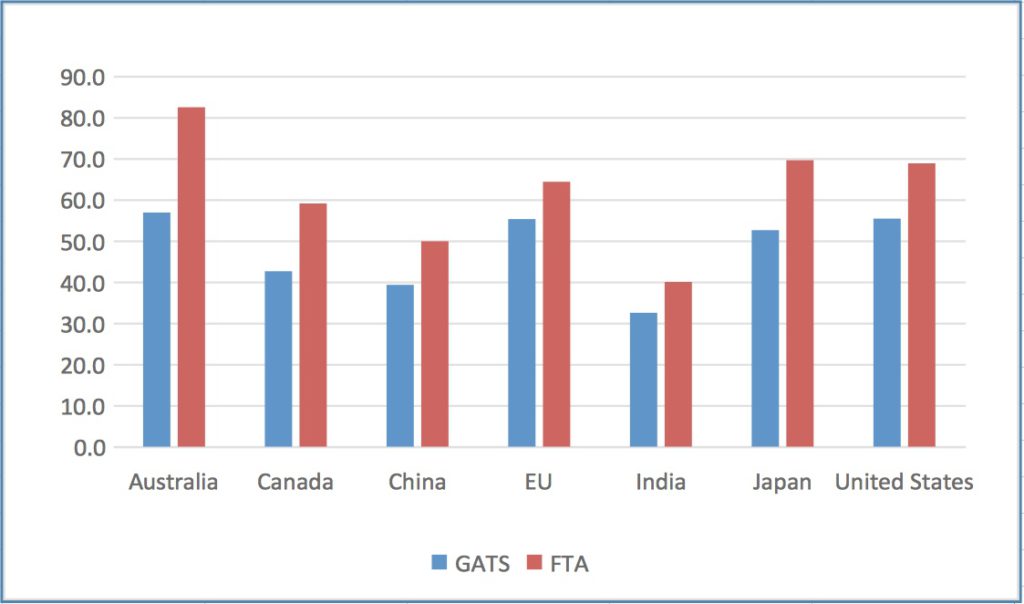

Figure 2 shows that countries’ applied policies are far more liberal than their GATS bindings. A similar exercise on the FTAs of WTO Members suggests that, on average, countries have committed more liberalisation in FTAs than in the GATS.[9] Figure 4 compares the openness in GATS commitments and the openness in FTA commitments for selected WTO members. Here, the scale shows the level of liberalisation. All the countries made “GATS+” commitments in their FTAs (i.e. more or deeper commitments than in the GATS), although the margin of liberalisation between the GATS and FTA commitments varies. However, this exercise excludes recently concluded FTAs, such as the Canada-EU, EU-Japan, and the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), which were signed after it was carried out. These agreements aim to go further in services than earlier ones did, but, as Magntorn and Winters (2018) show for EU-Canada (CETA), they still leave much to be done.

Source: WTO, Dataset of services commitments in regional trade agreements (RTAs)[10]

Note: The index score is brought within a scale of 0 to 100 for each sector (Mode 1 and Mode3), with 100 representing full commitments (i.e., without limitations) across all relevant sub-sectors. “GATS” reflects the index value for both GATS commitments and services offer in the Doha Development Agenda. “FTA” reflects the index value for a WTO Member’s ‘best’ FTA commitments prior to 2010. The score for EU commitments is for the EC-15.

It is important to recall that there are also other types of domestic regulation outside the scope of the GATS and FTAs, which are still de facto restrictive of foreign services suppliers. According to the OECD STRI, ‘other trade barriers’ provide 40% of restrictiveness on average.[12] Examples of these measures include requirements that: foreign suppliers are treated less favourably with regard to taxes and eligibility for subsidies; only locally-licensed professionals (e.g. lawyer, accountant, auditor, architect and engineer) may use the professional title; foreign programme producers have to recruit part of the cast and crew among local professionals; and discriminatory censorship fees and procedures. Whilst these are traditionally outside the scope of conventional services trade negotiations, it is possible to widen the scope of FTAs. Recently negotiated FTAs such as CPTPP, Canada-EU, and EU-Japan are tackling the issues of regulatory transparency, regulatory coherence and regulatory cooperation by providing (i) an independent chapter which applies to the whole services sector; (ii) detailed disciplines in sectoral chapters (e.g. express delivery financial services, telecommunications, and postal and courier) and electronic commerce; and (iii) co-operation on competition policy and state-owned enterprises and designated monopolies.[13]

From the discussion above, we see that the main benefit of services trade agreements (GATS and FTAs) is to legally bind the existing legal regime in terms of market access and national treatment. We call this a ‘lock-in’ effect. FTAs can give services providers preferential ‘legal certainty’ by locking in more policies, or more liberal positions, than in GATS commitments, but mostly only in the context of market access and national treatment under applied services trade policy.[14] Recently concluded FTAs are trying to reduce legal uncertainty, as well as ease the path for international trade, by providing disciplines for regulatory cooperation and by extending the scope of services agreements.

The evidence above suggests that FTA services negotiations are not strongly liberalising. Countries do not bind a higher-level of liberalisation in FTAs by changing their applied services regimes. Rather, they prefer to retain a certain degree of policy space. In this section, we analyse three features of services negotiations that hinder liberalisation, be it in multilateral, plurilateral or bilateral talks.

Services trade negotiations require extensive technical knowledge and experience due to the wide range of services and their complex regulatory requirements. The GATS covers 12 sectors (business services; communication services; construction services; distribution services; educational services; environmental services; financial services; health-related and social services; tourism and travel-related services; recreational, cultural and sporting services; transport services; and other services), which are further divided into over 150 subsectors.[15] Services trade negotiations cover four modes of supply cross-border supply (mode 1); consumption abroad (mode 2); investment (mode 3); and movement of natural persons (mode 4).[16] What is more, for many services, modes of supply have been changing over recent decades in response to technological progress and the diffusion of information and communications technology.[17] Changes in modes of delivery affect domestic regulatory authorities’ policy interests and the business sector’s demands on negotiations. Such dynamism increases the need for in-depth analysis of the economics of services and technical legal knowledge to associate economic realities with a services trade agreement (e.g. structure, scope, definition, disciplines and methods of commitments).

The domestic decision-making required for services trade negotiations is more complicated than for goods trade negotiations. In the case of goods, where the focus is conventionally tariff reduction/elimination, a focal point for negotiations is clear – the Ministry of Trade. In comparison, services trade negotiations are all about regulations. The services sector is more institutionally dependent on regulatory authorities than other sectors because market failures such as imperfect and asymmetric information are so pervasive.[18] Accordingly, more actors are involved in domestic decision-making, especially in federal states where the horizontal and vertical fragmentation of power diffuses responsibility for service sectors. During the domestic coordination process, regulatory authorities tend to be conservative, resisting the policy changes required by services trade negotiations. This is because their main task is to avert market failures, which induces a strong tendency towards risk aversion. It is very difficult for the Ministry of Trade, which has no regulatory autonomy, to overcome this fragmentation of power and risk aversion unless it receives very high-level political backing.[19]

The degree of services liberalisation to aim for, and the measure of liberalisation achieved, are not as clear as numerical tariff reductions/eliminations in goods liberalisation. This is because trade and investment in services are affected by a variety of domestic regulations, which constantly evolve to reflect technological progress. The regulations that inhibit market access in the GATS (e.g. share of foreign ownership and the total number of services operations) represent just a subset of actual trade barriers. In practice, other types of barriers, such as regulatory divergence; transparency of qualification requirements and procedures, technical standards and licensing requirements; measures which restrict competition; and domestic regulations that are more burdensome than necessary (although considered as legitimate in terms of market failures), have to be tackled together to achieve substantial services liberalisation. This means that even if a trade partner fully commits to GATS style market access without any limitations on national treatment, as long as other types of measure prevail, business cannot gain actual benefits from services trade negotiations.

In addition to these three complications that services trade negotiations face, economic and legal factors dilute a country’s incentives for promoting services trade liberalisation in FTAs.

Different countries have different interests in services liberalisation from a purely mercantilist point of view. The US and European countries are major services exporters and thus have a strong interest in opening up other markets.[20] The rest of the world, on the other hand, except for a few specific cases (e.g. China, India, Japan, Singapore and Hong Kong) have little capacity to provide international-quality services and so feel that they have little to gain from FTA services liberalisation. This is especially true for developing countries, which, with the exception of Mode 4 (the movement of natural persons), see few opportunities for strong export growth. And, of course, developed countries typically tend to be very miserly with their offers in Mode 4.

From the legal point of view, Most Favoured Nation (MFN) clauses in existing FTAs tend to erode a country’s incentives for making more liberal commitments with a new FTA partner. MFN clauses in a FTA prevent the signatory countries from creating any discriminatory conditions as a consequence of granting better deals to future FTA partners. They require that better deals made in future FTAs be automatically extended to the original FTA partners. MFN clauses are found in many FTAs concluded by developed countries, although the scope and depth of provisions vary in accordance with the level of development of their FTA partners. For example, the FTAs concluded by the USA mostly include MFN clauses. The MFN clause in the revised NAFTA (the United States-Mexico-Canada Agreement – USMCA) covers cross-border services trade, investment, and financial services.[21] Likewise, FTAs concluded by the EU include MFN clauses in selected modes or sectors.[22] For instance, MFN clauses in the Canada-EU Comprehensive Economic and Trade Agreement (CETA) cover investment, cross-border trade, and financial services.[23] Also, Japan includes MFN clauses in most of its FTAs. The strongest MFN clauses can be found in the FTA with the EU (the EU-Japan Economic Partnership Agreement), where MFN is applied to investment (both establishment and operation) and cross-border trade in services.

Based on the general observations above, we now examine the prospects of Britain’s future services trade deals with non-EU countries.

First, note that the UK government’s apparent decision to leave the EU single market for services while remaining in the customs union for goods means that the UK cannot include goods in its trade agreements for the foreseeable future, and thus needs to negotiate stand-alone services agreements. To date, not even a single comprehensive stand-alone services FTA has been notified to the WTO.[24] That is, any future UK FTA with non-EU countries would become the first services-only FTA in history. Excluding goods restricts the ability of FTA partners to make cross-cutting deals, such as committing to market access in mode 3 in services in exchange for the UK eliminating tariffs in agriculture/manufacturing goods.

Second, FTA partners will tend to have rather limited incentives for liberalisation in services. The UK’s fierce competitiveness in services trade means that UK business will be rooting for big liberalisations, but for many prospective non-EU partners, this is a problem. Even if they have the political will to start FTA negotiations with the UK, resistance from the local providers who fear being out-competed is likely to slow the negotiations down. Moreover, as Figure 2 demonstrated, most countries do not even make commitments in some of the sectors where the UK has strong export interests, such as broadcasting; motion pictures; sound recording; and maritime transport.

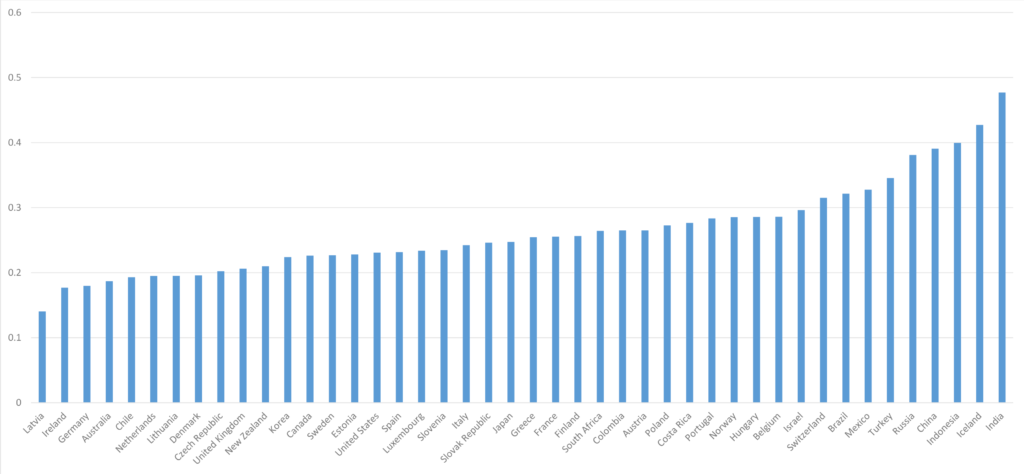

A further challenge is that the UK’s de facto open services economy limits the menu of concessions that it can offer in services to encourage them to reciprocate. According to the OECD STRI [25], the UK is the 10th most open market for services (Figure 5), so there is not much scope for further opening in general. But, in fact, much of the restrictiveness that the UK does impose is due to Mode 4 – the movement of natural persons. Particularly, in the case of developing countries, their only interest in services trade negotiation lies in exporting services providers (e.g. IT professionals, engineers, nurses, doctors, careers, cooks, building site workers, dance teachers and childminders). They will ask the UK government to commit preferential market access and visas in return for opening their own services markets. It does not take much experience of the current UK government policy to understand that this is not likely to yield much response.

Finally, the UK will not be immune from the intra-governmental coordination problems highlighted above, so generating cross-sectoral or cross-modal concessions within services trade negotiations will be difficult. With so many veto players, each seeing only one part of the negotiation, the government will need an ‘all-of-government’ approach to services trade negotiations. This requires strong leadership from the top and very large amounts of coordination and persuasion from the Department for International Trade. The latter needs to engage frequently with the many parties involved to understand their concerns and technical constraints in the process of constructing packages that will be attractive to negotiating partners. This process requires both time and resources. Given the lack of attention to detail that has characterised the UK government’s positions over the Brexit process, the lack of focus on services sectors in general and the political pressures towards striking early trade agreements with non-EU partners, it will be a major challenge to achieve meaningful services liberalisation in bilateral deals over the next few years. Indeed, rather than seeking quick but shallow trade agreements, the UK government would do well to devote its resources to trying to evolve the complex machinery required for significant services agreements in the medium term.

All told, the unique complexities of services trade negotiations, mean that the UK cannot expect to liberalise FTA partners’ markets for services beyond their applied services trade policy levels. There is a huge policy space between the GATS commitments and applied policy, and whilst FTAs can narrow this space they hardly ever eliminate it, even under favourable conditions. The most one can reasonably expect of FTAs, in reality, is just to provide a higher level of legal certainty that applied policies will remain in place than the GATS can provide.

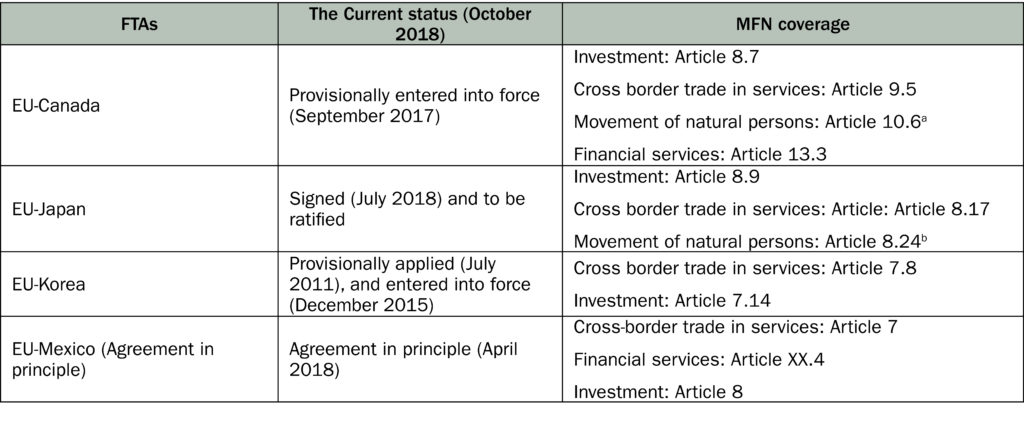

The UK cannot expect a higher level of services commitments from future FTA partners than the EU has achieved or will have achieved in its FTAs. From a legal point of view, the MFN clauses in the EU’s existing and future FTAs will be a stumbling block for the UK. Those countries which have already concluded an FTA with the EU, such as Canada, Japan, Korea and Mexico, will hesitate to offer a higher level of commitments to the UK, because the MFN clauses require any better offer to be immediately shared with the EU, an economy six times larger than the UK. Moreover, such concessions would be less attractive to the UK because it would have to share its preferential benefits with the EU 27. All this means that it is highly unlikely that the UK’s future services trade deals will be superior to the EU’s FTAs. The only realistic hope lies in the (relatively limited) set of services areas in which MFN clauses do not apply – see Table 1.

There are 13 countries/economic blocks which are currently negotiating an FTA with the EU. These include the countries/economic blocs of high interest to the UK, such as Australia, Mercosur, New Zealand, and India.[27] If the EU concludes FTA negotiations with these countries before the UK concludes its FTAs with them, the MFN clauses will spring into action. And even if the EU does not conclude negotiations before the UK, these partners will be wary of creating a precedent with the UK that they are not prepared to extend to the EU.

a,b, The MFN coverage is within a limited scope and definition.

Note: the EU-Singapore FTA (concluded negotiations in April 2018, to be ratified) does not include MFN clause.

The empirical evidence shows that FTAs are unlikely to achieve a higher level of liberalisation than actual applied services trade regimes. The role of FTAs, in practice, is to provide a higher level of legal certainty to business activities than the GATS can provide. Services trade liberalisation is difficult to achieve because of the distinctive nature of services trade negotiations. The UK will not be exempt from these difficulties when it comes to negotiate services trade deals with non-EU countries. In addition, we have highlighted a number of further challenges that the UK faces, including its inability to offer tariff concessions on goods, its currently already liberal stance in services, and the fact that future partners will have little incentive to make concessions beyond those they have already made to the EU.

Thus, it will be very difficult for the UK to (i) liberalise its trade partners’ markets for services more than their applied policy levels; and (ii) achieve a higher level of liberalisation than the EU has achieved/will have achieved prior to the UK negotiating its own FTAs. That is, advancing the export opportunities for UK services providers beyond their current levels will be very hard.

In short, while future UK FTAs in services with non-EU countries would be able to provide certain positive impacts on business activities by ensuring greater legal certainty than is provided by the GATS, these will be limited and will certainly not be sufficient to recoup the losses in services trade that will arise from terminating the UK’s membership of the EU Single Market in services.

Borchert, I, Gootiiz, B and Mattoo. A. (2011), Services in Doha: What’s on the Table?, Chap. 5 in: Will Martin and Aaditya Mattoo (Ed.), Unfinished Business? The WTO’s Doha Agenda, London: CEPR and World Bank, pp. 115-143.

Borchert, I. (2016). Services Trade in the UK: What Is at Stake?, Briefing Paper 6, UK Trade Policy Observatory.

Borchert, I and Tamberi, N (2018). The engagement of UK regions in Mode 5 services exports, Briefing Paper 22, UK Trade Policy Observatory.

Copeland, B. and Mattoo, A. (2008). The Basic Economics of Services Trade. In Mattoo, A. Stern, R. M and Zanini, G. (Ed.). A handbook of international Trade in Services (pp.84-129). Oxford University Press.

Francois, J. and Hoekman, B. (2009). Services trade and policy, Working Paper No.0903, March 2009, Department of Economics, Johannes Kepler University of Linz.

Hoekman, B (1996). Assessing the General Agreement on Trade in Services, in: Will Martin and L. Alan Winter (Ed.). The Uruguay Round and the developing countries, Cambridge: Cambridge University Press, pp. 88-124.

Kalinova, B., Palerm, A., and Thomsen, S. (2010). OECD’s FDI Restrictiveness Index 2010 Update, OECD Working Papers on International Investment 2010/03, OECD.

Lamprecht, P. and Miroudot, S. (2018). The Value of market access and national treatment commitments in services trade agreements, OECD Trade Policy Papers No. 213.

Magntorn, J. (2018). Most Favoured Nation clauses in EU trade agreements: one more hurdle for UK negotiators, Briefing Paper 25, UK Trade Policy Observatory.

Magntorn, J and Winters, L. A. (2018). European Union services liberalisation in CETA, Working Paper Series 0818, Department of Economics, University of Sussex.

Marchetti, J. and Roy, M. (2008). Services liberalization in the WTO and in PTAs, in J, Marchetti and Roy, M. (Ed.), Opening Markets for Trade in Services, Countries and Sectors in Bilateral and WTO Negotiations, Cambridge University Press, pp. 61-112.

Mattoo, A. and Fink, C. (2004). Regional Agreements and Trade in Services: Policy Issues. Journal of Economic Integration, 19 (4), 742-779.

Mattoo, A. (2005). Economics and Law of Trade in Services. World Bank Working Paper, February 2005. Washington. D.C.: World Bank.

Mattoo, A. and Amin, M. (2006). Do Institutions Matter More for Services?, World Bank Policy Research Working Paper 4032. Washington. D.C.: World Bank.

Mattoo, A. and Sauve, P. (2008). Regionalism in Services Trade. In Mattoo, A, Stern, R. M., and Zanini, G. (Ed.). A handbook of International Trade in Services (pp.84-129). Oxford; New York: Oxford University Press.

Mattoo, A. and Sauve, P. (2010). The Preferential Liberalisation of Services Trade. NCCR Trade Regulation, Working Paper 2010/13.

Mirodoudot, S. et al. (2011). Multilateralising regionalism; how preferential are services commitments in regional trade agreements?, OECD Trade Policy Papers, No. 106, OECD.

Miroudot, S. and Shepherd, B. (2014). The paradox of ‘preferences’: regional trade agreements and trade costs in services, The World Economy, Vol.37/12, John Wiley & Sons, pp. 1751-1772.

Miroudot, S. and Pertel, K. (2015). Water in the GATS: Methodology and results, OECD Working Party of the Trade Committee, TAD/TC/WP(2014)19/FINAL.

Morita-Jaeger, M. (2016) Services trade integration in East Asia and political economy impediments in domestic decision-making: a case study of Japan-ASEAN bilateral free trade agreements. The London School of Economics and Political Science (LSE).

OECD (2018). OECD Services Trade Restrictiveness Index: Policy trends up to 2018, January 2018.

Roy, M. (2011). Services Commitments in Preferential Trade Agreements: An Expanded Dataset, WTO Staff Working Paper, ERSD-2011-18, World Trade Organization. *Roy assessing only market access

Roy, M. (2012). Services Commitments in Preferential Trade Agreements: Surveying the Empirical Landscape, Working Paper No 2012/02 January 2012, nccr Trade Regulation.

VanGrasstek, C. (2011). The Political Economy of Services in Regional Trade Agreements. OECD Trade Policy Working papers No. 112.

Winters, L. A. (2018). What about the remaining 80 percent –Services? The ‘Customs Union’ and ‘Unilateral Free Trade’ share the same flaw, UKTPO blogs, 5th July, 2018. At: https://blogs.sussex.ac.uk/uktpo/2018/07/06/what-about-the-remaining-80-percent-services-the-customs-union-and-unilateral-free-trade-share-the-same-flaw/

[1] In WTO terminology a trade agreement in services is referred to as an Economic Integration Agreement (EIA), but we adopt the more popular usage in which the term FTA covers either or both of goods and services.

[2] Countries legally bind liberalisation commitments in terms of Market Access and National Treatment within the context of Article XVI (Market Access) and Article XVII (National Treatment) of the GATS. Therefore, restrictiveness in the GATS covers measures within the context of Market Access and National Treatment. Limitations on MA include: the number of services suppliers; the total value of services transactions or assets; the total number of service operations or the total quantity of service output; the total number of natural persons who may be employed in a particular service sector; the types of legal entity or joint venture through which a service may be supplied; and the participation of foreign capital. National Treatment calls for foreign providers to be treated no worse than domestics ones and applies to the sectors inscribed in a schedule of commitments subject to any conditions and qualifications set out therein.

[3] See Mirodoudot, S. and Pertel, K. (2015). The study used the OECD Services Trade Restrictiveness Index (STRI) to evaluate restrictiveness of applied services trade policy. Scoring relies on a careful reading of regulations and policies by economists and lawyers. Each of many elements is scored as restrictive (1) or not (0) and the overall score derived as a weighted sum of the parts scaled to range from 0 (no restrictions) to 100 (total restriction). The coverage of restrictiveness in the STRI stretches beyond the GATS market access and national treatment measures. In addition, it covers ‘domestic regulation inside/outside the scope of the GATS and other measures’. The study shows that 60% of the values of STRI indices is about market access and national treatment related restrictions.

[4] The OECD study refers to ‘policy space’ between the GATS commitments and applied policy as ‘water’ in the GATS. The water is measured as the average difference observed across countries between the maximum restrictiveness allowed in the GATS Trade Restrictiveness Index made by the authors and a simple average of the STRI (Miroudot and Pertel 2015, p11)

[5] The countries are: Australia, Austria, Belgium, Canada, Chile, China, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, India, Indonesia, Ireland, Israel, Italy, Japan, Korea, Luxembourg, Mexico, Netherlands, New Zealand, Norway, Poland, Portugal, Russia, Slovak Republic, Slovenia, South Africa, Spain, Sweden, Switzerland, Turkey, the UK and the US. STRI in 2014 was used for the study.

[6] Borchert, I, Gootiiz, B and Mattoo. A. (2011)

[7] Borchert, I, Gootiiz, B and Mattoo. A. (2011).

[8] See more detail about methodology: http://www.oecd.org/tad/services-trade/methodology-services-trade-restrictiveness-index.htm.

[9] See Roy, M. (2011) and (2012).

[10] https://www.wto.org/english/tratop_e/serv_e/dataset_e/dataset_e.htm

[11] According to Lamprecht and Mirodout (2018), ‘it is not very common to find such preferences in services trade agreements but there are a few cases’ (p9).

[12] See Mirodout and Pertel (2014). In the STRI, ‘other measures’ include ‘domestic regulation’ in the context of the GATS (GATS VI: Domestic Regulation) and outside the scope of the GATS.

[13] Although the revised NAFTA (United States-Mexico-Canada Agreement) does not promote regulatory cooperation horizontally (i.e. universally), it provides the disciplines in telecommunications, financial services, and digital trade. The Agreement also covers competition policy and monopolies and state enterprises.

[14] Lamprecht and Miroudot (2018) observed that additional legal certainty in FTAs has a positive impact on trade. “Going from the level of commitments observed on average in GATS to the average level in RTAs is associated with a significant positive impact on trade in the range of 8% to 12% depending on the sector”. (p19).

[15] The Services Sectoral Classification List (W/120), which was introduced during the Uruguay Round, has been used as a principal classification system in services trade negotiations.

[16] In addition, economic studies identify the growing role of Mode 5: services traded as embodied inputs into a country’s merchandise exports, although these are not negotiated directly. See Borchert and Tamberi (2018).

[17] For example, legal services used to be provided only by mode 4, but it is provided via internet (mode 1 and mode 2).

[18] Mattoo and Amin (2006).

[19] See Morita-Jaeger (2016).

[20] The US is the largest services exporter (14.3% of the global services exports), followed by the UK (6.7%), Germany (5.7%), and France (4.9%).

[21] See Chapter Cross border trade (Article 15.4); Chapter Investment (Article 14.5), and Chapter Financial services (Article 17.4). The previous NAFTA covers all services trade commitments (Article 1203, ‘[e]ach Party shall accord to service providers of another Party treatment no less favorable than that it accords, in like circumstances, to service providers of any other Party or of a non-Party)’.

[22] See: Magntorn (2018).

[23] See Table 1.

[24] Exceptions are bilateral investment treaties, bilateral or plurilateral mutual recognition agreements under the GATS VII, bilateral air services agreements, and the EEA agreement.

[25] The OECD STRI now covers 22 sectors across 44 countries, which account for over 80% of global services trade.

[26] http://www.oecd.org/tad/services-trade/services-trade-restrictiveness-index.htm.

[27] 13 countries which are negotiating an FTA with the EU include: ASEAN, Australia, Chile, India, Indonesia, Mercosur, Malaysia, Morocco, New Zealand, Philippines, Tunisia, and Viet Nam. China is negotiating the China-EU Investment Agreement. From the European Commission website (http://trade.ec.europa.eu/doclib/docs/2006/december/tradoc_118238.pdf)

[28] The MFN coverage is within a limited scope and definition.

[29] The MFN coverage is within a limited scope and definition.