In recent years the UK has confronted a series of non-trivial challenges such as Brexit, the Covid-19 pandemic, the Ukraine-Russia war and the cost-of-living crisis. Such issues pose serious challenges for the Government, but the consensus is that a big push is needed to boost economic growth. Now the UK government has an independent trade policy, the question arises “what might trade do to help increase economic growth?”

This briefing paper sketches the main lessons from the literature on international trade and economic growth. Starting with an overview of the main macroeconomic models of growth, it first looks at the cross-country evidence related to trade liberalisation and economic growth. Recognising how innovation and increase in productivity create change in long-run growth, the paper then reviews the microeconomic literature, studying the effects of trade openness on firm-level outcomes. It focuses on firm-level total factor productivity, market power and innovation, looking at the evidence regarding goods and services trade liberalisation, as well as the presence of foreign-owned firms. Finally, it distils a few high-level policy lessons from this literature.

This Briefing Paper provides a quick guide for policymakers on what we do and do not know about trade and growth, rather than a comprehensive review. No one believes that trade policy is the only tool, or the main one, to address economic growth. However, it clearly has a role to play both directly and indirectly, because inappropriate trade policy can render other growth-focused policies less effective.

Every politician knows that growth comes from investment. By increasing investment, we can endow each worker with more capital and increase labour productivity. However, this process cannot run forever, and will eventually run out of steam. We can equip a worker with one hammer, and this will increase his productivity compared to hammering nails by hand. Equipping him with a second hammer, however, will not increase his productivity much further. This is the decreasing marginal return on capital: the more you have of something, the less useful additional units of it become.[1]

To boost growth further we need another ingredient: technical progress. This is the key ingredient that can promote sustained growth in the long run by increasing efficiency. Here we must distinguish between what economists call “exogenous” and “endogenous” technical progress. Exogenous progress is generated by some process not included in the economist’s model, for instance, a random discovery such as penicillin. On the other hand, endogenous progress responds to some behaviours included in the model.

Growth is likely to be spurred by a single instance of exogenous technical advancement and although such advancement will increase the level of income, its impact on growth will eventually cease as the new equilibrium is reached. Such transition dynamics can be long – so long that we often cannot tell from data whether higher growth is transitory or permanent. However, in the absence of any further innovation, the higher growth rates will eventually return to normal.

When talking about capital, we should distinguish between physical and human capital. The main difference between the two is that humans can think, and by doing so they can innovate.[2] Raising human capital may raise the rate of innovation with new inventions arriving more frequently. This in turn will allow us to sustain a higher economic growth rate in the long run. Technical progress can include developing a better understanding of how to mix or organise a known set of inputs, and indeed, such advances can often lead to much better outcomes.[3] Good management can be another way of boosting economic performance.[4]

Endogenous technical progress has both direct and indirect effects. The indirect effects of some of the elements such as R&D and human capital, are likely to have spillover effects leading to further growth. Indeed, some innovations have found applications beyond the original scope for which they were developed, sometimes revolutionising other sectors or ways of doing things (e.g., the internet). While incentives to invest and innovate are internal to the firm, they can affect others and generate further growth. This type of outcome is generally accounted for in most growth models as they focus on aggregate effects.

International trade, as well as other disruptive transitions, creates winners and losers.[5] Some firms will be kicked out of the market, while some workers will lose their jobs due to globalisation. One of the key conditions to make trade more effective is ensuring that displaced factors will be re-employed efficiently – meaning that the labour market functions efficiently. A key role that policy can play in ensuring that trade policy contributes to growth is to ensure that it does so. This can be done, for example, via re-training or job-search centres, but also in more fundamental ways like addressing frictions in the property market. An example of a policy instrument that works in this way is the European Union’s European Globalisation Adjustment Fund for Displaced Workers.

Re-employing factors is not just about labour, however. While possibly politically less pressing, an efficient reallocation of capital is also crucial for sustaining long-term economic growth.[6] Refurbishing capital might be easier than labour – it does not object to being moved – and the market forces might just be able to find a new efficient equilibrium. However, if there is misallocation, policies that incentivise an efficient reallocation of capital might be warranted, including removing policy-imposed frictions. Examples of such misallocation include super-low interest rates that keep zombie firms alive, laws that make closing down slow or expensive, and infrastructure policies that maintain service for existing firms but do not admit new firms. Governments need to address frictions both in capital markets and in labour markets. Indeed, an efficient allocation of capital can lead to substantial increases in productivity.[7]

In some cases, an efficient short-run reallocation might not yield the desired outcome in the long-run. Such a paradigm is represented by the “comparative advantage trap”: a country develops a comparative advantage in a slow-growing sector, which then attracts even more resources, thus slowing down aggregate economic growth. This is essentially an inter-temporal misallocation of resources. The comparative advantage trap is often seen in terms of capital vs labour-intensive sectors but should not be limited to the capital/labour comparison. For instance, if the capital-intensive sector grows faster than the labour-intensive one, a labour-abundant country specialised in the production of the labour-intensive sector will grow at a slower rate than the capital-abundant economy specialised in the capital-intensive and high-growth sector. Similar situations can arise with respect to the labour force: policies that attract certain types of workers (e.g., high vs low skill) can steer the economy towards different types of specialisations and different long-run growth rates. For instance, if a country has a comparative advantage in low-skill tasks, it will not attract high-skill workers. This will make it harder to move towards the high-skill sector. If the low-skill sector has small growth compared to the high-skill sector, a comparative advantage trap arises. As the definition of “high skill” is not ubiquitous, what types of skills/tasks are attracted into the country will matter. Attracting lawyers or software developers will most likely have different consequences for innovation.

Another allocation decision to be made is regarding the resources devoted to innovation. How many scientists should we have? The Covid-19 pandemic certainly taught us that having scientists around is beneficial. At the same time, the economic system may lose efficiency beyond a certain level of resources being allocated to innovation rather than production.[8]

How does trade fit into this framework? Trade can help by making new or different intermediate inputs available to firms, or by enlarging the market, including for ideas. For instance, tariff cuts will make imports cheaper allowing firms to source their inputs from a larger pool of products. This is mainly an allocation effect, and such changes will lead to higher growth only for a finite period. At the same time, numerical simulation exercises suggest that such transition dynamics can last for decades.[9] Moreover, cheaper and more intermediate inputs can render some previously prohibitively costly production processes feasible, effectively changing production technology.

Trade can be important for generating technical progress within the country. A larger market offers larger returns to innovation. In addition, given that investment in innovation requires upfront fixed costs (such as setting up a laboratory in the chemical industry), being able to sell beyond the home market allows firms to spread the fixed cost across more output. In this case, increasing returns to scale plays a key role.[10] It is also possible that access to larger markets incentivises firms to increase their investments.

Also, trade openness can increase competition in the final goods market, leading to a reduction in the market power of incumbent firms and the reallocation of resources towards more efficient firms.[11] It can also push firms to innovate to remain competitive in the medium to long run. On the input side, having access to a larger pool of intermediate inputs can increase productivity by finding a better mix or by reducing their price via increased supply. Indeed, one of the main effects of trade restrictions is to reduce the supply of intermediate goods.[12]

Importing ideas can certainly benefit economic progress. At the same time, exporters of ideas must be protected if we want to encourage the development of any new ideas. Here is where intellectual property rights come into play, and where trade agreements can ensure the free flow of ideas while rewarding producers appropriately.

There is a vast empirical literature on how international trade affects growth. The evidence is mostly in favour of a positive association, with trade generating higher growth rates.

There are two distinct branches within empirical literature: macro and micro studies. Macro studies generally draw from cross-country comparisons over long periods of time. There are two main advantages when choosing macro over micro studies. First of all, growth is an aggregate phenomenon. Measurement at the aggregate level allows us to focus on the net effects of the potential conflicting effects of trade on aggregate growth. For instance, trade often has reallocation effects. Through aggregate data, we can see its net effects – i.e., which effect dominates. Second, macro studies can cover long time periods, hence allowing one to study growth in the long run. The downsides of the macro approach include issues with the measurement of trade openness and the ability to identify or separate out the causal effects of trade on economic growth from other confounders.

Pinning down a particular mechanism at play from aggregate data can be difficult. In contrast, micro studies – often conducted with industry or firm-level data – allow one to focus on particular channels via which trade affects productivity, prices or markups, in isolation from aggregate effects that can confound the analysis of data. However, it is often difficult to recover aggregate effects. Moreover, micro studies often focus on “case studies” – even if they involve all firms in a country – in the sense that they generally focus on a particular policy instance in a particular country. This is not bad per se, as it allows us to study the policy in a more detailed way. However, when reviewing the micro literature we houldd ask ourselves whether the experience of a particular country during a certain moment in time is relevant for other situations. In this sense, micro studies can support macro ones but do not substitute them.

However, the main issue with micro studies concerns structural effects. It is possible that trade liberalisation increases productivity in all sectors, while aggregate productivity decreases. This would be the case if the overall mix of sectors changes in a way that low-productivity sectors gain market shares at the expense of high-productivity sectors, and that the rise in productivity of the low-productivity sectors is not enough to overcome the adverse reallocation effect.[13]

In general, the empirical literature finds that international trade has a positive effect on aggregate economic growth. At the same time, some measurement and methodological issues prevent us from being entirely certain about this relationship and its magnitude. In the data, trade and growth are positively related, but the main concern is attributing causation: does trade induce more growth, or is the positive relation between trade and growth, the reverse or only spurious?

One strand of the literature uses indicators that classify countries as open or not open to trade and compares the growth of open and non-open countries.[14] To understand the meaning of open and closed, consider the index of Sachs and Warner (1995). According to this index, a country is closed if one of the following is true: (i) average tariffs above 40%; (ii) more than 40% of imports covered by non-tariff barriers; (iii) socialist economic system; (iv) the black market premium on the exchange rate is above 20%; and (v) the majority of its exports are under the control of a state monopoly. A country is open if none of these conditions apply. Most of the studies employing these indicators find that open countries grow faster than non-open ones by about 1-2% p.a., with the 2% upper bound probably driven by temporary catch-up. These studies are often criticised because of the crudeness of the trade openness measure and their failure to control for other confounding factors.[15] Moreover, it should be recognised that going from closed to open involves many policy changes and thus makes attribution of the outcome to trade policy very challenging. Moreover, such changes are not something we have observed in advanced economies.

To isolate the causal link between trade and growth, economists looked at geography. The location of a country in the world is fixed, and it is well-known that distance affects international trade. At the same time, distance from large markets by itself should not affect growth by itself, and the only way in which it can affect growth is via its effect on international trade. This part of the literature finds that 1% extra openness increases GDP per capita by 1%.[16] It should be noted that these studies only inform us of the effect of trade volumes on growth, but not of the effects of trade policy on growth.[17]

Further evidence comes from changes in trade routes’ distance over time – such as the temporary closure of the Suez Canal – or changes in the price and mode of transportation – such as the shift from seaborne to airborne trade. Looking at changes over time in trade distance or cost allows one to net out much of the intrinsic cross-country variation in trade and growth that does not change over time and does not represent the causal relation between trade and growth. By eliminating this extraneous variation, researchers can reach more robust estimates of the effects of trade on growth.[18] These cross-country and cross-time comparisons find that trade has a positive effect on income. Also, the elasticity of income with respect to trade is estimated to be about one-half. It is smaller when we consider only trade in goods.

While the consensus is that trade is beneficial for growth, initial conditions matter. For instance, the initial level of income of a country can determine whether liberalisation will have a positive or negative effect on growth. In fact, researchers find that richer countries benefit more from openness than poorer ones.[19]

It is well established in the economic literature that the quality of institutions is fundamental for long-term growth. Institutions are also relevant for a country to be able to benefit from trade openness.[20] Moreover, evidence suggests that the effect of trade on growth can be negative if institutions are of low quality, since trade can exacerbate the adverse effect of other distortions.

Economic conditions also play a role. Flexibility in the business environment, labour market, low inflation and good governance are also conditions for a positive effect of trade on growth. Moreover, the complementarity of trade policy with other reforms appears to be important. Trade openness has smaller effects on growth when inflation is high. It is larger when progress is made in terms of human capital investments, financial markets depth and development of public infrastructures.[21] Similarly, corruption appears to be another factor that prevents countries from benefitting from increased openness.

A series of studies using firm-level data looked at instances of trade liberalisation of a particular country – firm-level datasets covering more than one country are rare. One common finding is that reducing tariffs on the intermediate inputs used by a firm increases its productivity. The lower cost of inputs (e.g., via a reduction in tariffs) or their wider availability (e.g., via a loosening of quantitative restrictions) means that the firm can free up some resources and it appears that they respond by reallocating inputs to increase their productivity. However, this could also reflect an increase in market power – see below.

A reduction in the output tariff (or other forms of protectionism) – which increases foreign competition in the domestic market – is also generally found to have a positive effect on firms’ (and certainly sectors’) productivity.[22] Relatively speaking, input liberalisation generally appears to have a larger effect than output liberalisation – about twice as much.[23]

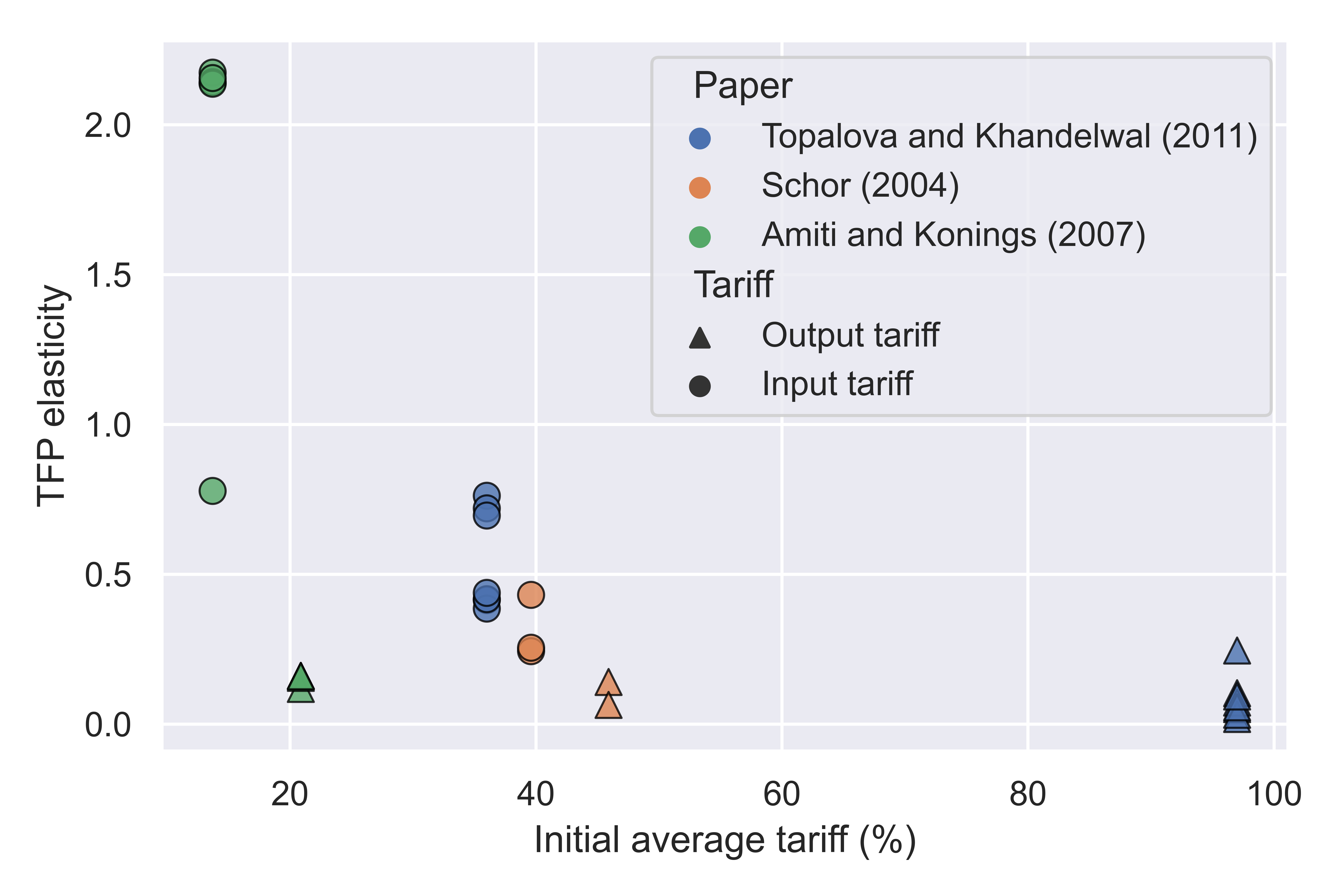

To illustrate the effects of tariff liberalisation of TFP, we take three studies which use a similar methodology and compute the elasticity of TFP with respect to tariff changes.[24] The elasticity tells us the percentage change in productivity given by a 1% change in the tariff. It is therefore a unit-free measure that allows us to make comparisons across studies. Figure 1 plots the TFP elasticity against the initial tariff level. The TFP elasticity is higher the lower the initial tariff level and there are differences between input and output tariffs. Based on these results, we can infer that at an initial tariff (both input and output) of 5%, a 1% reduction in the input tariff increases TFP by 2.4%. Whereas a 1% reduction in the output tariff increases TFP by 0.16%.[25] A caveat to this relationship is that it is based on only three studies and should be interpreted with caution.

Figure 1: TFP elasticity and initial tariff rate across selected studies

Source: author’s calculation based on estimates and summary statistics reported in Amiti and Konings (2007), Topalova and Khandelwal (2011) and Schor (2004). The figure plots the calculated elasticity of TFP with respect to tariff against the initial tariff rate.

Export liberalisations (a reduction in trade barriers by a foreign economy) could also affect productivity. For instance, by enlarging the output market, firms can have incentives to innovate and take advantage of economies of scale. An interesting question is whether import or export side liberalisations have different effects on productivity. Episodes of liberalisation occurring both ways are less frequent and are often due to two countries signing a trade agreement. Evidence from the Canada-US trade agreement suggests the cut in the import tariff on firms’ outputs kicks mid-productivity non-exporters out of the market. As a result, resources are reallocated towards more productive exporters. On the other hand, the cut in the export tariff leads more firms to export. It also increases productivity, innovation and adoption of advanced technologies.[26]

Within-firm responses to changes in trade policy are well-documented. At the same time, we observe aggregate productivity effects at the industry level. These effects are the result of intra-sectoral reallocations as well as within-firm responses. Firm-level studies often find important changes at the extensive margins, with firms entering and exiting the market. Most often, it is found that low-productivity firms are more likely to exit while high-productivity ones continue to function and possibly grow. This leads to increases in aggregate productivity at the industry level. It should be noted that while new entrants are generally small firms, hence not adding much in aggregate in the short run, they have the potential to expand quickly and therefore become significant in the medium to long run.

Competition in the domestic output market will push firms to reduce their output price to retain market share. This can be done in two ways: reducing markups or increasing efficiency.[27] Reducing markups is likely to have an immediate but short-lived effect: when a subsequent shock arrives the ability to reduce markups again will be limited. On the other hand, firms can invest in new technologies or managerial practices hoping that this will lead to higher productivity in the medium to long run, allowing it to retain demand. Investments in innovation usually take time to materialise, hence we should not expect to observe their effects immediately.

Most of the evidence on firm-level productivity looks at a revenue-based productivity measure. Such a measure can be divided into two components: physical efficiency (the ability to produce more units of output from a given set of inputs) and price markup. These two elements have potentially opposite effects on economic growth. More efficiency in input usage is likely to bring higher growth, although probably only temporarily. On the other hand, while an increase in the markups on exports will increase incomes rather than output, increasing markups, in general, will reflect increases in market power. These might or might not induce more innovation.

Separating efficiency and markups in the data is not straightforward, and data limitations often do not allow such calculation. The few studies that can do so show that a reduction in the tariff in the output market generates pro-competitive effects as firms respond by reducing their markups. However, at the industry level, these pro-competitive effects seem to come mainly from new entrants putting pressure on incumbent firms. On the other hand, a reduction in the input tariff has the opposite effect, as firms tend to respond by increasing their markups.[28]

This makes us re-assess the evidence discussed in the previous section on input and output tariffs. While input liberalisations tend to have stronger effects than output liberalisations, pro-competitive effects only occur via increased competition in the output market.

This suggests that the resources freed from the lower cost of inputs tend to end up as a transfer of welfare from consumers (lower customs tax revenues) to producers (higher markups). For non-tariff barriers (NTBs), and hence for services trade, it is a different story, as no tariff revenues are raised. These forms of trade protection often show up as rent for incumbents. While we lack research on this, it is possible that an increase in markups would not occur for NTBs, as cheaper inputs are offset by the loss of rent.

However, we should note that this literature is not yet very extensive so at the moment only a few studies are able to separate physical productivity from markups. More research on this matter is necessary to confirm or refute these results – or, more likely, sort out when one effect dominates the other.

As we have seen above, productivity measures typically reflect a mix of market power and efficiency components. Hence looking directly at innovation is a useful alternative. Results here are heterogeneous and most likely depend on the type of trade shock under scrutiny. If trade openness results mainly in increased competition in the output market, firms have an incentive to increase their investments in innovation to remain competitive in the medium run. On the one hand, if increased trade openness mainly comes from imports of intermediate inputs, the incentive for a firm to innovate is reduced.[29] On the other hand, the opportunities to innovate may increase – for example, importing certain digital services may allow a firm to increase its product quality or introduce new products.

Evidence from European firms’ responses to Chinese competition in their domestic output market shows that firms reacted by increasing their TFP, patents, IT intensity, R&D expenditure and management skills. On the other hand, evidence from China shows that after a reduction in input tariffs, firms responded by reducing innovation. This is because access to foreign products, and the technology that they embedded, already provided a way to increase efficiency. It is likely that such responses also depend on a country’s distance from the technological frontier. For an advanced economy, importing inputs from abroad might change the cost of inputs – cheaper inputs from developing countries – but it is unlikely to bring new technologies into the economy. Hence, the response to foreign competition can be to do more of what you are good at: high-tech products. On the other hand, for a developing country, opening up to trade with advanced economies allows firms to access advanced technologies that can be imported directly or embedded in equipment rather than developed in-house. This may be done because it is cheaper to import or because it is impossible to develop the same technology at home.

Many studies looking at instances of trade liberalisation focus on the import and domestic market channels. However, incentives to innovate can come from the export market as well. Access to a larger market means that fixed costs can be spread across more units of output. Given that investments in innovation largely involve fixed sunk costs, a trade liberalisation can induce firms to invest in innovation activities. Evidence from Argentina and MERCOSUR shows that when firms start exporting to a larger market, they increase their expenditure on technology.[30]

Innovation can take many forms. It can be investments in R&D, patents or expenditure on technology. However, strictly speaking, these are input measures used as proxies for innovation. In addition, we have evidence that trade openness can increase product quality as well as product scope.[31]

In terms of how firms respond to trade liberalisation, we have evidence of multiple channels being activated. Increases in competition push firms to innovate by registering more patents, increasing expenditure on R&D and IT intensity, changing management practices, and reducing prices and unit profitability. These changes tend to bring increases in labour and total factor productivity. Another channel of adjustment is the product mix, with firms changing the types or mix of products being produced.

However, the response to international competition is not the same for all firms. Domestic firms tend to respond in a greater way than multinationals, perhaps because the latter are already subject to international competition.[32] Input tariff liberalisations appear to boost sector-level productivity due to higher productivity of new entrants and, to a smaller extent, increased productivity of incumbent firms. Within-firm reallocations do not have large effects and the contribution of exiting firms is minimal. The effect of increased competition in the output market on average sectoral productivity comes almost entirely from the higher productivity of new entrants.

An output tariff liberalisation also has pro-competitive effects (i.e., reducing the average sectoral markup) that arise almost entirely due to the reduced markups of existing firms. On the other hand, input liberalisations have anti-competitive effects, which arise almost entirely because entering firms have higher markups than incumbents.[33]

There is also evidence that firms closer to the technological frontier choose to increase their productivity and grow after a rise in international competition. On the other hand, low-tech firms suffering from increased competition tend to respond by lowering employment and investment and exiting the market.

Comparisons of studies done for different countries show that the import competition effects tend to increase productivity but with differences across stages of development. The pro-competitive effects are large in developing countries and in Europe. However, there is mixed evidence for North America.[34]

Learning by exporting is the hypothesis that firms can become more productive because they export. Exposure to foreign markets can teach firms new insights, as well as push them to become more competitive to acquire foreign market shares. Empirically, the literature is not settled. While some evidence of learning by exporting exists, many studies do not find that firms become more productive by exporting and that causality runs from productivity to exporting. There are questions as to whether evidence of learning by exporting is specific to each case study – and hence not generalisable – or whether methodological issues prevent learning by exporting from being detected in the studies that do not find evidence for it.[35] Some evidence suggests that the type of innovation, whether radical or marginal, matters, with only radical innovation leading to more exports.[36]

What we know from firm-level studies mostly comes from manufacturing, but services matter too. The reason why services are less studied is data: services trade is not recorded via customs transactions, and it is much scarcer and coarser than goods trade data. Second, services are less traded than goods. Third, while quantity productivity is a well-defined concept for manufacturing firms, it is not so well-defined in the context of service producers. Finally, services trade policy began to be measured only recently with a Services Trade Restriction Index (STRI), which is not as easy to interpret as tariffs.[37]

However, services account for more than half of the economy in most advanced countries. Scholars investigated the effects between services trade and firm performance. Because of difficulties in measuring services firms’ productivity, most of these studies look at the effects of services trade on manufacturing firms. The channel explored is the use of services as intermediate inputs by manufacturing firms.

Services trade restrictiveness has negative effects on manufacturing productivity. Institutions play a crucial role in allowing manufacturing firms to benefit from a liberal services trade policy. For instance, and this is not a services-specific issue, widespread corruption and ineffective regulation can create economic uncertainty that offsets the positive effects of the liberalisation.[38] Moreover, a more restrictive services import policy has a dampening effect on the export of manufacturing firms; with the restriction of foreign entry (mode 3 restrictions) as the most important type of restriction.[39]

Evidence from services industries reform in India and the Czech Republic shows that allowing foreign companies into the services market – hence presumably increasing the scope and the quality of services products – can be strongly beneficial for the productivity of manufacturing firms using those services products as inputs.[40]

Digital services are increasingly traded internationally. While it is too early to have hard evidence on the effects of digital trade, it should not be ignored given its soaring importance in modern economies. Some emerging countries such as India and the Philippines have recently seen spectacular services export-led growth.

Digital services can, at least in part, be studied through the conventional trade and growth framework. While they will affect different branches of the economy than other past advances in manufacturing technology, the development of digital services trade will most likely work through the channel of comparative advantage, with associated gains from specialisation. It is possible, however, that compared to other technologies, digital services will have a more horizontal application, hence affecting many industries in ways that are still unknown.

Foreign direct investments do not matter only for services. Because of the large sunk cost required to set up foreign affiliates, firms investing in foreign subsidiaries are generally among the most productive. Allowing them into the country can raise the productivity of the sector simply because a more productive firm entered. Moreover, FDI can bring positive productivity effects to the rest of the economy if foreign firms can, directly or indirectly, pass some of their know-how to other firms – productivity spillover effects.

Such productivity spillovers can pass along the value chain, both to suppliers of the foreign subsidiary as well as to firms that purchase inputs from it. There is some robust evidence that direct links with the multinational (e.g., contractual links) allow some technology or know-how to be passed to domestic firms – so-called vertical spillovers.[41]

On the other hand, horizontal spillovers are not always detected in the data. These are spillovers to other firms in the same industry where the multinational operates, hence not along the value chain. Only a few studies find evidence for this, and the presence of horizontal spillovers might be conditional on the type of industry considered.[42]

Robust protection of intellectual property rights is key to attract foreign firms in the first place. Once they are in the country, they can bring to the economy productivity spillovers that go beyond IP-protected technology. For instance, contacts with domestic suppliers might teach domestic firms managerial best practices. Also, foreign multinationals can bring links to global supply chains and push domestic firms to engage more in international trade broadening their markets for output and inputs (network effects). Other channels via which FDI can bring positive productivity spillovers to the host economy are strategic partnerships, competition and imitation effects, and labour mobility.[43]

This section describes how trade policy can help in fostering growth. The policy suggestions are based on the evidence reviewed in the previous sections of this paper. Rather than suggesting specific policy tools, we present the key points that a policymaker should keep in mind while thinking about trade policy and growth.

In terms of fostering openness, trade policy can enter the scene in two places: barriers and uncertainty. The government can – but does not necessarily want to – remove trade barriers to facilitate international trade and increase openness. For a manufacturing trader, when customs tariffs are low already there are other trade policy tools that can give larger benefits, such as improving infrastructures, simplifying bureaucracy and access to information, and removing other forms of non-tariff barriers for traders. Certainty about the regulatory environment is also a key factor in promoting investments.

In removing barriers, policy should recognise the value of both liberalising imports and inward investments, as well as incentivising exports. When starting to trade there are fixed costs, which can relate to different issues such as access to finance and bureaucratic procedures, but also market- and product-specific barriers. Regulatory barriers can also be a deterrent to international trade. Additionally, gains from regulatory alignment and mutual recognition of standards with large trade partners should not be overlooked. Reducing fixed costs can help firms enter international markets and thus discover whether they can expand in this way. This will be especially true for small and medium enterprises.

In addition to reducing barriers, merely identifying, monitoring and reporting on trade barriers is a key part of trade policy. In order to support effective policy decisions, a complete and detailed knowledge of the status of existing trade barriers for different products and markets is fundamental to support effective policy decisions.

Trade policy, and trade agreements in particular, can reduce uncertainty around trading conditions. It is well documented that uncertainty about market conditions can deter investments, lowering participation in international trade. This is because when exporting involves high initial fixed sunk costs, the possibility of future restrictions in market access makes firms uncertain about recovering their initial investment via future cash flows. This applies especially to investment in innovation activities, which involve large initial investments and will offer benefits only in the medium run. Hence, a sound trade policy must be credible and stable. This requires the government’s ability to adapt to new shocks, keep good relations with trade partners and avoid large and unexpected swings in trade policy. Moreover, trade agreements can help remove or reduce uncertainty about market access by locking in trade policy commitments. In particular, the removal of uncertainty will be stronger when agreements cover issues such as customs formalities, standards and regulations, showing the full commitments of trade partners to keep the trading relations stable over time, and when formal dispute settlement and enforcement mechanisms are established through trade agreements.[44]

Beyond market access, trade agreements may play an important role in technology transfer. Chapters on intellectual property rights are required to ensure that developers of new ideas and inventions are rewarded appropriately and, at the same time, allow the free flow of ideas and technology so that innovation can take place everywhere. Similarly, chapters on digital trade and e-commerce often go beyond market access, covering issues such as cooperation in the development of new technologies or data sharing.

Apart from increasing openness, sharing the benefits of trade policy requires other policies to be in place. Coordination of policies across the whole policy spectrum is fundamental to bring growth and higher income for the country at large. As discussed already in this document, one of the key issues is monitoring the reallocation of resources and ensuring that displaced factors of production are re-employed efficiently. This will involve training and greasing the labour market with tools that facilitate job search, but without forgetting that capital must also be reallocated efficiently if we want investments in innovation activities to take place. This might involve setting up the correct form of incentives if the market fails to find an efficient equilibrium by itself. Moreover, addressing issues regarding infrastructure, bureaucracy, access to information and finance is a key factor in enabling firms to take advantage of policies concerning trade barriers. For instance, having proper infrastructures at the border ensures that customs formalities are dealt with smoothly, enabling the benefits of trade liberalisations to materialise.

Regarding the UK, its economy is open and has low tariffs. This suggests that further tariff liberalisations are unlikely to provide a large boost to productivity. Until recently, the country had low regulatory barriers with the EU, its largest and closest partner, and low services trade barriers, but this changed with the exit from the EU in 2020. The UK is highly specialised in services and advanced manufacturing. For manufacturing, this suggests that import competition effects will tend to push firms to innovate more and remain competitive. For the services sector, the evidence is too scarce to draw conclusions and we can only speculate based on the evidence for the manufacturing sector. In terms of productivity, the country has had low levels of within-industry productivity growth since the 2008-9 financial crisis.

Overall, trade policy is only one of the instruments available to policymakers to achieve higher economic growth. Importantly, trade policy by itself is unlikely to be sufficient and it should be applied coherently with other forms of policy interventions.

[1] Decreasing marginal return is at the core of growth models starting from Solow (1956).

[2] Sophisticated AI may be able to innovate in the future, but from the big bang until now innovation has been a prerogative of humans in this world.

[3] Romer (2008).

[4] Bloom et al. (2013).

[5] See Gasiorek et al. (2019) for a review of winners and losers of international trade.

[6] Capital does not vote, and those who own it count for fewer votes than workers; however, they are likely to be better connected politically.

[7] Hsieh and Klenow (2009).

[8] See Rivera-Batiz and Romer (1991a, b) and Grossman and Helpman (1995).

[9] Rutherford and Tarr (2002).

[10] Grossman and Helpman (1995)

[11] Melitz (2003)

[12] Romer (1994)

[13] McMillan and Rodrik (2011) refer to this phenomenon as structural change.

[14] Sachs and Warner (1995); Wacziarg and Welch (2003); Giavazzi and Tabellini (2005); Kneller, Morgan, and Kanchanahatakij (2008); Wacziarg and Welch (2008) and Billmeier and Nannicini (2009, 2011, 2013).

[15] Rodriguez and Rodrik (1999).

[16] Frankel and Romer (1999); Noguer and Siscart (2005) also control for geographical characteristics of a country that can influence economic growth independently of trade, such as being a certain latitude and spread of certain diseases.

[17] This point is raised in Frankel and Romer (1999) and reiterated in Rodriguez and Rodrik (2000).

[18] Feyrer (2019); Feyrer (2021).

[19] Dejong and Ripoll (2006) and Kim and Lin (2009) find that trade is beneficial only for high income countries. On the other hand, Van der Ploeg and Poelhekke (2009) – although not focussing particularly on trade and GDP – find the contrary.

[20] Bhattacharyya et al. (2009)

[21] Bolaky and Freund (2008); Chang, Kaltani and Loayza (2008)

[22] Bloom et al. (2016) ; De Loecker (2007)

[23] Amiti and Konings (2007); Topalova and Khandelwal (2011); Schor (2004).

[24] The three studies considered are Amiti and Konings (2007), Topalova and Khandelwal (2011) and Schor (2004). All three papers regress the log of TFP on input and output tariffs in levels, not in logs. Elasticities are computed by dividing the regression coefficient on input (output) tariffs by the percentage change in input (output) average tariff between the first and last year in the sample as reported in the summary statistics of each paper. Calculations are done for the main table of each paper only with specifications including both input and output tariffs (Table 4 columns 2-6 of Amiti and Konings; Table 5 of Topalova and Khandelwal; Table 5 of Schor). We exclude the results with positive coefficients on tariffs.

[25] The calculation is done by fitting a linear regression of TFP elasticity against initial tariff rates and a constant (separately for input and output tariffs) and extrapolating the TFP elasticity for a 5% initial tariff rate.

[26] Lileeva (2008); Trefler and Lileeva (2010)

[27] Goldberg and Pavcnik (2016)

[28] De Loecker et al. (2016); Brandt et al. (2017)

[29] Bloom et al. (2016) for European firms; Qing and Qiub (2016) for Chinese ones.

[30] Bustos (2011)

[31] Fan et al. (2015); Goldberg et al. (2010)

[32] Topalova and Khandelwal (2011).

[33] Brant et al. (2017) and the subsequent corrigendum. The effect of competition on new firms is presumably to prevent them from appearing. Brant et al. decompose changes in industry-level markups and productivity across four margins: changes within continuing firms, reallocations between existing firms, entry and exit.

[34] Shu and Steinwender (2019).

[35] Wagner (2012), De Loecker (2007); Van Biesebroeck (2005); De Loecker (2013); Syverson (2011); Trefler and Lileeva (2010); Garcia-Marin and Voigtländer (2019)

[36] Jibril and Roper (2022)

[37] See Borchert et al. (2012) for the World Bank STRI; see Nordås and Rouzet (2015) for the OECD STRI.

[38] Beverelli et al. (2017)

[39] Hoekman and Shepherd (2017)

[40] Arnold et al. (2011); Arnold et al. (2014)

[41] For instance, Javorcik (2004)

[42] Javorcik (2004); Newman et al. (2015); Di Ubaldo and Siedschlag (2022); Kneller and Yeaple (2009). Kneller and Yeaple (2009) find evidence of horizontal spillovers for high-tech industries in the US but not for other industries.

[43] See https://www.oecd-ilibrary.org/sites/51a9f5d3-en/index.html?itemId=/content/component/51a9f5d3-en

[44] Handley and Limao (2017); Holmes and Smith (1997); Baldwin et al. (1997).