6 February 2018

6 February 2018

Alasdair Smith is an Emeritus Professor of Economics at the University of Sussex, Dr Michael Gasiorek is Senior Lecturer in Economics at the University of Sussex and Director and Managing Director of InterAnalysis, Ilona Serwicka is Research Fellow in the Economics of Brexit. All are Fellows of the UK Trade Policy Observatory (UKTPO).

How would different versions of Brexit affect the UK economy? Are some parts of the economy likely to be affected more than others? Will trade deals with the rest of the world make up for any loss of UK access to EU markets? These are highly topical questions this week as the UK Cabinet’s Brexit committee makes important decisions about its objectives in the next stage of the Brexit negotiations.

They are the questions we seek to address in our new Briefing Paper ‘Which Manufacturing Sectors are Most Vulnerable to Brexit?’, published today. As it says on the tin, we answer them only for the manufacturing sectors; and in doing so we take a very disaggregated approach to UK manufacturing.

Manufacturing constitutes only 10% of the UK economy, though of course there are many jobs in services supporting and supported by manufacturing. Manufactures are a much bigger slice of UK trade, accounting for 44% of our exports and 57% of our imports; and 47% of our exports of goods and 55% of our goods imports are traded with the EU.

The impact of Brexit on manufacturing is therefore of considerable importance to the UK economy. It’s also worth paying particular attention to manufacturing because the availability of very detailed data on trade flows and trade barriers in manufacturing makes it possible to undertake data-intensive policy modelling.

We model the manufacturing economy at quite a detailed level: divided into 122 sectors. Sector titles like ‘motor vehicles’, ‘basic precious and other non-ferrous metals’, and ‘domestic appliances’ or ‘footwear’ give a sense of the degree of sectoral disaggregation.

We look at the UK’s trade relations with three country groups, the rest of the EU, the 67 countries with which the UK presently has free trade agreements with through its current membership of the EU (FTA67), and the rest of the world (ROW). We do this using trade and tariff data that is available at a very disaggregated level. Estimates of non-tariff trade barriers, like border costs and regulatory compliance costs, come from the literature, with considerably less precision and detail than trade and tariff data.

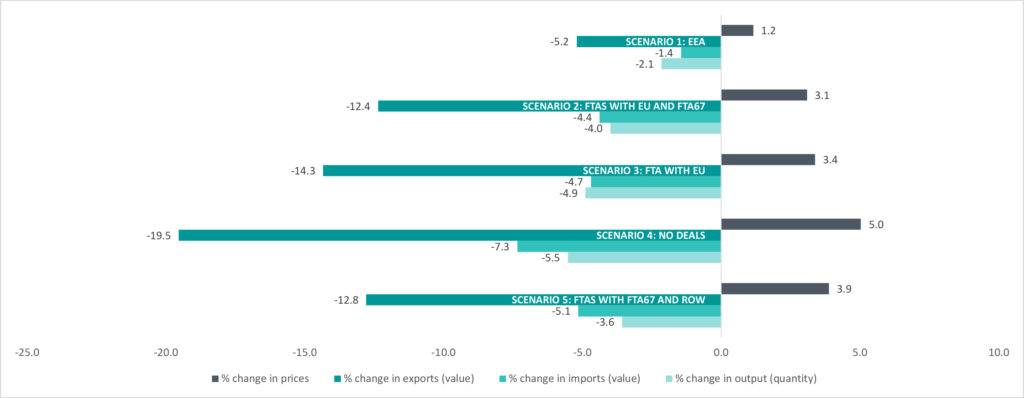

We model 5 different possible Brexit scenarios whose effects for different versions of Brexit are summarised in the Figure. The ‘softest’ Brexit is labelled “EEA” – the UK leaves the customs union but remains in the single market and retains its free trade agreement (FTA) with the EU and the FTA67. In the next two scenarios, the UK leaves the Single Market but keeps its FTA with the EU; in the former it rolls over the agreements with the FTA67, in the latter it does not. Scenario 4 is the ‘hardest’ Brexit, with no trade deals: the UK trades on WTO terms with all countries. In scenario 5, there is no trade deal with the EU, but we assume FTAs with all other countries.

Figure: How different Brexit scenarios will impact on prices, exports, imports and output in the manufacturing sector

The Figure shows the effects for all manufacturing sectors together. The first conclusion visible is that each of three main steps towards a harder Brexit has roughly equal costs: scenario 1 shows the costs of leaving the Customs Union, the step to scenario 2 shows the cost of leaving the Single Market, while the step from 3 to 4 shows the cost of not having an FTA with the EU.

The fact that the step from scenario 2 to scenario 3 is relatively small shows that the rolling over of agreements with the FTA67 is less significant than the direct changes in the UK-EU relationship. In a similar vein, scenario 5 shows that even achievement of the (literally) incredible objective of signing FTAs with every non-EU country would not compensate for the loss of the relationship with the EU. There are similar losses associated with scenarios 3 and 5: perhaps not surprisingly, having an FTA with the EU with which the UK does roughly half of its trade has a similar benefit to having FTAs with all the countries with whom the UK does the other half of its trade. But the current relationship with the EU is more than a FTA: and FTAs with the rest of the world cannot compensate for departure from the Customs Union and the Single Market.

The results differ substantially, not just between scenarios but also between sectors. The most important factor, not surprisingly, seems to be the extent to which the individual sector sells to the EU market. The sectors classified as ‘textiles, apparel & footwear’ industry grouping seem likely to shrink as a result of Brexit: a very high proportion of their output is currently sold in the EU market. By contrast, the sectors in the ‘food processing’ group have generally lower sales to the EU, but import high proportions of UK consumption from the EU: the loss of EU markets to exports has a smaller effect on the sector’s sales than the increased protection they get from raised barriers to imports from the EU. Importantly while protection might increase output for some industries this is at the expense of higher prices which impacts on consumers, and on producers buying intermediates.

We also group sectors according to the OECD classification of R&D intensity. We find that the high, medium-high and medium R&D intensive sectors all seem likely to suffer more from the effects of Brexit. This is an important result since the UK Government’s Industrial Strategy seeks to promote high-tech sectors: Brexit might make it harder to achieve this objective.

Finally, we consider the regional impact of the changes in UK manufacturing. Areas of the country where there are many jobs in food processing may see gains in output, but most manufacturing jobs are in sectors which are at risk from Brexit, and a list of the areas most at risk – Sunderland, Birmingham, Coventry, Derby, Cheshire East, Solihull, and County Durham – show the importance of the motor industry in assessing the risks of Brexit.

And this prompts a concluding warning. We are not in this paper making ‘predictions’ about precise sectoral effects of Brexit. Rather we are drawing attention to the ways that the existing structure of UK trade, combined with reasonable assumptions about possible changes in trade barriers, suggests how the effects of Brexit will differ in different manufacturing sectors. But the fortunes of the food processing sector cannot be analysed in isolation from the effects of Brexit on UK agriculture; and the fortunes of the motor industry will depend on how Brexit affects its supply chains as much as how it affects its final consumer markets. This paper is a first step in the numerical modelling of Brexit at a detailed sectoral level; it is not the last word.

Briefing Paper 16 – Which Manufacturing Sectors are Most Vulnerable to Brexit?

Press Release: High-tech industries face biggest Brexit slowdown (06.02.18)

Disclaimer:

The opinions expressed in this blog are those of the author alone and do not necessarily represent the opinions of the University of Sussex or UK Trade Policy Observatory.

Reasonable assumptions are mentioned, together with the major impact to the UK motor industry re Brexit because of the changes to the supply chain. In less than 2 years the UK has seen the inclusion of UK manufactured parts rise form 57% to 64% and it is accelerating ,not least because if the Sterling/ Euro exchange depreciation. What part has this process played in your forecasts?

We haven’t modelled any impact of exchange rate changes, just changes in trade costs, such as rising tariffs, NTMs and border cost inspections. We also have not modelled the impact on industries from changes in their costs along the supply chain, such as changes in the price of intermediate inputs. Including such linkages is for future research and may well result in the impacts being bigger than our initial estimates.

Changes in migration and hence in population levels have a very important effect on the overall impact of these studies. For example the Cambridge Econometrics study showed even the hardest Brexit would hit GVA per capita by just 0.7% over 11 years, comparing the softest of Brexits with the hardest of scenarios.

In isolation, this study has little meaning in terms of its impact on the welfare of UK citizens.

The figure is very impressive, but the horizontal axis is not labelled (£s or %, or some other value?), and there is no indication of what the different colours mean. While your arguments are logical and convincing, the confusing figure implies a lack of statistical stringency

Have you tried to model the effects of Brexit on those industries which require regulatory approvals, certifications or type-approvals etc from bodies or agencies based in the EU? Chemicals,( ECHA) pharmaceuticals (EMA) aerospace and air-travel (EASA) and automotive industries come to mind. Certification by UK “Notified Bodies” will no longer be valid in the EU, neither will their accreditation through UKAS. More generally UK exporters who are or use AEO’s registerd in the EU will need to set up AEO’s in the EU or move their operations there in order to continue to trade in the EU.

Well this is clear evidence that pursuing Brexit will have serious implications for the economy of the UK whichever path is taken. Unfortunately it appears that those in control of Government at present are pursuing Brexit for ideological reasons and have absolutely no interest in evidence of this nature. Perhaps this can persuade enough of those in charge of our future that a change of path is necessary.

How do you respond to Prof Minford article? Is his scenario realistic

https://www.thesun.co.uk/archives/politics/1086319/brexit-will-boost-our-economy-and-cut-the-cost-of-bmws-and-even-brie/

Professor Alan Winters initially responded to Prof Minford in April 2017. You can read the full article here: https://blogs.sussex.ac.uk/uktpo/2017/04/19/will-eliminating-uk-tariffs-boost-uk-gdp-by-4-percent/ and again in August 2017: https://blogs.sussex.ac.uk/uktpo/2017/08/21/the-economic-benefits-of-brexit-revisited-and-rectified/ In essence, whilst we agree that it is correct to claim that trade liberalisation is generally a very sound policy for boosting economic welfare, Minford’s article is based on an unrealistic view of the world economy, will require deeper integration with the EU as well as a race to the bottom on standards and his calculations do not include the devaluation of sterling and thus his numbers are erroneous.

[…] FTAs with each non-EU nation would not recompense for a detriment of a attribute with a EU,” write a team in an concomitant […]

[…] Which Manufacturing Sectors are Most Vulnerable to Brexit? […]

excellent study, thanks. I post it everywhere I can

[…] em 2011. Segundo o Observatório de Políticas Comerciais do Reino Unido da Universidade de Sussex(https://blogs.sussex.ac.uk/uktpo/2018/02/06/manufacturing-industry/), que estudou como o Brexit afectará a Indústria Transformadora Britânica, de forma muito […]

I agree with the approach in the study and the overview is quite insightful.

From a practical point of view, scenarios 1 and 5 are unrealistic, so I’d focus on the other three. In regards to scenario 2, I think it would be interesting to break it down; the relevance of the Pan-Euro-Med convention for UK manufacturing is different to that of the Andean Agreement, so it would be interesting to see which FTA’s (or groups of FTAs) would be more / less relevant for UK.

On the other hand, we must keep in mind that an FTA “per se” will not deliver immediate benefits; there are rules of origin that must be met, and in some sectors / industries, the assumption is that under FTA, only 30 to 40% of the products will benefit from tariff free / reduced tariff. Also, there is an additional cost for companies to comply with rules of origin which means that some companies will simply ignore the FTAs (I know that this study excludes non-tariff barriers…). Finally, FTA might imply restrictions on the application of some specific duty reliefs for UK manufacturing, typically Inward Processing Relief (I’m referring to the “non drawback” clause included in several FTAs)

[…] are concerns that British manufacturing exports could be reduced by a third, as detailed by the UK Trade Policy Observatory in their paper released earlier this […]