19 February 2019

19 February 2019

Ilona Serwicka, Research Fellow in the economics of Brexit at the UK Trade Policy Observatory and Nicolo Tamberi, Research Assistant in Economics for the Observatory.

Earlier this month, Japanese car manufacturer, Nissan made an unexpected U-turn and announced that it was no longer planning to manufacture its new X-Trail SUV model at the Sunderland plant. In a statement, Nissan said that:

‘while we have taken this decision for business reasons, the continued uncertainty around the UK’s future relationship with the EU is not helping companies like ours to plan for the future’.[1]

Yesterday, another Japanese car manufacturer, Honda, said that it was going to close its Swindon plant in 2021, and consolidate its production operations in Japan – a move that is going to put some 3,500 jobs at risk, with more jobs threatened in the supply chain. Early speculation suggests that tariff-free access to the EU is among the factors behind the company’s decision.[2]

Although neither Nissan nor Honda explicitly blamed Brexit for a decision to scale down their operations in the UK, Brexit provides the context for the decisions and for the steps that can be taken to cope with them.

Towards the end of last year, we published a briefing paper that looked at the impact of Brexit on global inward foreign investment to the UK. Our analysis suggested that the Brexit vote may have reduced foreign investment to the UK by some 19-24%. Our findings were recently confirmed by the LSE-CEP study, which found that the EU referendum reduced the number of new EU investments in the UK by 11%, amounting to £3.5 billion of lost investment. Importantly, the CEP-LSE study also found that there has been a rise in the number of new investments made by British firms in the EU, and this indicates that British firms are securing a place in the EU ahead of the Brexit date.

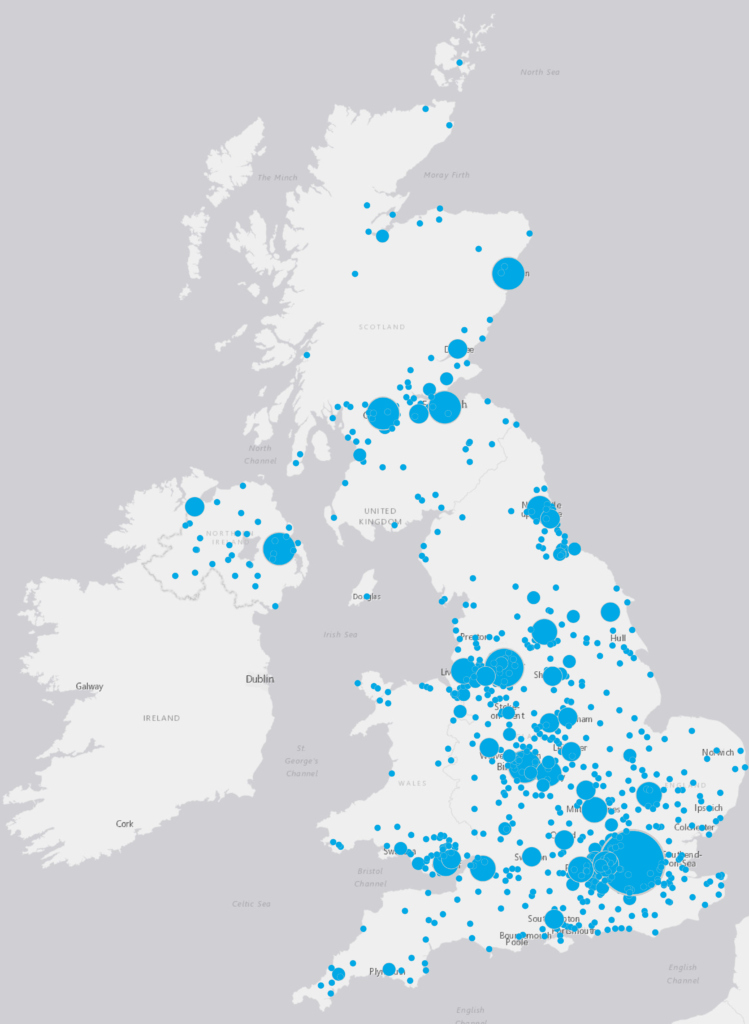

In this blog, we offer a brief description of the geographical distribution of FDI in the UK. Data come from the fDi Markets database and measures the number of greenfield FDI project announcements. The map below plots the average number of FDI projects per year over the period 2003-2018.

Reflecting the overall structure of the British economy, FDI investment to the UK is quite concentrated. As one could imagine, the main cities attract a significant number as they are the main economic centres of the country. The Greater London area stands above everywhere else, attracting almost 40% of total FDI every year, while the Greater Manchester area, second on the list, has only 3.4% of total FDI on average.

A simple exercise to see whether regions have different FDI experiences following the Brexit referendum is to compare the inward FDI before and after. The table below reports the number of average FDI projects per year before and after the referendum together with the percentage change. For symmetry, we considered 10 quarters before and 10 after the referendum.[3] We lack geographical information only for a small part of the data (reported in the ‘Not Specified’ category accounting for about 4% of total).

With the exception of the East Midlands, every region in the UK received fewer projects after the EU referendum. Wales, the North East and the East of England have seen the largest reduction, with average FDI per year decreasing by more than 30%. On the other hand, the West Midlands and Greater London had the smallest reduction – around 10%. In total, average FDI per year decreased by 16%, a figure in line with our previous estimates.[4] While the differences between regions are notable, it is too early to say that Brexit has changed the pattern of FDI inflows in a statistically significant way.

| Region | Before | After | % Change |

| East Midlands | 39 | 42 | 9.3 |

| West Midlands | 65 | 59 | -9.3 |

| Greater London | 432 | 382 | -11.7 |

| Yorkshire and Humberside | 42 | 35 | -17.1 |

| Northern Ireland | 38 | 31 | -18.9 |

| South East | 82 | 66 | -19.6 |

| Scotland | 117 | 92 | -21.2 |

| South West | 34 | 26 | -23.5 |

| North West | 70 | 52 | -26.3 |

| East of England | 48 | 34 | -29.8 |

| North East | 36 | 24 | -31.5 |

| Wales | 36 | 19 | -46.1 |

| Not Specified | 48 | 46 | -5.8 |

| Total | 1086 | 907 | -16.5 |

| Source: authors’ calculation based on fDi markets data. The table reports average number of FDI announcements per year before and after the Brexit referendum. We considered 10 quarters before and 10 after. The percentage change is computed as 100*(FDIt – FDIt-1) / FDIt-1. A chi-squared test rejected the hypothesis that before-after changes are related to region characteristics. The test statistic is X2 = 6.87 with 11 degrees of freedom.

Source: fDi Markets, a service from the Financial Times Limited 2019. All Rights Reserved. |

|||

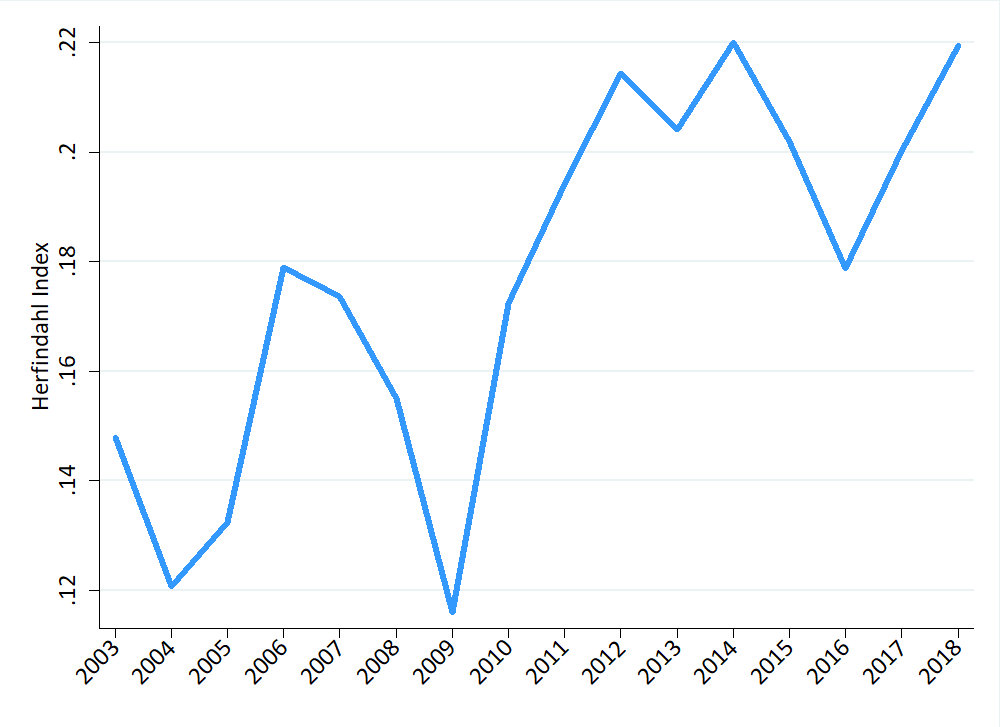

Given the relatively better performance of London at attracting investment after Brexit, it is worth looking at the spatial concentration of FDI to see whether the patterns of investment may have exacerbated existing inequalities within the UK. The index we use is the commonly-used Herfindahl index, which can range from 1, indicating that all FDI goes to one single city, to 1/N which would imply that all cities received equal shares, with N being the number of cities.

Source: authors’ own analysis using fDi Markets, a service from the Financial Times Limited 2019. All Rights Reserved.

The Herfindahl index measures concentration at the city level. It is computed as the sum of each city squared share in year t: excluding the ‘Not Specified’ category. The index varies between 1 and 1/N with H = 1 being full concentration.

Around the financial crisis (in 2009), the Herfindahl index dropped considerably, only to jump back to its pre-crisis level and then increase again. We observe some similar behaviour in the period around the Brexit referendum: concentration dropped in 2016 only to increase sharply in 2017-18 to reach 2015 values again. Although movements in the concentration index are largely driven by what happens in London, the basic pattern holds, even if we exclude the capital from the sample.

Some have suggested that the Brexit vote reflected the pain in those parts of the country that felt left behind because of lacking opportunities or future prospects – with Brexit seen as a way of reversing existing regional inequalities.[5] What we have seen so far – mainly due to uncertainty – does not reveal clear regional patterns, with foreign investment falling in most places. However, it certainly does not display the rebalancing towards disadvantaged regions that such people hoped for. Indeed, the recent announcements from Nissan and Honda suggest that it may be those places least able to withstand negative economic impacts that will face the worst of the coming storms.

[1] Parker, G., Campbell, P. and Tighe, Ch. (2019) Nissan U-turn is a no-deal Brexit ‘warning sign’, says Clark, The Financial Times, 3 February 2019. Available at: https://www.ft.com/content/92825130-27a2-11e9-a5ab-ff8ef2b976c7.

[2] Kleinman, M. (2019) Honda to stun ministers with closure of Swindon factory, Sky News, 18 February 2019. Available at: https://news.sky.com/story/honda-to-stun-ministers-with-closure-of-swindon-factory-11641154.

[3] The choice of ten quarters is dictated by data availability. At present, FDI data are available until December 2018.

[4] Note that our previous figure where computed as the difference between the observed UK and the estimated counterfactual, while this is a simple change over time.

[5] Rodriguez-Pose, A. (2018) The revenge of places that don’t matter, VOX CEPR Policy Portal. Available at: https://voxeu.org/article/revenge-places-dont-matter.

Disclaimer:

The opinions expressed in this blog are those of the author alone and do not necessarily represent the opinions of the University of Sussex or UK Trade Policy Observatory.

Republishing guidelines:

The UK Trade Policy Observatory believes in the free flow of information and encourages readers to cite our materials, providing due acknowledgement. For online use, this should be a link to the original resource on our website. We do not publish under a Creative Commons license. This means you CANNOT republish our articles online or in print for free.